Question: Suppose the average return on T-Bills was 1%. The average factor risk premiums are the following: .market (MKT): 6% size (SMB) 2% value (HML): 3%

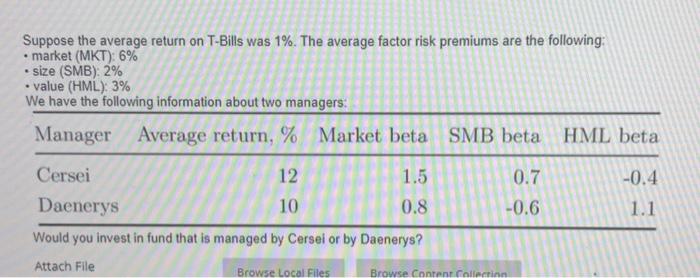

Suppose the average return on T-Bills was 1%. The average factor risk premiums are the following: .market (MKT): 6% size (SMB) 2% value (HML): 3% We have the following information about two managers: Manager Average return, % Market beta SMB beta HML beta -0.4 Cersei 12 1.5 Daenerys 10 0.8 Would you invest in fund that is managed by Cersei or by Daenerys? 0.7 -0.6 1.1 Attach File Browse Local Files Browse Content Collectinn

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock