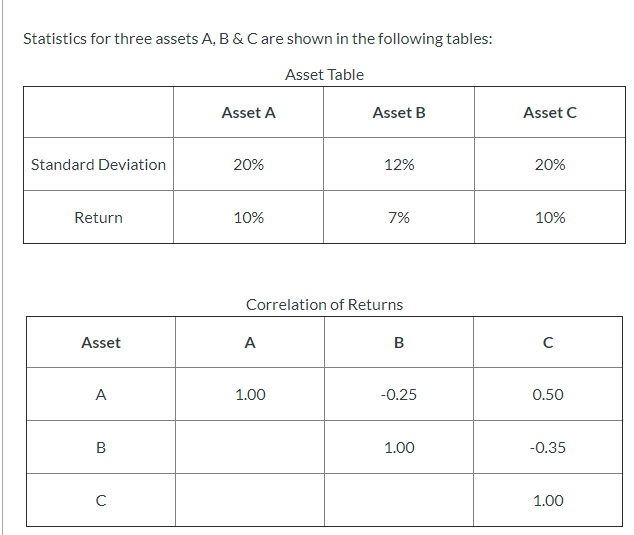

Question: Statistics for three assets A, B & Care shown in the following tables: Asset Table Asset A Asset B Asset C Standard Deviation 20% 12%

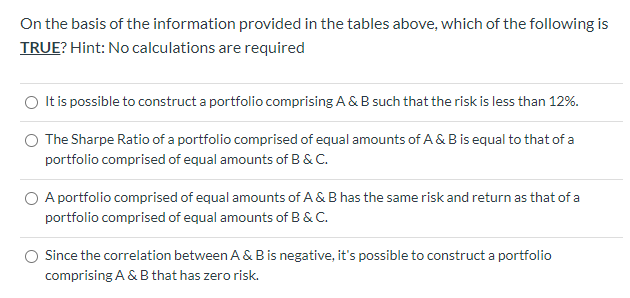

Statistics for three assets A, B & Care shown in the following tables: Asset Table Asset A Asset B Asset C Standard Deviation 20% 12% 20% Return 10% 7% 10% Correlation of Returns Asset A B A 1.00 -0.25 0.50 B 1.00 -0.35 C 1.00 On the basis of the information provided in the tables above, which of the following is TRUE? Hint: No calculations are required It is possible to construct a portfolio comprising A & B such that the risk is less than 12%. The Sharpe Ratio of a portfolio comprised of equal amounts of A & B is equal to that of a portfolio comprised of equal amounts of B &C. A portfolio comprised of equal amounts of A&B has the same risk and return as that of a portfolio comprised of equal amounts of B & C. Since the correlation between A & B is negative, it's possible to construct a portfolio comprising A & B that has zero risk

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts