Question: The answer to the first question is 13.20% and the second question is -0.45% are both wrong. Can someone please tell me why? Use these

The answer to the first question is 13.20% and the second question is -0.45% are both wrong. Can someone please tell me why?

The answer to the first question is 13.20% and the second question is -0.45% are both wrong. Can someone please tell me why?

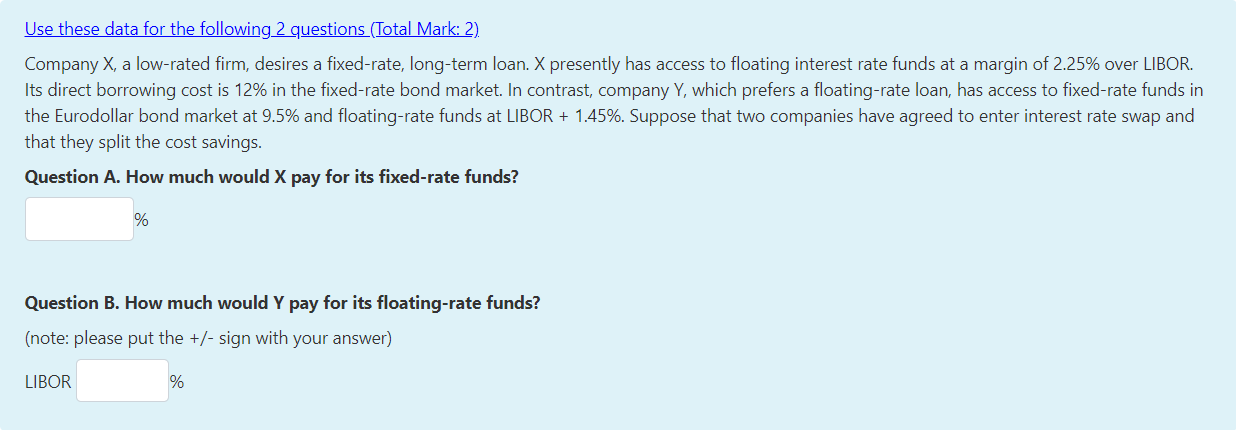

Use these data for the following 2 questions (Total Mark: 2). Company X, a low-rated firm, desires a fixed-rate, long-term loan. X presently has access to floating interest rate funds at a margin of 2.25% over LIBOR. Its direct borrowing cost is 12% in the fixed-rate bond market. In contrast, company Y, which prefers a floating-rate loan, has access to fixed-rate funds in the Eurodollar bond market at 9.5% and floating-rate funds at LIBOR + 1.45%. Suppose that two companies have agreed to enter interest rate swap and that they split the cost savings. Question A. How much would X pay for its fixed-rate funds? Question B. How much would Y pay for its floating-rate funds? (note: please put the +/- sign with your answer) LIBOR

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts