Question: solve this question in below 2. This question is on solving stochastic differential equations. The state variable X- satisfies the stochastic differential equation dXt =

solve this question in below

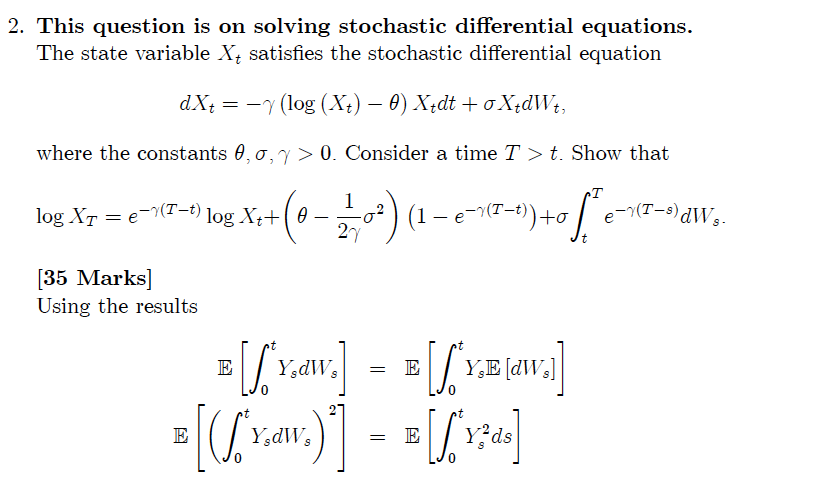

2. This question is on solving stochastic differential equations. The state variable X- satisfies the stochastic differential equation dXt = -y (log (X+) - 0) Xtdt + oXtdWt, where the constants 0, o, y > 0. Consider a time T > t. Show that T log Xr = e-7(T-t) log Xt+ (0- 2 ( 1 - e- 7( I-t) ) to e (T-5) dWs. [35 Marks] Using the results t E YsdWs = E 0 0 YsE [dWs] t 2 E YsdWs = E Y-ds 0 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock