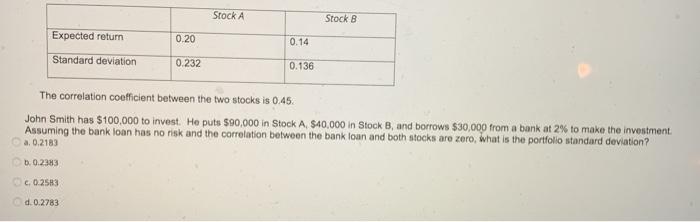

Question: Stock A Stock B Expected return 0.20 0.14 Standard deviation 0.232 0.136 The correlation coefficient between the two stocks is 0.45 John Smith has $100,000

Stock A Stock B Expected return 0.20 0.14 Standard deviation 0.232 0.136 The correlation coefficient between the two stocks is 0.45 John Smith has $100,000 to invest. He puts $90,000 in Stock A $40,000 in Stock B, and borrows $30,000 from a bank at 2% to make the investment Assuming the bank loan has no risk and the correlation between the bank loan and both stocks are zero, what is the portfolio standard deviation? a 0.2183 0.0.2383 C. 0.2583 d. 0.2783

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock