Question: Table 1 - Single Index Model Regression Results Stock A Stock B Stock C a 1% 0.6% 0.2% 1 1.6 1 o () 4.1% 4.8%

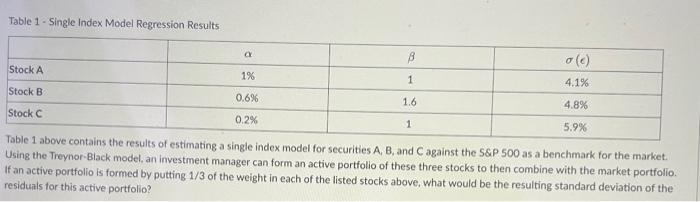

Table 1 - Single Index Model Regression Results Stock A Stock B Stock C a 1% 0.6% 0.2% 1 1.6 1 o () 4.1% 4.8% 5.9% Table 1 above contains the results of estimating a single index model for securities A, B, and C against the S&P 500 as a benchmark for the market. Using the Treynor-Black model, an investment manager can form an active portfolio of these three stocks to then combine with the market portfolio. If an active portfolio is formed by putting 1/3 of the weight in each of the listed stocks above, what would be the resulting standard deviation of the residuals for this active portfolio?

Table 1 - Single Index Model Regression Results Table 1 above contains the results of estimating a single index model for securities A, B, and C against the S\&P 500 as a benchmark for the market. Using the Treynor-Black model, an investment manager can form an active portfolio of these three stocks to then combine with the market portfolio. If an active portfolio is formed by putting 1/3 of the weight in each of the listed stocks above, what would be the resulting standard deviation of the residuals for this active portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock