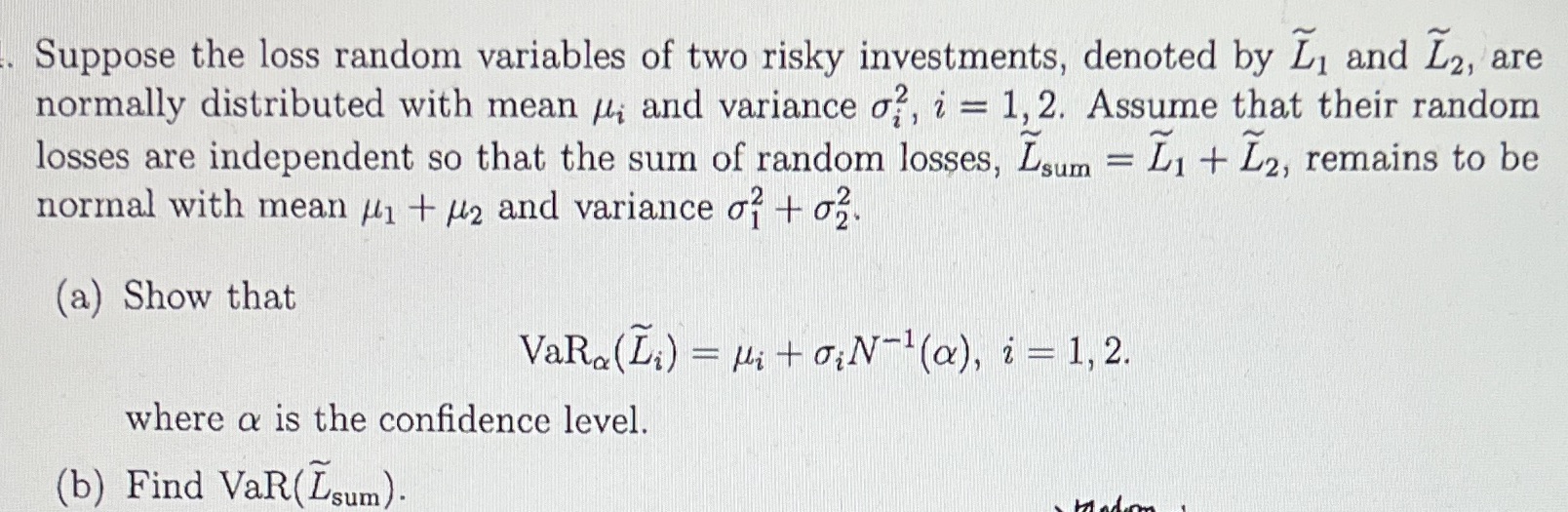

Suppose the loss random variables of two risky investments, denoted by L1 and L2, are normally...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Introduction to Operations Research

ISBN: 978-1259162985

10th edition

Authors: Frederick S. Hillier, Gerald J. Lieberman

Posted Date: