Question: Terms: Receive fixed rate every 6 months and pay 3ML for 2 years Use the market data provided below to construct a US$ interest-rate swap

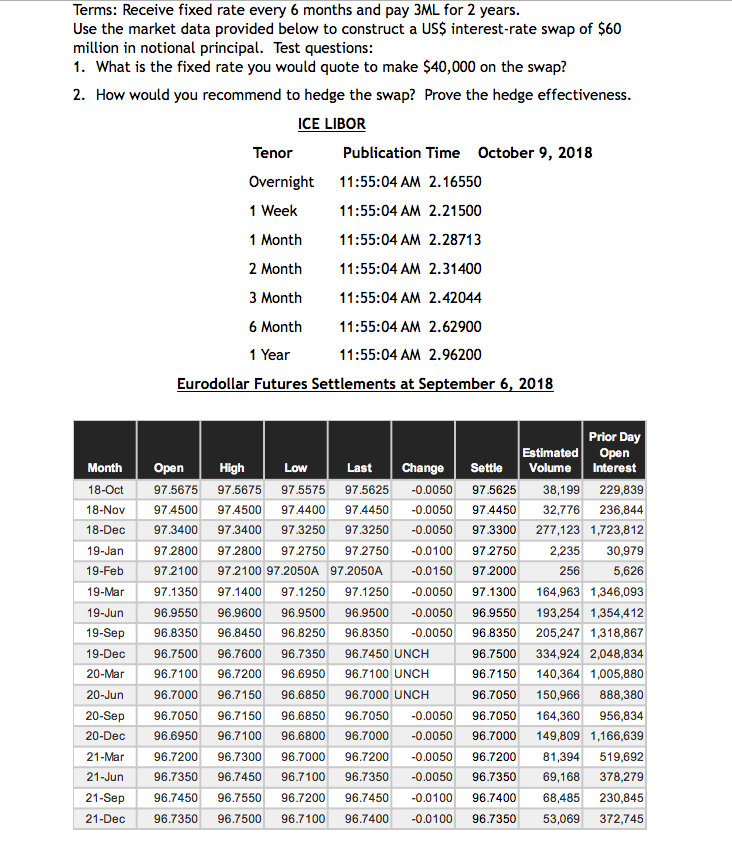

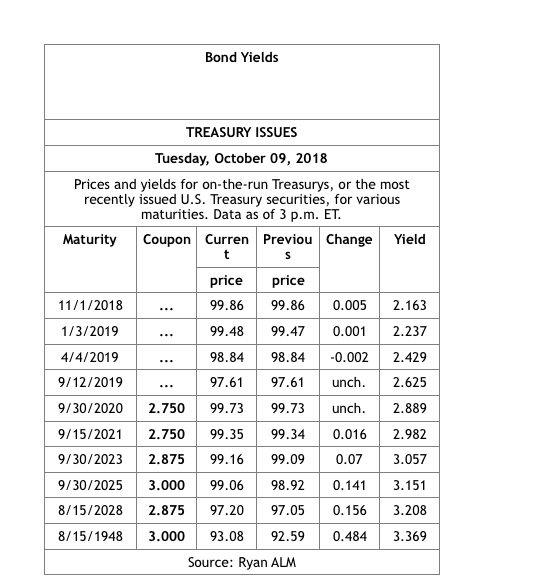

Terms: Receive fixed rate every 6 months and pay 3ML for 2 years Use the market data provided below to construct a US$ interest-rate swap of $60 million in notional principal. Test questions: 1. What is the fixed rate you would quote to make $40,000 on the swap? 2. How would you recommend to hedge the swap? Prove the hedge effectiveness ICE LIBOR Tenor Overnight 1 Week 1 Month 2 Month 3 Month 6 Month 1 Year Publication Time October 9, 2018 11:55:04 AM 2.16550 11:55:04 AM 2.21500 11:55:04 AM 2.28713 11:55:04 AM 2.31400 11:55:04 AM 2.42044 11:55:04 AM 2.62900 11:55:04 AM 2.96200 Eurodollar Futures Settlements at September 6, 2018 Prior Day Estimated Open Month OpenHigh 18-Oct 18-Nov 18-Dec 19-Jan 19-Feb 19-Mar97.1350 97.1400 97.1250 97.1250-0.0050 97.1300 164,963 1,346,093 19-Jun 96.9550 96.9600 96.9500 96.95000.0050 96.9550 193,254 1,354,412 19-Sep96.8350 96.8450 96.8250 96.8350-0.0050 96.8350 205,247 1,318,867 19-Dec Low Last Change Settle Volume Interest 97.5675 97.5675 97.5575 97.5625 -0.0050 97.5625 38,199 229,839 974500 974500 974400 97 4450 0.0050 97.4450 32,776 236,844 97.3400 97.3400 97.3250 97.3250-0.0050 973300 277,123 1,723,812 97.2800 97.2800 97.2750 97.2750 0.0100 97.2750 97.2100 97.2100 97.2050A 97.2050A 2,235 30,979 5,626 0.0150 97.2000 256 96.7500 96.7600 96.7350 96.7450 UNCH 96.7100 96.7200 96.6950 96.7100 UNCH 96.7000 96.7150 96.6850 96.7000 UNCH 96.7500 334,924 2,048,834 96.7150140,364 1,005,880 96.7050 150,966 888,380 20-Jun 20-Sep96.7050 96.7150 96.6850 96.7050-0.0050 96.7050 164,360 956,834 20-Dec 21-Mar96.7200 96.7300 96.7000 96.7200 -0.0050 96.7200 81,394519,692 21-Jun96.7350 96.7450 96.7100 96.7350 -0.0050 96.7350 69,168 378,279 21-Sep 21-Dec 96.6950 96.7100 96.6800 96.7000 0.0050 96.7000 149,809 1,166,639 96.7450 96.7550 96.7200 96.7450 -0.0100 96.7400 68,485 230,845 96.7350 96.7500 96.7100 96.7400 0.0100 96.7350 53,069 372,745 Terms: Receive fixed rate every 6 months and pay 3ML for 2 years Use the market data provided below to construct a US$ interest-rate swap of $60 million in notional principal. Test questions: 1. What is the fixed rate you would quote to make $40,000 on the swap? 2. How would you recommend to hedge the swap? Prove the hedge effectiveness ICE LIBOR Tenor Overnight 1 Week 1 Month 2 Month 3 Month 6 Month 1 Year Publication Time October 9, 2018 11:55:04 AM 2.16550 11:55:04 AM 2.21500 11:55:04 AM 2.28713 11:55:04 AM 2.31400 11:55:04 AM 2.42044 11:55:04 AM 2.62900 11:55:04 AM 2.96200 Eurodollar Futures Settlements at September 6, 2018 Prior Day Estimated Open Month OpenHigh 18-Oct 18-Nov 18-Dec 19-Jan 19-Feb 19-Mar97.1350 97.1400 97.1250 97.1250-0.0050 97.1300 164,963 1,346,093 19-Jun 96.9550 96.9600 96.9500 96.95000.0050 96.9550 193,254 1,354,412 19-Sep96.8350 96.8450 96.8250 96.8350-0.0050 96.8350 205,247 1,318,867 19-Dec Low Last Change Settle Volume Interest 97.5675 97.5675 97.5575 97.5625 -0.0050 97.5625 38,199 229,839 974500 974500 974400 97 4450 0.0050 97.4450 32,776 236,844 97.3400 97.3400 97.3250 97.3250-0.0050 973300 277,123 1,723,812 97.2800 97.2800 97.2750 97.2750 0.0100 97.2750 97.2100 97.2100 97.2050A 97.2050A 2,235 30,979 5,626 0.0150 97.2000 256 96.7500 96.7600 96.7350 96.7450 UNCH 96.7100 96.7200 96.6950 96.7100 UNCH 96.7000 96.7150 96.6850 96.7000 UNCH 96.7500 334,924 2,048,834 96.7150140,364 1,005,880 96.7050 150,966 888,380 20-Jun 20-Sep96.7050 96.7150 96.6850 96.7050-0.0050 96.7050 164,360 956,834 20-Dec 21-Mar96.7200 96.7300 96.7000 96.7200 -0.0050 96.7200 81,394519,692 21-Jun96.7350 96.7450 96.7100 96.7350 -0.0050 96.7350 69,168 378,279 21-Sep 21-Dec 96.6950 96.7100 96.6800 96.7000 0.0050 96.7000 149,809 1,166,639 96.7450 96.7550 96.7200 96.7450 -0.0100 96.7400 68,485 230,845 96.7350 96.7500 96.7100 96.7400 0.0100 96.7350 53,069 372,745

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts