(b) Suppose that today is 30 June 2023. The spot exchange rate between the Swiss franc and...

Question:

(b) Suppose that today is 30 June 2023. The spot exchange rate between the Swiss franc and the US dollar is 1.09 dollars per franc. A European put option on the Swiss franc with a strike price of 1.09 dollars per franc and expiration date of 30 November 2023 is trading at 0.0184 dollars per franc.

(i) What is the time value of this put option contract?

(ii) Suppose that the volatility of the franc-dollar exchange rate increases, but everything else stays the same. How would the premium of the put option be affected?

(iii) A second Swiss franc put option has a strike price of 1.11 dollars per franc and the same expiration date as the first. Would the premium of the second put option be higher or lower than that of the first? Explain why.

(iv) A third franc put option has an expiration date of 30 September 2023 and the same strike price as the first. Would the premium of the third put option be higher or lower than that of the first? Explain why

Expert Answer:

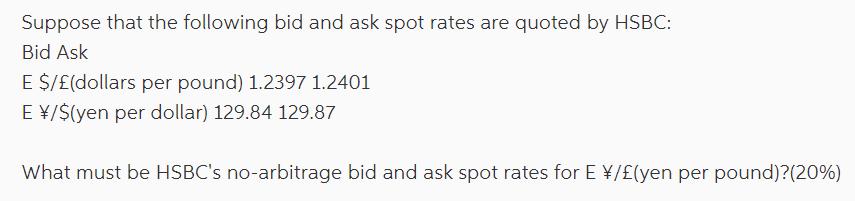

Calculate the bid and ask rates as follows 1 Bid Rate1298412401 10470 2 Ask Rate 1298712397 10476 Th... View the full answer