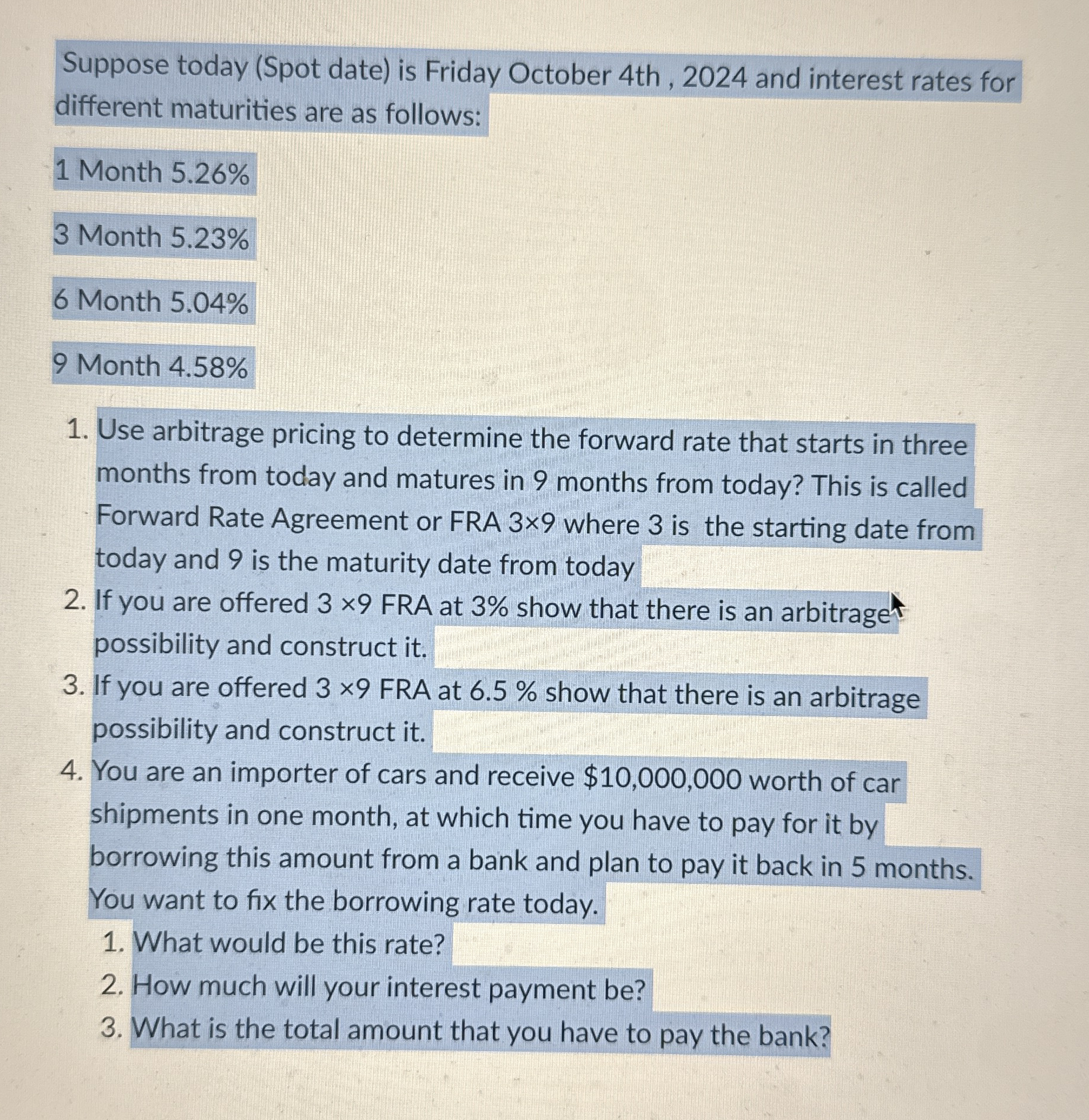

Question: Suppose today ( Spot date ) is Friday October 4 th , 2 0 2 4 and interest rates for different maturities are as follows:

Suppose today Spot date is Friday October th and interest rates for different maturities are as follows:

Month

Month

Month

Month

Use arbitrage pricing to determine the forward rate that starts in three months from today and matures in months from today? This is called Forward Rate Agreement or FRA where is the starting date from today and is the maturity date from today

If you are offered FRA at show that there is an arbitrage possibility and construct it

If you are offered FRA at show that there is an arbitrage possibility and construct it

You are an importer of cars and receive $ worth of car shipments in one month, at which time you have to pay for it by borrowing this amount from a bank and plan to pay it back in months. You want to fix the borrowing rate today.

What would be this rate?

How much will your interest payment be

What is the total amount that you have to pay the bank?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock