Question: Suppose that a two-factor (Factor X and Factor Y) model describes the return generating processes of all securities in the market and that the

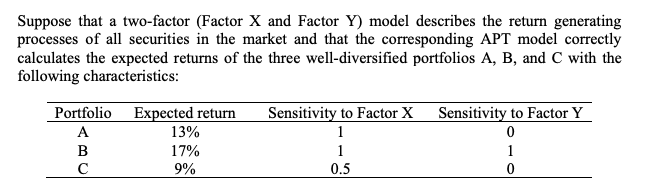

Suppose that a two-factor (Factor X and Factor Y) model describes the return generating processes of all securities in the market and that the corresponding APT model correctly calculates the expected returns of the three well-diversified portfolios A, B, and C with the following characteristics: Portfolio Expected return A BC 13% 17% 9% Sensitivity to Factor X Sensitivity to Factor Y 1 1 0.5 0 1 0 b) Suppose that Portfolio D's expected return is 10% instead. The risk-free rate is 5%. How would you exploit the arbitrage opportunity? In other words, design an arbitrage strategy consisting of portfolios A, B, D, and the risk-free asset. Assume that portfolios A, B, and D are well diversified to the extent that their idiosyncratic risks are negligible, and that all portfolios and the risk-free asset can be bought on margin or sold short.

Step by Step Solution

3.43 Rating (143 Votes )

There are 3 Steps involved in it

Given the new information about Portfolio D Portfolio Ds expected return is 1... View full answer

Get step-by-step solutions from verified subject matter experts