Question: Suppose we have the following information: Debt Expected return 7% Standard deviation 14% Correlation -100% Equity 12% 25% What's the expected return of the

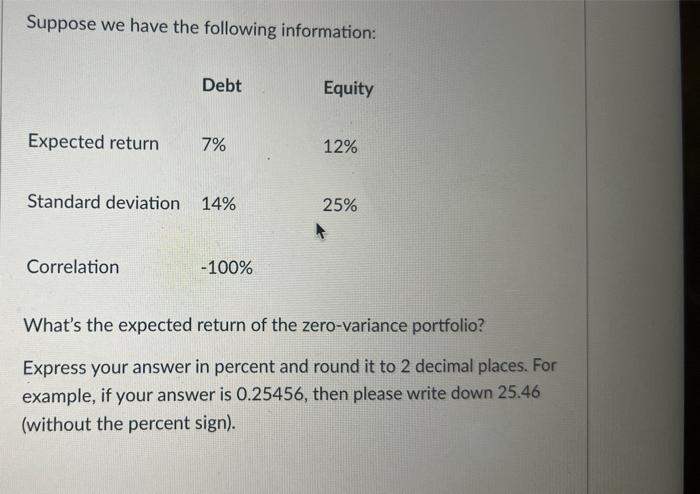

Suppose we have the following information: Debt Expected return 7% Standard deviation 14% Correlation -100% Equity 12% 25% What's the expected return of the zero-variance portfolio? Express your answer in percent and round it to 2 decimal places. For example, if your answer is 0.25456, then please write down 25.46 (without the percent sign).

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

The expected return of a zerovariance portfolio can be calculate... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock