Question: The 2012 Greek Default and Subsequent DebtRestructuring6 In March and April 2012 Greece defaulted on its debt by swapping its outstanding obligations for new obligations

The 2012 Greek Default and Subsequent DebtRestructuring6

In March and April 2012 Greece defaulted on its debt by swapping its outstanding obligations for new obligations of much lesser face value. For each euro of face value outstanding, a holder of Greek debt was given the following securities with an issue date of 12 March 2012.

Two European Financial Stability Fund (EFSF) notes. Each note had a face value of7.57.5. The first note paid an annual coupon (on the anniversary of the issue date) of 0.4% and matured on 12 March 2013. The second note paid an annual coupon of 1% and matured on 12 March 2014.

A series of bonds issued by the Greek government with a combined face value of31.531.5. The simplest way to characterize these bonds is as a single bond paying anannual coupon (onDecember 12 of each year) of 2% for years 2012-2015, 3% for years 2016-2020, 3.65% for 2021, and 4.3% thereafter. Principal is repaid in 20 equal installments (that is, 5% of face value) in December in the years 2023-2042.

Other securities that were worth little.

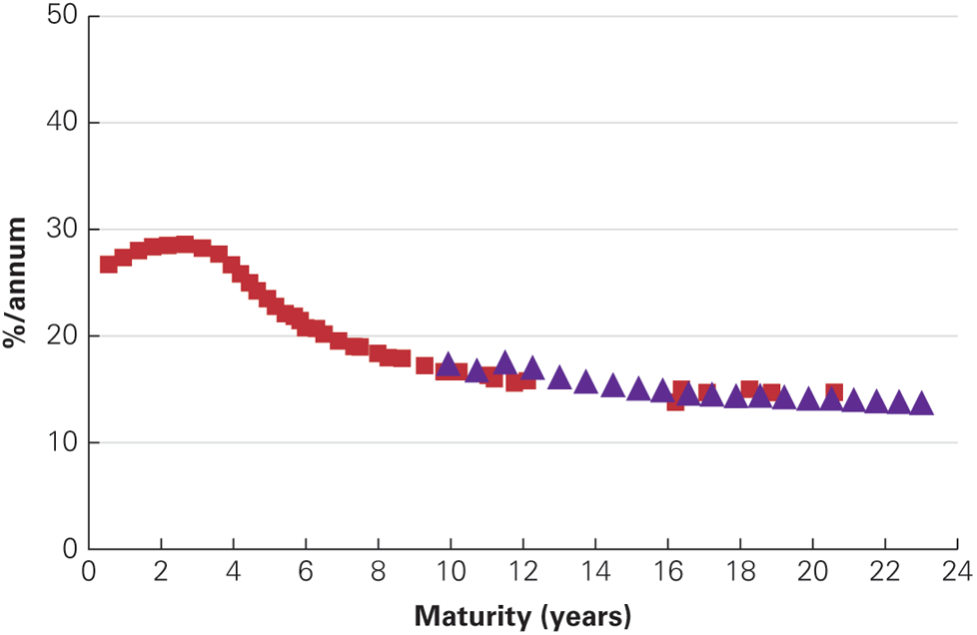

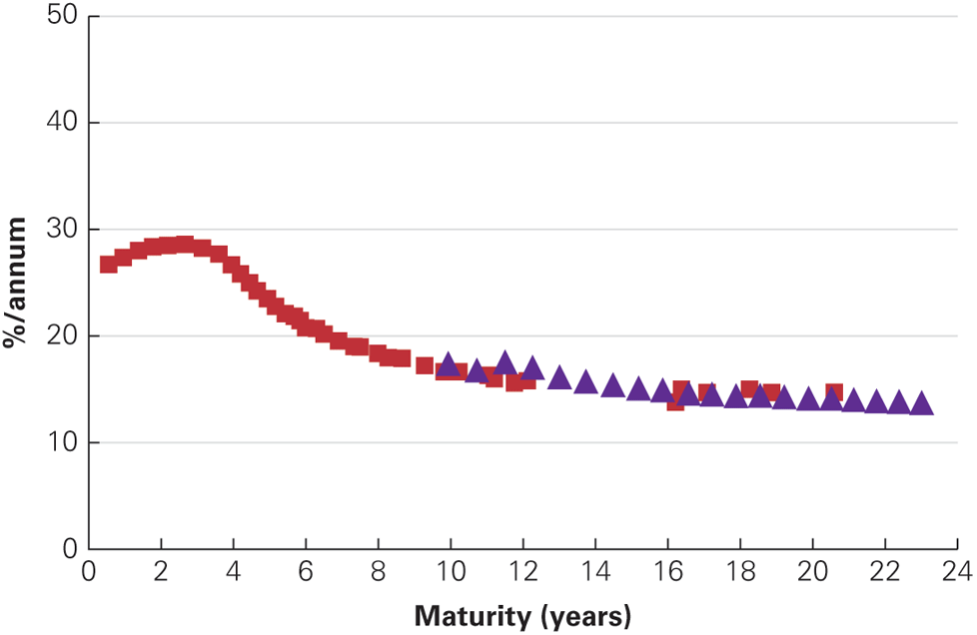

An important feature of this swap is that the same deal was offered to all investors, regardless of which bonds they were holding. That meant that the loss to different investors was not the same.To understand why, begin by calculating the present value of what every investor received. For simplicity, assume that the coupons on the EFSF notes were issued at market rates so they traded at par. Next, put all the promised payments of the bond series on a timeline.Figure6.7shows the imputed yields on Greek debt that prevailedafter the debt swapwas announced. Assume the yields inFigure6.7are yields on zero coupon bonds maturing in the 23 years following the debt swap, and use them to calculate the present value of all promised payments on March 12, 2012.

Figure6.7 - Imputed Greek Government Yield Curve on March 12, 2012

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts