Question: Suppose Johnson & Johnson and Walgreen Boots Alliance have expected returns and volatilities shown here, with a correlation of 20%. Calculate (a) the expected return

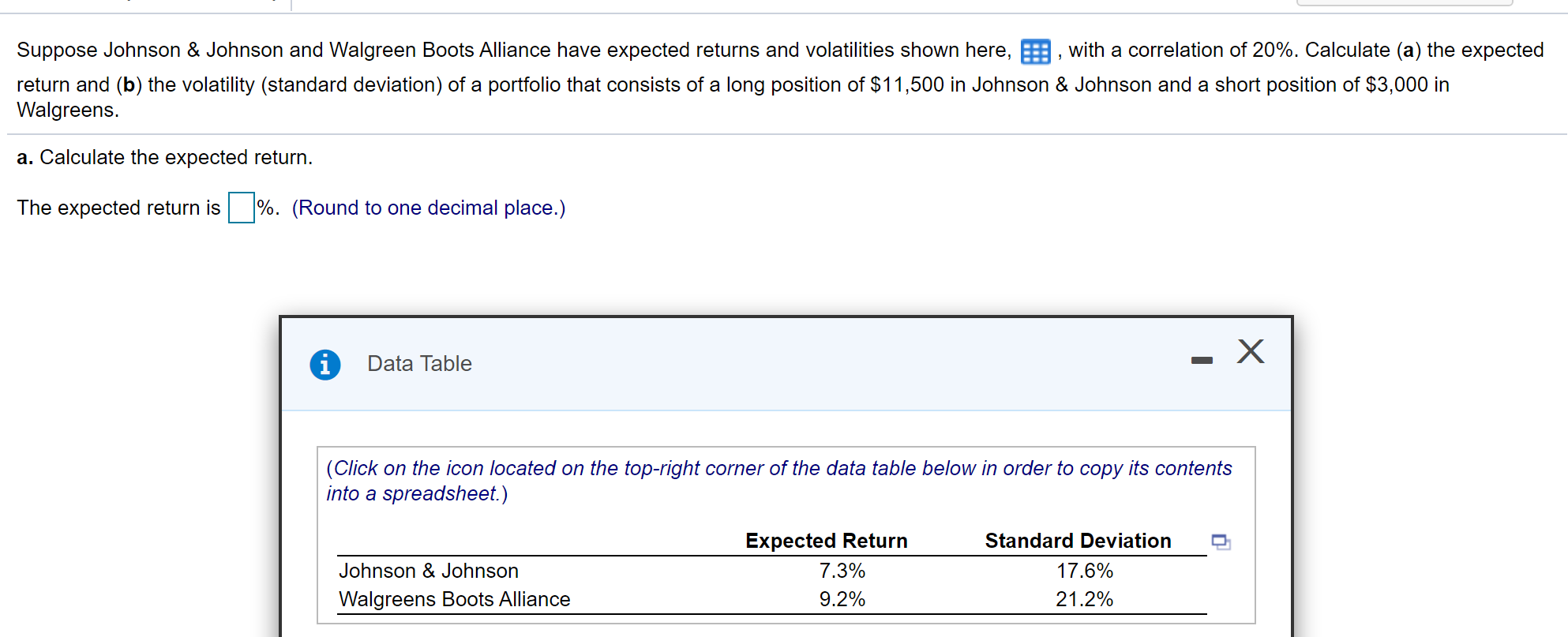

Suppose Johnson & Johnson and Walgreen Boots Alliance have expected returns and volatilities shown here, with a correlation of 20%. Calculate (a) the expected return and (b) the volatility (standard deviation) of a portfolio that consists of a long position of $11,500 in Johnson & Johnson and a short position of $3,000 in Walgreens. a. Calculate the expected return. The expected return is %. (Round to one decimal place.) i Data Table - (Click on the icon located on the top-right corner of the data table below in order to copy its contents into a spreadsheet.) Johnson & Johnson Walgreens Boots Alliance Expected Return 7.3% 9.2% Standard Deviation 17.6% 21.2%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts