Question: Step by Step Please include formulas. Please !! Thank You!! A and FB? (Bounds on returns) Consider a universe of just three securities rates of

Step by Step Please include formulas.

Please !!

Thank You!!

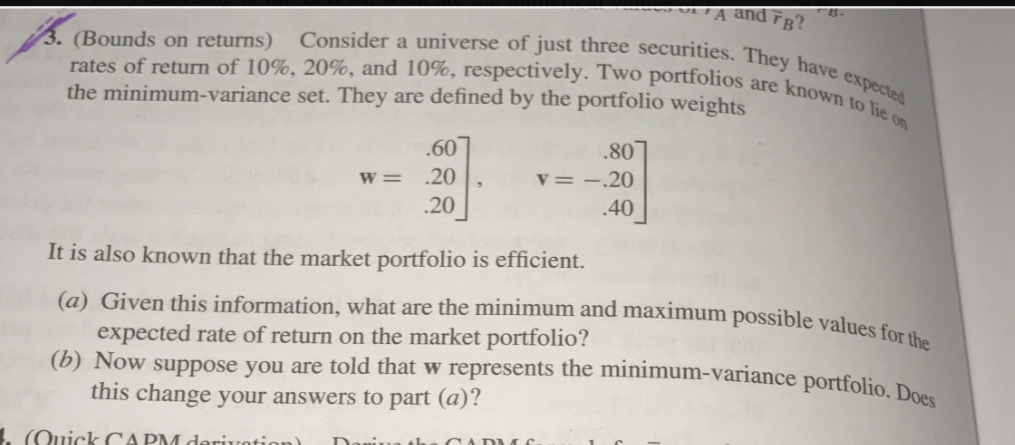

A and FB? (Bounds on returns) Consider a universe of just three securities rates of return of 10%, 20%, and 10%, respectively. Two portfolios They have ex are known to lie pected the minimum variance set. They are defined by the portfolio w ce set. They are defined by the portfolio weights .60 w= .20 .20 .80 20 .40 It is also known that the market portfolio is efficient. (a) Given this information, what are the minimum and maximum po ssible values for the expected rate of return on the market portfolio? (b) Now suppose you are told that w represents the minimum-variance portfolio Does this change your answers to part (a)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts