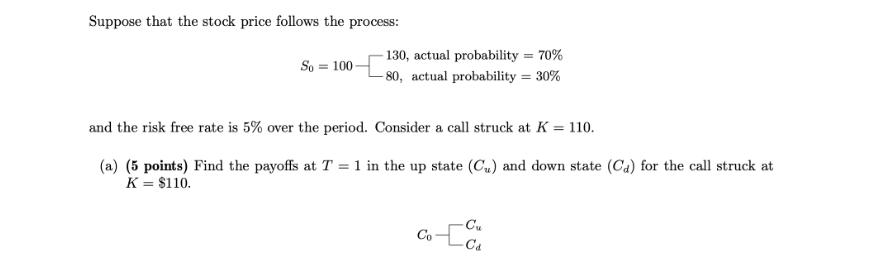

Suppose that the stock price follows the process: So 100- 130, actual probability = 70% -80,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

It seems that you would like assistance with a set of problems related to options pricing using the binomial model which involves finding payoffs calculating the option price and answering truefalse q... View the full answer

Related Book For

Posted Date: