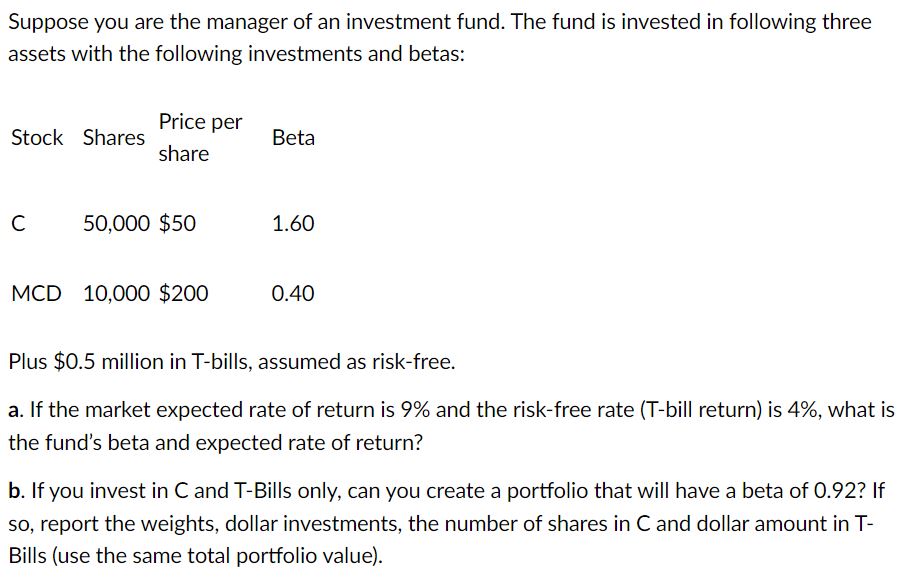

Suppose you are the manager of an investment fund. The fund is invested in following three...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a To calculate the funds beta and expected rate of return we need to use the formula for the expected return of a portfolio Expected Return RiskFree R... View the full answer

Related Book For

Financial Theory and Corporate Policy

ISBN: 978-0321127211

4th edition

Authors: Thomas E. Copeland, J. Fred Weston, Kuldeep Shastri

Posted Date: