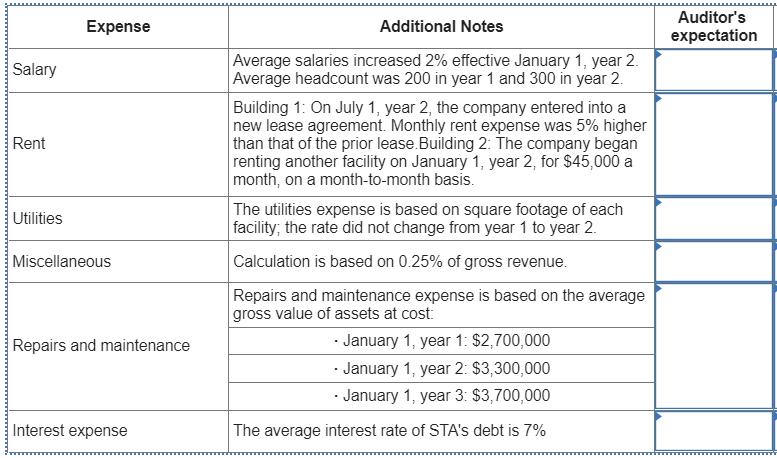

The auditors of STA, Inc., a calendar-year corporation, obtained the selected information for years 1 and 2

Fantastic news! We've Found the answer you've been seeking!

Question:

The auditors of STA, Inc., a calendar-year corporation, obtained the selected information for years 1 and 2 located in the exhibit below.

| Selected information | Year 2 | Year 1 | |||

| Gross revenue | $ | 63,000,000 | $ | 60,000,000 | |

| Net income before taxes | 11,650,000 | 11,000,000 | |||

| Salary expense | 12,500,000 | 8,000,000 | |||

| Rent expense | 1,920,000 | 1,200,000 | |||

| Utilities expense | 155,000 | 120,000 | |||

| Depreciation expense | 705,000 | 675,000 | |||

| Repairs and maintenance | 375,000 | 300,000 | |||

| Interest expense | 523,000 | 338,100 | |||

| Miscellaneous | 151,000 | 135,000 | |||

| Tax expense | 4,325,150 | 3,850,000 | |||

Additionally, the auditors noted the following information:

- STA rents space in an office building:

- Space in Building 1: 25,000 sq. ft.

- On January 1, year 2, the company added a second space:

- Space in Building 2: 11,000 sq. ft.

- The balance of interest-bearing debt outstanding:

- January 1, year 2: $4,830,000

- December 31, year 2: $10,262,000

- The company issued additional debt on July 1, year 2

The auditors are performing analytical procedures relative to the expectations of expenses for year 2 and have established a materiality threshold of 5% of the auditor's expected year 2 amount.

For each of the expenses in column A below, consider the additional notes in column B, and complete the following:

- In "Auditor's expectation" column, enter the auditor's expectation of year 2 expense. (Round all amounts to the nearest dollar.)

- In "Auditor's decision" column, select the auditor's decision as to whether further testing is needed. (Consider each account independently - an option may be used once, more than once, or not at all.)

Expert Answer:

Related Book For

Managerial Accounting An Introduction to Concepts Methods and Uses

ISBN: 978-0324639766

10th Edition

Authors: Michael W. Maher, Clyde P. Stickney, Roman L. Weil

Posted Date: