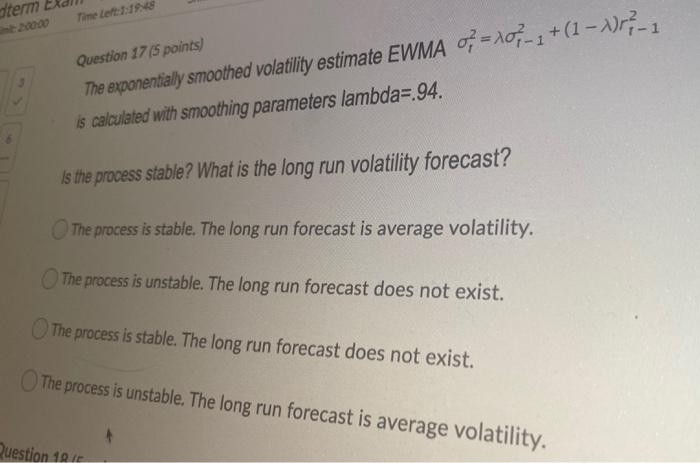

Question: term Time Left Question 17 (5 points) The exponentially smoothed volatility estimate EWMA 0; = 107-1 + (1 - 1)-7-1 is calculated with smoothing parameters

term Time Left Question 17 (5 points) The exponentially smoothed volatility estimate EWMA 0; = 107-1 + (1 - 1)-7-1 is calculated with smoothing parameters lambda=.94. Is the process stable? What is the long run volatility forecast? The process is stable. The long run forecast is average volatility. The process is unstable. The long run forecast does not exist. The process is stable. The long run forecast does not exist. The process is unstable. The long run forecast is average volatility. Question 1 IP

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock