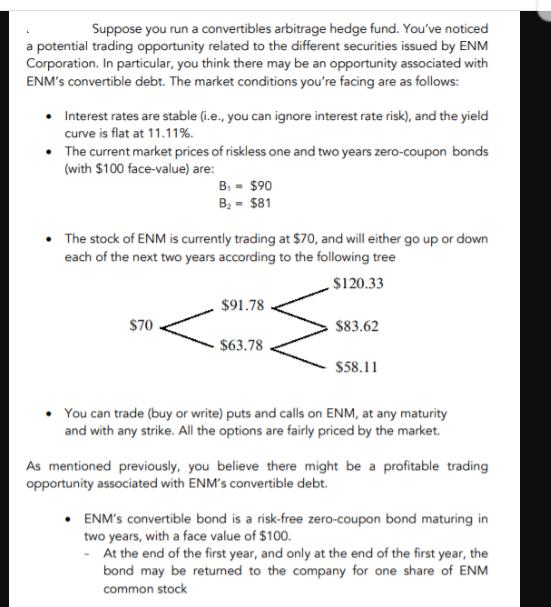

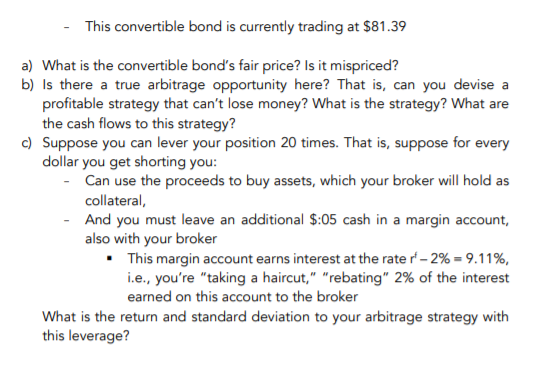

Suppose you run a convertibles arbitrage hedge fund. You've noticed a potential trading opportunity related to...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a The fair price of the convertible bond is 1yr 05 90 05 81 855 2yr 05 81 05 81 81 Since the bond is ... View the full answer

Related Book For

Data Analysis and Decision Making

ISBN: 978-0538476126

4th edition

Authors: Christian Albright, Wayne Winston, Christopher Zappe

Posted Date: