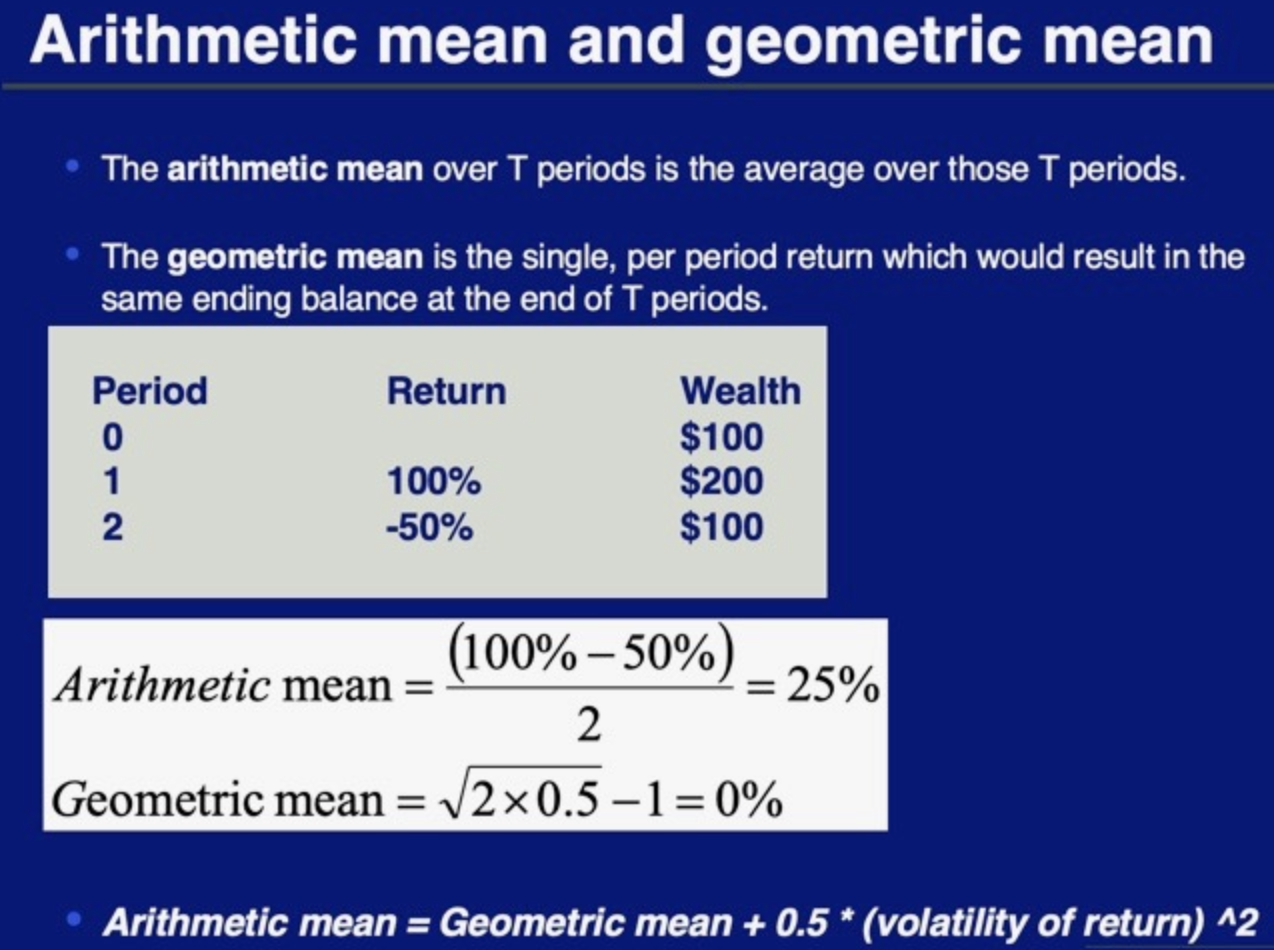

Suppose the geometric mean for Japanese Government Bond monthly return in a year is 1.75% and arithmetic

Fantastic news! We've Found the answer you've been seeking!

Question:

Suppose the geometric mean for Japanese Government Bond monthly return in a year is 1.75% and arithmetic mean is 2%. Suppose the Emerging market equity is twice as volatile as the Japanese bond in the same period. If the geometric mean for emerging market equity monthly return is 2% in a year, what's the arithmetic mean of the Emerging market equity monthly return in a year? See Formula in. attached Snipit.

Expert Answer:

Related Book For

Posted Date: