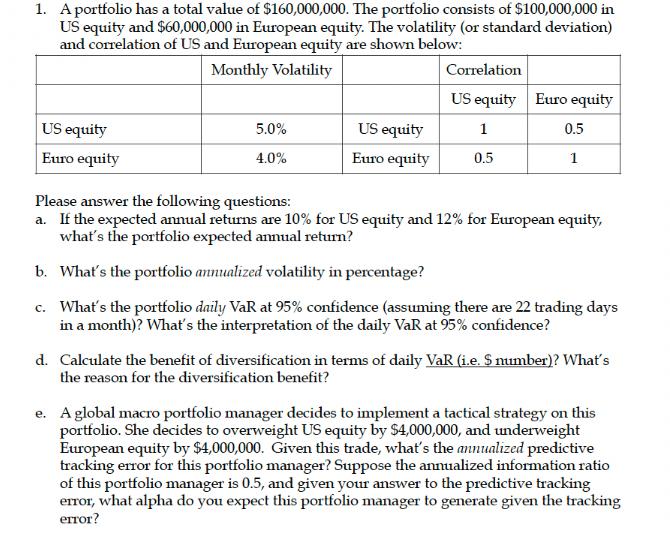

1. A portfolio has a total value of $160,000,000. The portfolio consists of $100,000,000 in US...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

1. A portfolio has a total value of $160,000,000. The portfolio consists of $100,000,000 in US equity and $60,000,000 in European equity. The volatility (or standard deviation) and correlation of US and European equity are shown below: Monthly Volatility US equity Euro equity 5.0% 4.0% US equity Euro equity Correlation US equity 1 0.5 Euro equity 0.5 1 Please answer the following questions: a. If the expected annual returns are 10% for US equity and 12% for European equity, what's the portfolio expected annual return? b. What's the portfolio annualized volatility in percentage? c. What's the portfolio daily VaR at 95% confidence (assuming there are 22 trading days in a month)? What's the interpretation of the daily VaR at 95% confidence? d. Calculate the benefit of diversification in terms of daily VaR (i.e. S number)? What's the reason for the diversification benefit? e. A global macro portfolio manager decides to implement a tactical strategy on this portfolio. She decides to overweight US equity by $4,000,000, and underweight European equity by $4,000,000. Given this trade, what's the annualized predictive tracking error for this portfolio manager? Suppose the annualized information ratio of this portfolio manager is 0.5, and given your answer to the predictive tracking error, what alpha do you expect this portfolio manager to generate given the tracking error? 2. Suppose the geometric mean for Japanese Government Bond monthly return in a year is 1.75% and arithmetic mean is 2%. Suppose the Emerging market equity is twice as volatile as the Japanese bond in the same period. a. If the geometric mean for emerging market equity monthly return is 2% in a year, what's the arithmetic mean of the Emerging market equity monthly return in a year? 3. For the pension plan of a company XYZ, the strategic asset allocation is 60% in global equity and 35% in global fixed income and 5% in US cash. a. If the global equity market generates negative return and bond yield declines in the coming year, what will happen to the PBO funded ratio? Why? b. The pension plan sponsor of company XYZ wants to reduce the risk of the portfolio. His suggestion is to increase the cash allocation from 5% to 20% since cash is the "risk-free" asset. Considering cash as an asset and as an investment in a pension portfolio, do you agree with his suggestion? Why? c. The pension plan sponsor expects the asset return to be low and bond yield remains low in the future. Suppose the pension plan has a PBO funded ratio of 85% currently. In order to minimize the amount of corporate contribution to the pension plan and increase funded ratio, the pension plan sponsor is very interested in applying the Alpha Beta framework to his pension fund. Please provide your recommendation using Alpha/Beta investment framework. What should be the new asset allocation strategy? How much active risk should the pension plan take? Be specific and provide the rationale for your recommendation. d. In particular, the pension plan sponsor is considering investing in hedge fund. Do you think hedge fund is a good investment vehicle for the pension plan? Give a detailed discussion of hedge funds as an investment in pension plans. Be thorough in your answers. 4. An endowment Chief Investment Officer is considering investment ($100 million) with an active global equity manager. One candidate manager is a fundament driven stock picker (very similar to the China Fund manager that we have talked about in the class). The fundamental manager runs a strategy that has an alpha target of 5% and a track error target of 10%. The other candidate manager is a quantitatively driven active equity manager (very similar to GSAM case as we have discussed in the class). The quantitative manager has an alpha target of 2.5% and a tracking error target of 3.5%. The two managers' alpha streams historically have a correlation of 0.1. a. Please comment on the pros and cons of these two investment styles (fundamental vs. quantitative) for active equity management. b. How would you recommend the endowment CIO to structure her active global equity allocation ($100 million)? Specifically, should she hire one manager vs. another? Should she split her allocation between the two managers? If so, what's the split? Please provide detailed rationale for your recommendation. 1. A portfolio has a total value of $160,000,000. The portfolio consists of $100,000,000 in US equity and $60,000,000 in European equity. The volatility (or standard deviation) and correlation of US and European equity are shown below: Monthly Volatility US equity Euro equity 5.0% 4.0% US equity Euro equity Correlation US equity 1 0.5 Euro equity 0.5 1 Please answer the following questions: a. If the expected annual returns are 10% for US equity and 12% for European equity, what's the portfolio expected annual return? b. What's the portfolio annualized volatility in percentage? c. What's the portfolio daily VaR at 95% confidence (assuming there are 22 trading days in a month)? What's the interpretation of the daily VaR at 95% confidence? d. Calculate the benefit of diversification in terms of daily VaR (i.e. S number)? What's the reason for the diversification benefit? e. A global macro portfolio manager decides to implement a tactical strategy on this portfolio. She decides to overweight US equity by $4,000,000, and underweight European equity by $4,000,000. Given this trade, what's the annualized predictive tracking error for this portfolio manager? Suppose the annualized information ratio of this portfolio manager is 0.5, and given your answer to the predictive tracking error, what alpha do you expect this portfolio manager to generate given the tracking error? 2. Suppose the geometric mean for Japanese Government Bond monthly return in a year is 1.75% and arithmetic mean is 2%. Suppose the Emerging market equity is twice as volatile as the Japanese bond in the same period. a. If the geometric mean for emerging market equity monthly return is 2% in a year, what's the arithmetic mean of the Emerging market equity monthly return in a year? 3. For the pension plan of a company XYZ, the strategic asset allocation is 60% in global equity and 35% in global fixed income and 5% in US cash. a. If the global equity market generates negative return and bond yield declines in the coming year, what will happen to the PBO funded ratio? Why? b. The pension plan sponsor of company XYZ wants to reduce the risk of the portfolio. His suggestion is to increase the cash allocation from 5% to 20% since cash is the "risk-free" asset. Considering cash as an asset and as an investment in a pension portfolio, do you agree with his suggestion? Why? c. The pension plan sponsor expects the asset return to be low and bond yield remains low in the future. Suppose the pension plan has a PBO funded ratio of 85% currently. In order to minimize the amount of corporate contribution to the pension plan and increase funded ratio, the pension plan sponsor is very interested in applying the Alpha Beta framework to his pension fund. Please provide your recommendation using Alpha/Beta investment framework. What should be the new asset allocation strategy? How much active risk should the pension plan take? Be specific and provide the rationale for your recommendation. d. In particular, the pension plan sponsor is considering investing in hedge fund. Do you think hedge fund is a good investment vehicle for the pension plan? Give a detailed discussion of hedge funds as an investment in pension plans. Be thorough in your answers. 4. An endowment Chief Investment Officer is considering investment ($100 million) with an active global equity manager. One candidate manager is a fundament driven stock picker (very similar to the China Fund manager that we have talked about in the class). The fundamental manager runs a strategy that has an alpha target of 5% and a track error target of 10%. The other candidate manager is a quantitatively driven active equity manager (very similar to GSAM case as we have discussed in the class). The quantitative manager has an alpha target of 2.5% and a tracking error target of 3.5%. The two managers' alpha streams historically have a correlation of 0.1. a. Please comment on the pros and cons of these two investment styles (fundamental vs. quantitative) for active equity management. b. How would you recommend the endowment CIO to structure her active global equity allocation ($100 million)? Specifically, should she hire one manager vs. another? Should she split her allocation between the two managers? If so, what's the split? Please provide detailed rationale for your recommendation. 1. A portfolio has a total value of $160,000,000. The portfolio consists of $100,000,000 in US equity and $60,000,000 in European equity. The volatility (or standard deviation) and correlation of US and European equity are shown below: Monthly Volatility US equity Euro equity 5.0% 4.0% US equity Euro equity Correlation US equity 1 0.5 Euro equity 0.5 1 Please answer the following questions: a. If the expected annual returns are 10% for US equity and 12% for European equity, what's the portfolio expected annual return? b. What's the portfolio annualized volatility in percentage? c. What's the portfolio daily VaR at 95% confidence (assuming there are 22 trading days in a month)? What's the interpretation of the daily VaR at 95% confidence? d. Calculate the benefit of diversification in terms of daily VaR (i.e. S number)? What's the reason for the diversification benefit? e. A global macro portfolio manager decides to implement a tactical strategy on this portfolio. She decides to overweight US equity by $4,000,000, and underweight European equity by $4,000,000. Given this trade, what's the annualized predictive tracking error for this portfolio manager? Suppose the annualized information ratio of this portfolio manager is 0.5, and given your answer to the predictive tracking error, what alpha do you expect this portfolio manager to generate given the tracking error? 2. Suppose the geometric mean for Japanese Government Bond monthly return in a year is 1.75% and arithmetic mean is 2%. Suppose the Emerging market equity is twice as volatile as the Japanese bond in the same period. a. If the geometric mean for emerging market equity monthly return is 2% in a year, what's the arithmetic mean of the Emerging market equity monthly return in a year? 3. For the pension plan of a company XYZ, the strategic asset allocation is 60% in global equity and 35% in global fixed income and 5% in US cash. a. If the global equity market generates negative return and bond yield declines in the coming year, what will happen to the PBO funded ratio? Why? b. The pension plan sponsor of company XYZ wants to reduce the risk of the portfolio. His suggestion is to increase the cash allocation from 5% to 20% since cash is the "risk-free" asset. Considering cash as an asset and as an investment in a pension portfolio, do you agree with his suggestion? Why? c. The pension plan sponsor expects the asset return to be low and bond yield remains low in the future. Suppose the pension plan has a PBO funded ratio of 85% currently. In order to minimize the amount of corporate contribution to the pension plan and increase funded ratio, the pension plan sponsor is very interested in applying the Alpha Beta framework to his pension fund. Please provide your recommendation using Alpha/Beta investment framework. What should be the new asset allocation strategy? How much active risk should the pension plan take? Be specific and provide the rationale for your recommendation. d. In particular, the pension plan sponsor is considering investing in hedge fund. Do you think hedge fund is a good investment vehicle for the pension plan? Give a detailed discussion of hedge funds as an investment in pension plans. Be thorough in your answers. 4. An endowment Chief Investment Officer is considering investment ($100 million) with an active global equity manager. One candidate manager is a fundament driven stock picker (very similar to the China Fund manager that we have talked about in the class). The fundamental manager runs a strategy that has an alpha target of 5% and a track error target of 10%. The other candidate manager is a quantitatively driven active equity manager (very similar to GSAM case as we have discussed in the class). The quantitative manager has an alpha target of 2.5% and a tracking error target of 3.5%. The two managers' alpha streams historically have a correlation of 0.1. a. Please comment on the pros and cons of these two investment styles (fundamental vs. quantitative) for active equity management. b. How would you recommend the endowment CIO to structure her active global equity allocation ($100 million)? Specifically, should she hire one manager vs. another? Should she split her allocation between the two managers? If so, what's the split? Please provide detailed rationale for your recommendation. 1. A portfolio has a total value of $160,000,000. The portfolio consists of $100,000,000 in US equity and $60,000,000 in European equity. The volatility (or standard deviation) and correlation of US and European equity are shown below: Monthly Volatility US equity Euro equity 5.0% 4.0% US equity Euro equity Correlation US equity 1 0.5 Euro equity 0.5 1 Please answer the following questions: a. If the expected annual returns are 10% for US equity and 12% for European equity, what's the portfolio expected annual return? b. What's the portfolio annualized volatility in percentage? c. What's the portfolio daily VaR at 95% confidence (assuming there are 22 trading days in a month)? What's the interpretation of the daily VaR at 95% confidence? d. Calculate the benefit of diversification in terms of daily VaR (i.e. S number)? What's the reason for the diversification benefit? e. A global macro portfolio manager decides to implement a tactical strategy on this portfolio. She decides to overweight US equity by $4,000,000, and underweight European equity by $4,000,000. Given this trade, what's the annualized predictive tracking error for this portfolio manager? Suppose the annualized information ratio of this portfolio manager is 0.5, and given your answer to the predictive tracking error, what alpha do you expect this portfolio manager to generate given the tracking error? 2. Suppose the geometric mean for Japanese Government Bond monthly return in a year is 1.75% and arithmetic mean is 2%. Suppose the Emerging market equity is twice as volatile as the Japanese bond in the same period. a. If the geometric mean for emerging market equity monthly return is 2% in a year, what's the arithmetic mean of the Emerging market equity monthly return in a year? 3. For the pension plan of a company XYZ, the strategic asset allocation is 60% in global equity and 35% in global fixed income and 5% in US cash. a. If the global equity market generates negative return and bond yield declines in the coming year, what will happen to the PBO funded ratio? Why? b. The pension plan sponsor of company XYZ wants to reduce the risk of the portfolio. His suggestion is to increase the cash allocation from 5% to 20% since cash is the "risk-free" asset. Considering cash as an asset and as an investment in a pension portfolio, do you agree with his suggestion? Why? c. The pension plan sponsor expects the asset return to be low and bond yield remains low in the future. Suppose the pension plan has a PBO funded ratio of 85% currently. In order to minimize the amount of corporate contribution to the pension plan and increase funded ratio, the pension plan sponsor is very interested in applying the Alpha Beta framework to his pension fund. Please provide your recommendation using Alpha/Beta investment framework. What should be the new asset allocation strategy? How much active risk should the pension plan take? Be specific and provide the rationale for your recommendation. d. In particular, the pension plan sponsor is considering investing in hedge fund. Do you think hedge fund is a good investment vehicle for the pension plan? Give a detailed discussion of hedge funds as an investment in pension plans. Be thorough in your answers. 4. An endowment Chief Investment Officer is considering investment ($100 million) with an active global equity manager. One candidate manager is a fundament driven stock picker (very similar to the China Fund manager that we have talked about in the class). The fundamental manager runs a strategy that has an alpha target of 5% and a track error target of 10%. The other candidate manager is a quantitatively driven active equity manager (very similar to GSAM case as we have discussed in the class). The quantitative manager has an alpha target of 2.5% and a tracking error target of 3.5%. The two managers' alpha streams historically have a correlation of 0.1. a. Please comment on the pros and cons of these two investment styles (fundamental vs. quantitative) for active equity management. b. How would you recommend the endowment CIO to structure her active global equity allocation ($100 million)? Specifically, should she hire one manager vs. another? Should she split her allocation between the two managers? If so, what's the split? Please provide detailed rationale for your recommendation.

Expert Answer:

Answer rating: 100% (QA)

Lets address each question one by one Portfolio Analysis a To find the portfolios expected annual return you can use a weighted average of the expected returns for US and European equity Portfolio Exp... View the full answer

Related Book For

Fundamentals of Cost Accounting

ISBN: 978-0077398194

3rd Edition

Authors: William Lanen, Shannon Anderson, Michael Maher

Posted Date:

Students also viewed these finance questions

-

A large pipe called a penstock in hydraulic workis 1.5in diameter. The pipe thick with a maximum tensile strength of 300Mpa a. Determine the max bursting pressure (Kpa) if the max depth of water in...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

The following additional information is available for the Dr. Ivan and Irene Incisor family from Chapters 1-5. Ivan's grandfather died and left a portfolio of municipal bonds. In 2012, they pay Ivan...

-

Jack Williams works in a very active department called purchasing. He works with store managers, marketing, and supply companies. The people in his department try to have the right product, in the...

-

Rachel borrowed $10,000 and agreed to pay back the loan with five consecutive annual payments, with the first payment occurring in one year. If the annual interest rate is 5%, what is the amount of...

-

Scrooge and Zilch, a public accounting firm in London, is engaged in the preparation of income tax returns for individuals. The firm uses the weighted-average method of process costing for internal...

-

What are examples of Natural Systems Environment threats and their sources?

-

What factors outside Browns control interfered with his efforts to work with the utility? MINI CASE Reggie Brown, B&W Nuclear Service Companys (BWNS) project manager for Nita Light and Powers Green...

-

Question 5 . Each set of Bragg planes can be referred to systematically by "Miller Indices" that indicate the way in which the Bragg planes cut the unit cell. Miller indices are a group of three...

-

Create a concept map that depicts your assumptions and findings of the theory-practice gap. You are a staff nurse working in an intensive care unit and assigned to care for a 75-year-old African...

-

What are the LIMITATIONS OF SALES PROMOTION?

-

Indicate whether each of the following statements is true or false by writing T or F in the answer c olumn. Words or terms that become a common part of the language are referred to as generic.

-

Why was the limited exemption from antitrust laws so crucial to the development of the NFL?

-

1. You have just started a new company to deliver mail and parcels to rural communities. At the moment, other companies either do not provide a service or are exceptionally expensive. The new company...

-

Indicate whether each of the following statements is true or false by writing T or F in the answer c olumn. The Green Giant is an example of a trade name.

-

Why cant Premier League teams like Arsenal exert as much monopoly power as the NFL's Chicago Bears?

-

An individual wants to manage its demand for monetary assets. The options available include a bank deposit that pays 15% interest but requires 2 hours of dedicated time at the bank during work hours...

-

Show that the peak of the black body spectrum as a function of ? is given by eq. (22.14) kg T Wmax = 2.82

-

It has been said that a prior departments costs behave similarly to direct materials costs. Under what conditions are the costs similar? Why account for them separately?

-

Peninsula Candy Company makes three types of candy bars: Chewy, Chunky, and Choco-Lite (Lite). Sales volume for the annual budget is determined by estimating the total market volume for candy bars...

-

Sell Block prepares three types of simple tax returns: individual, partnerships, and (small) corporations. The tax returns have the following characteristics: The total fixed costs per year for the...

-

The following time-series plot and bar graph both present the sales of digital music for the years 20122015. Which of the graphs presents the more accurate picture? Why? Million $ 5000 4800- 5000...

-

The Dow Jones Industrial Average reached its lowest point in recent history on October 9, 2008, when it closed at $8,579. Eight years later, on October 10, 2016, the average had risen to $18,329.04....

-

In 2007, U.S. residents saved approximately $310 billion. In 2015, that amount was $784 billion, about two-and-a-half times greater. Which of the following graphs compares these totals more...

Study smarter with the SolutionInn App