Suppose the market index has a standard deviation of 0.40 and the riskless rate is 5 %

Fantastic news! We've Found the answer you've been seeking!

Question:

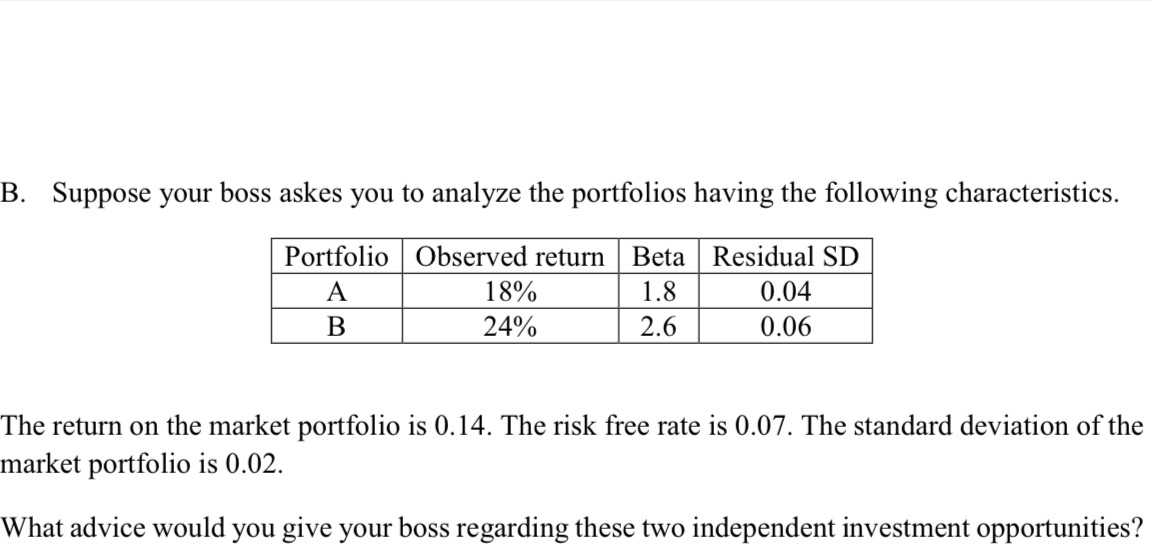

Suppose the market index has a standard deviation of 0.40 and the riskless rate is 5 % . You are given the following information about two stocks X and Y : , and . R=[10%,20%] Cov * (RX, RMarket) = 0.096 Cov * (RY, RMarket) = 0.240 Suppose firm - specific errors are independent and identically distributed with a mean of zero and standard deviation of 0.5 . a ) What are the standard deviations of stocks X and Y ? b ) You were to construct a portfolio P with the following proportions : 20 % in Stockx , 50 % in Stock Y , and 30 % in T - bills . Find the market return and the beta of portfolio P.

Expert Answer:

Related Book For

Statistics The Exploration & Analysis Of Data

ISBN: 9780840058010

7th Edition

Authors: Roxy Peck, Jay L. Devore

Posted Date: