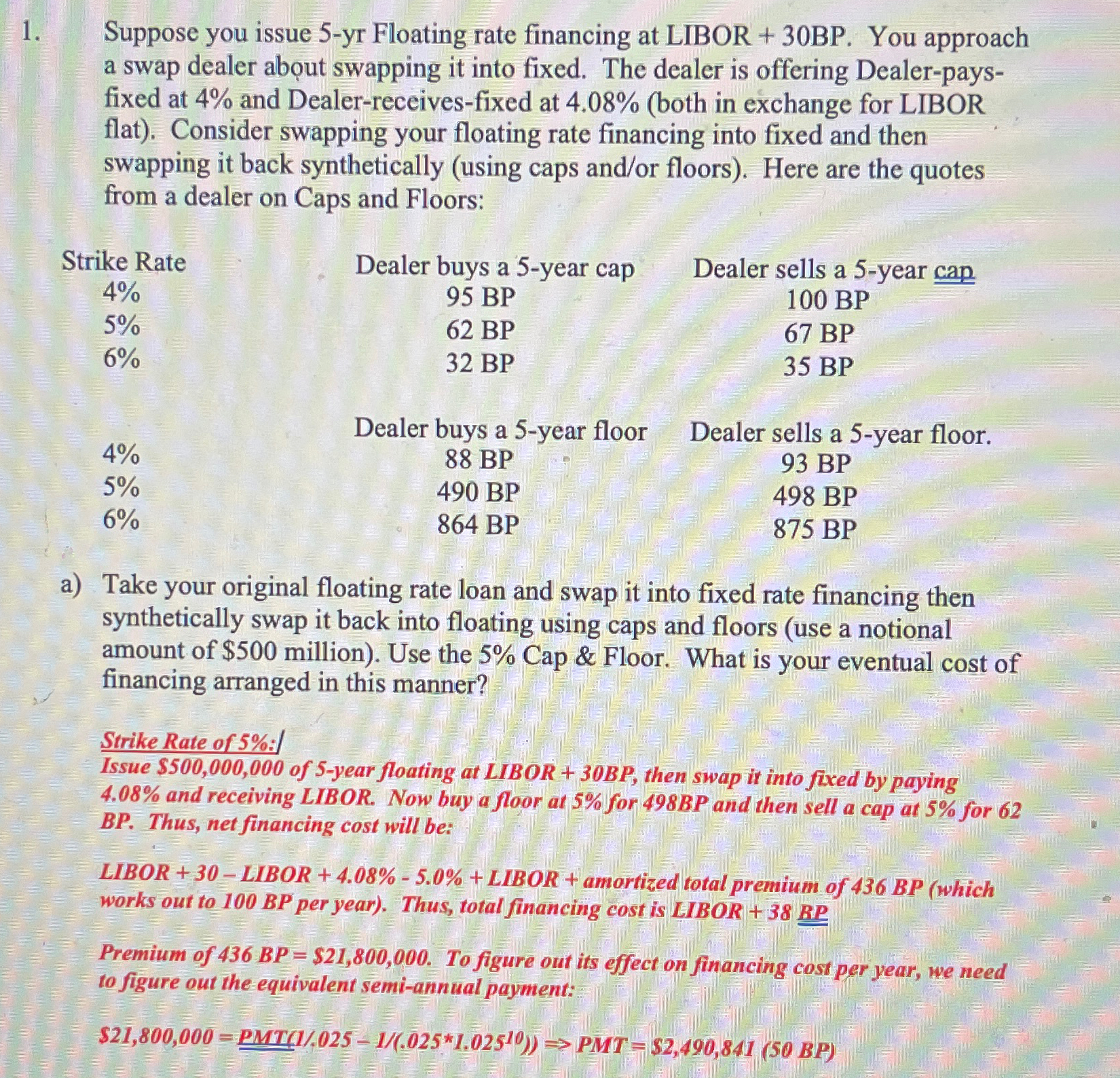

Question: Suppose you issue 5 - y r Floating rate financing at LIBOR + 3 0 BP . You approach a swap dealer about swapping it

Suppose you issue Floating rate financing at LIBOR BP You approach a swap dealer about swapping it into fixed. The dealer is offering Dealerpaysfixed at and Dealerreceivesfixed at both in exchange for LIBOR flat Consider swapping your floating rate financing into fixed and then swapping it back synthetically using caps andor floors Here are the quotes from a dealer on Caps and Floors:

tableStrike Rate,Dealer buys a year cap,Dealer sells a year cap

Note: use for amortization

How was bo per year found? Please show step by step work

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock