You are a portfolio manager with $100,000 to invest. Today (at date t) there are two opportunities

Question:

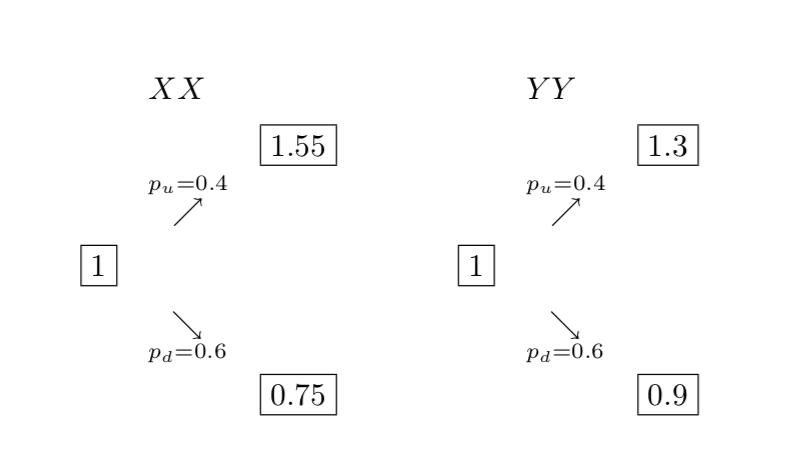

You are a portfolio manager with $100,000 to invest. Today (at date t) there are two opportunities to invest, both yielding a stochastic payoff depending the state of the world to be realized next month (at date t + 1). In particular, the economy will continue on an upward trajectory with probability 40%, or will turn into recession with probability 60%. For each dollar invested in a project, the distribution of the project's payoff is given as follows:

Suppose that you hold a portfolio W with $30,000 invested in project XX, and $70,000 invested in project Y Y

1. What is the expected payoff and the variance of project XX? What is the expected payo§ and the variance of project Y Y ?

2. What is the expected payoff of your portfolio as of today (date t)? What about the standard deviation of your portfolio?

3.How does the risk of the portfolio compare with the risk of the individual projects (i.e. investing the entire $100; 000 in either project XX or Y Y )?

4.What is the expected rate of return of your portfolio as of today (date t)? What about the standard deviation of the rate of return?

Expert Answer:

Based on the information provided we can calculate the expected payoff and the variance for projects XX and YY as follows For Project XX The payoff in the upward trajectory u is 155 and the probabilit... View the full answer

Microeconomics An Intuitive Approach with Calculus

ISBN: 978-0538453257

1st edition

Authors: Thomas Nechyba