Question: Suppose there are two bonds, a 3-year bond with a coupon rate of 5% that pays interest twice a year, and a 10-year bond with

Suppose there are two bonds, a 3-year bond with a coupon rate of 5% that pays interest twice a year, and a 10-year bond with a coupon rate of 9% that pays interest once a year. Assuming that the current spot interest rate (discount rate) is 12% and the interest rate curve is horizontal, the investor's liability is paid in 7-year installments, and the annual payment is $1000. How do you achieve immunity?

Suppose there are three bonds, a 10-year bond with a coupon rate of 6.7%, which pays interest once a year; another 15-year bond with a coupon rate of 6.988%, which pays interest once a year; and a 30-year bond, The coupon rate is 5.9%, and interest is paid annually. The investor's liability is in 10-year installments of $1,000 per year. Assuming that the current spot interest rate (discount rate) is 6% and the interest rate curve is flat, how to achieve immunity?

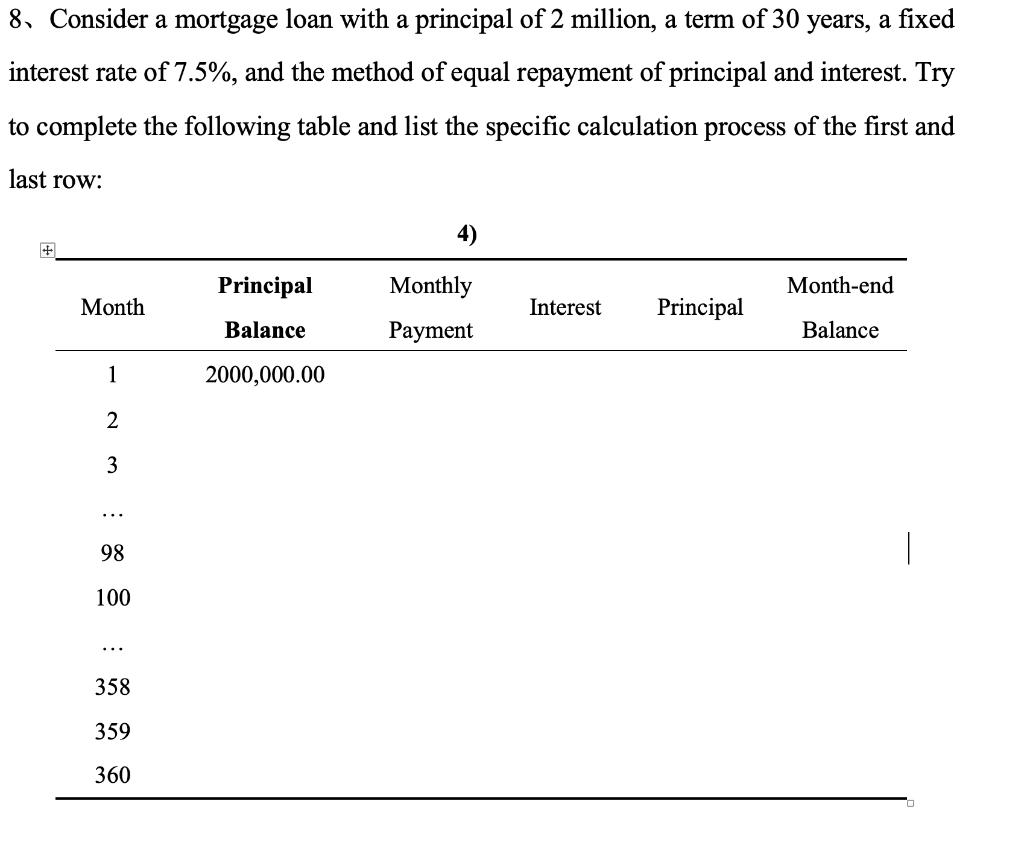

8. Consider a mortgage loan with a principal of 2 million, a term of 30 years, a fixed interest rate of 7.5%, and the method of equal repayment of principal and interest. Try to complete the following table and list the specific calculation process of the first and last row: Month 1 2 3 98 100 358 359 360 Principal Balance 2000,000.00 4) Monthly Payment Interest Principal Month-end Balance

Step by Step Solution

3.52 Rating (176 Votes )

There are 3 Steps involved in it

1 To achieve immunity in the first example the investor should construct a portfolio of the two bonds purchasing the 3year bond with a coupon rate of ... View full answer

Get step-by-step solutions from verified subject matter experts