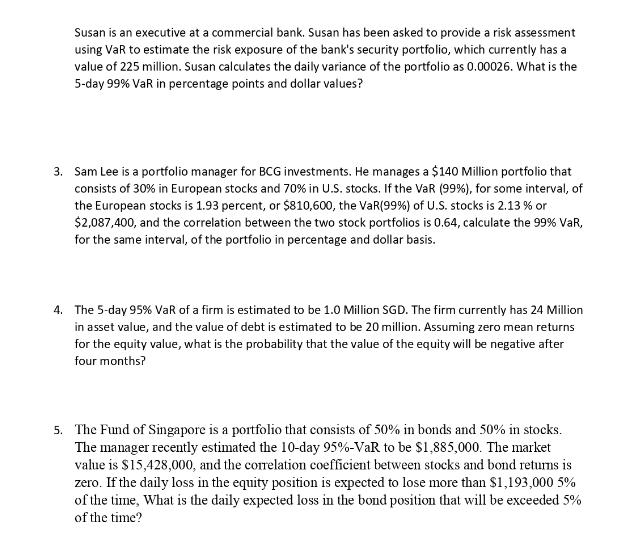

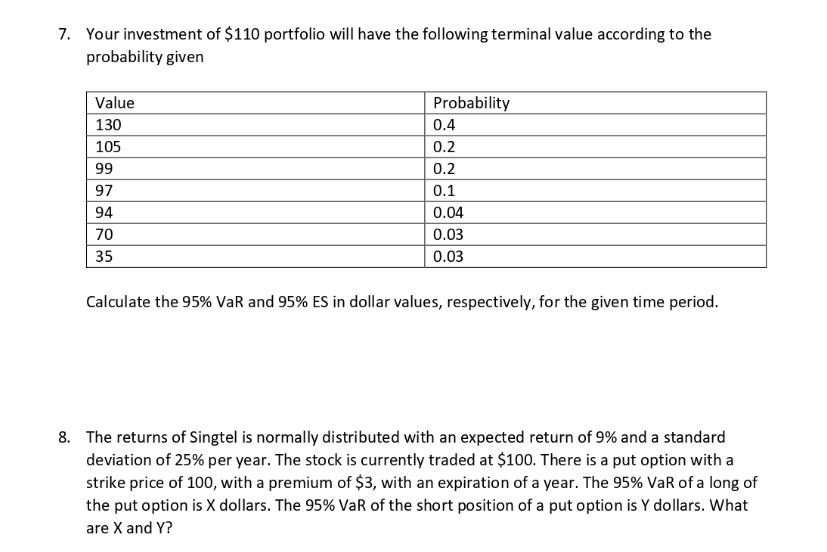

Susan is an executive at a commercial bank. Susan has been asked to provide a risk...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

SOLUTION 1 To calculate the 5day 99 VaR in percentage points we can use the formula VaR portfolio value sqrtvariance zscore where zscore inverse of the cumulative distribution function of the standard ... View the full answer

Related Book For

Posted Date: