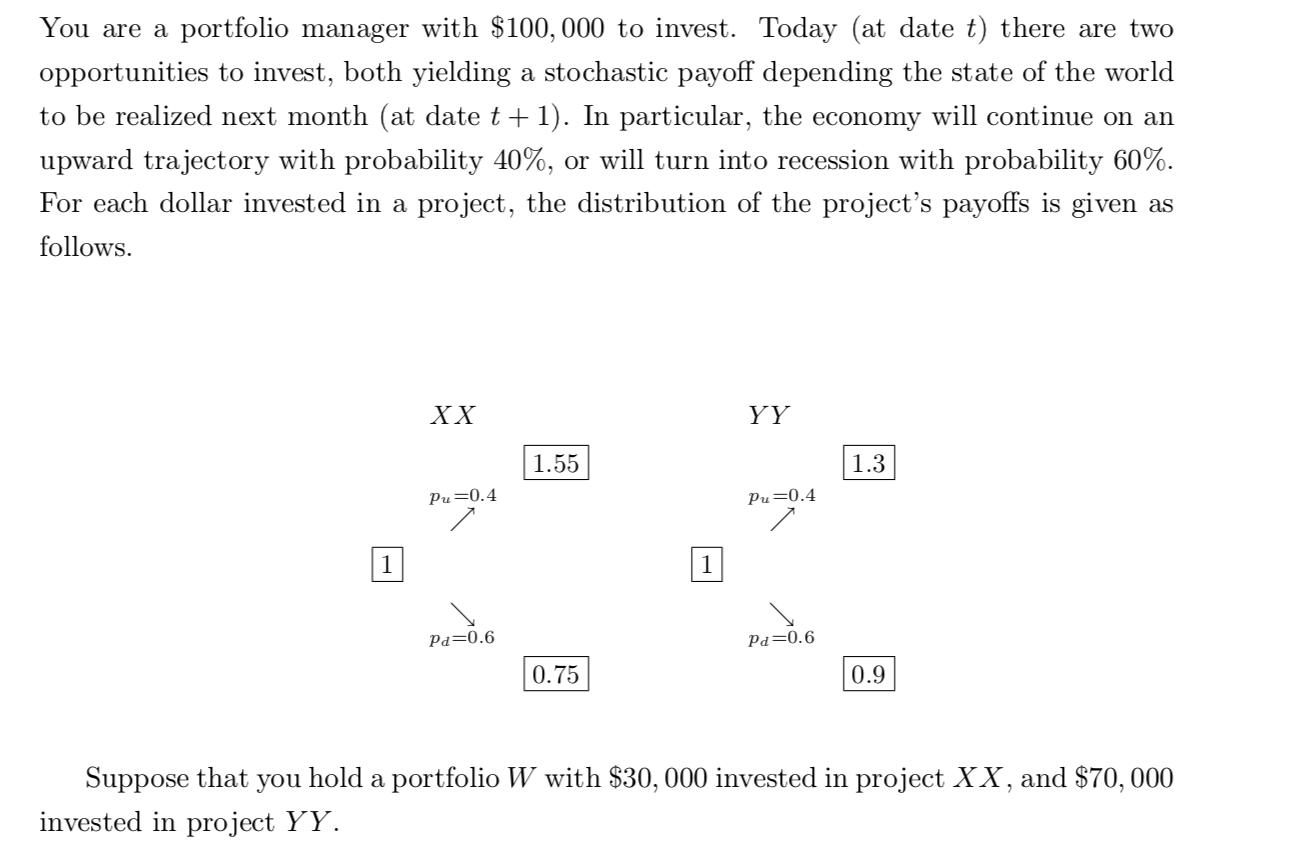

Suppose that your preferences are captured by a mean-variance utility function, with a risk aversion coefficient a=

Fantastic news! We've Found the answer you've been seeking!

Question:

Suppose that your preferences are captured by a mean-variance utility function, with a risk aversion coefficient a= 0:7. If given a choice to invest the entire amount of $100,000 in a single project, which would you choose: project XX, project Y Y , or a risk-free project, F, that yields a rate of return of rF = 3.5%?

You are given an additional $100; 000 to invest. How do you allocate it between your original portfolio, W, and the risk-free project, F?

Expert Answer:

I dont have personal preferences or the ability to invest money However I can provide some guidance based on the meanvariance utility function and ris... View the full answer

Related Book For

Microeconomics An Intuitive Approach with Calculus

ISBN: 978-0538453257

1st edition

Authors: Thomas Nechyba

Posted Date: