Question: The Balance Sheet and Segment footnote for Procter and Gamble (P & G) are shown below. Using this information complete the following questions. 1. From

The Balance Sheet and Segment footnote for Procter and Gamble (P & G) are shown below. Using this information complete the following questions.

1. From Appendix 3, the accounting profession requires which companies to report supplemental information regarding operating segments?

2. From Appendix 3, only segments of a certain size must be disclosedquantitative thresholds. List the three criteria.

A.

B.

C.

3. From the footnote. Which of the criteria were met for each of the segments that were reported on by Procter and Gamble during 2018? List all that apply.

- Beauty _________________________

- Grooming______________________________

- Healthcare_____________________________

- Fabric and Home Care________________________

- Baby Care and Family Care____________________

4. From Appendix 3, what is the criteria for disclosing a major customer?

5. From the footnote, who is Procter & Gambles major customer?

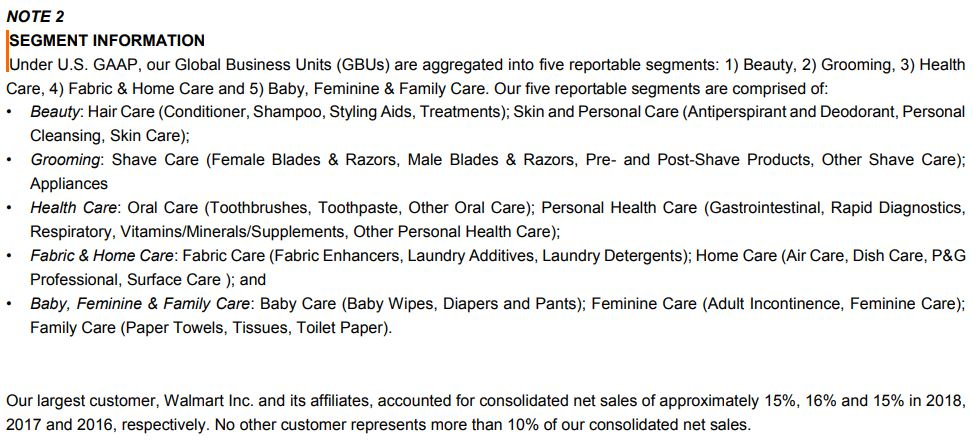

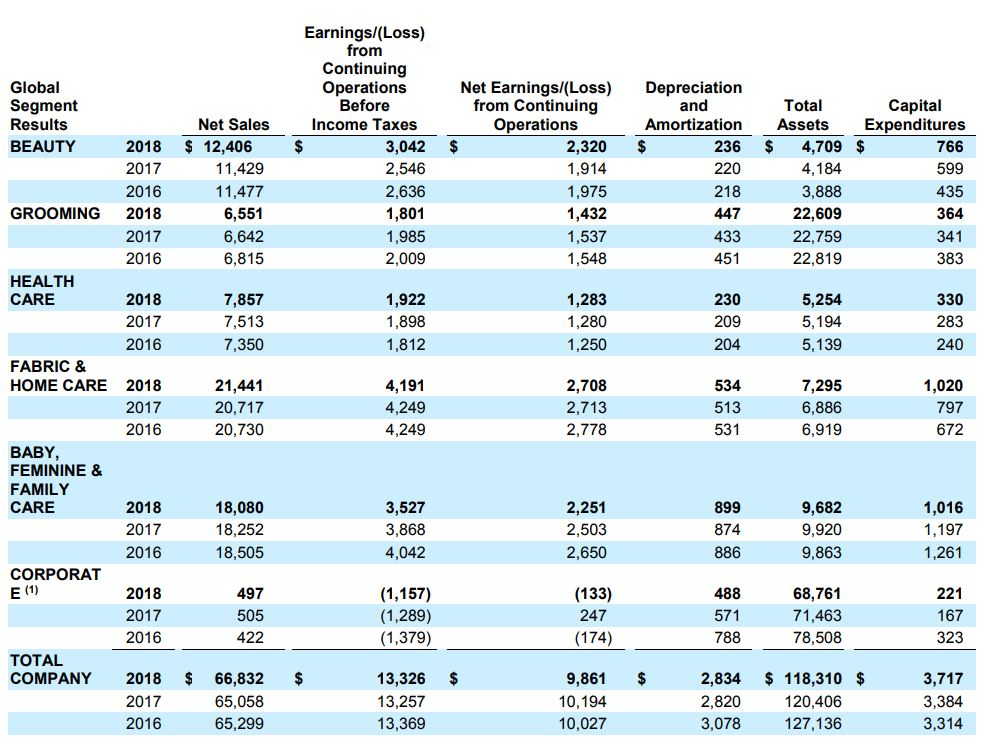

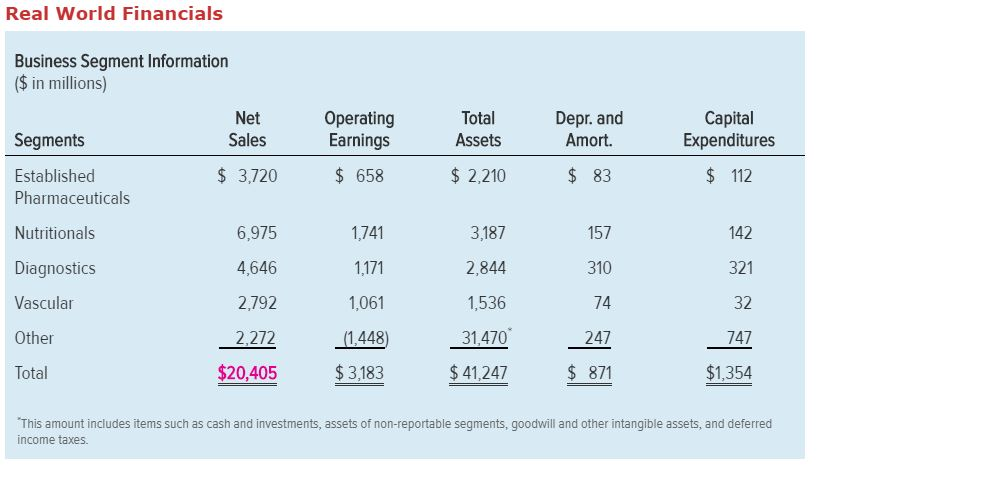

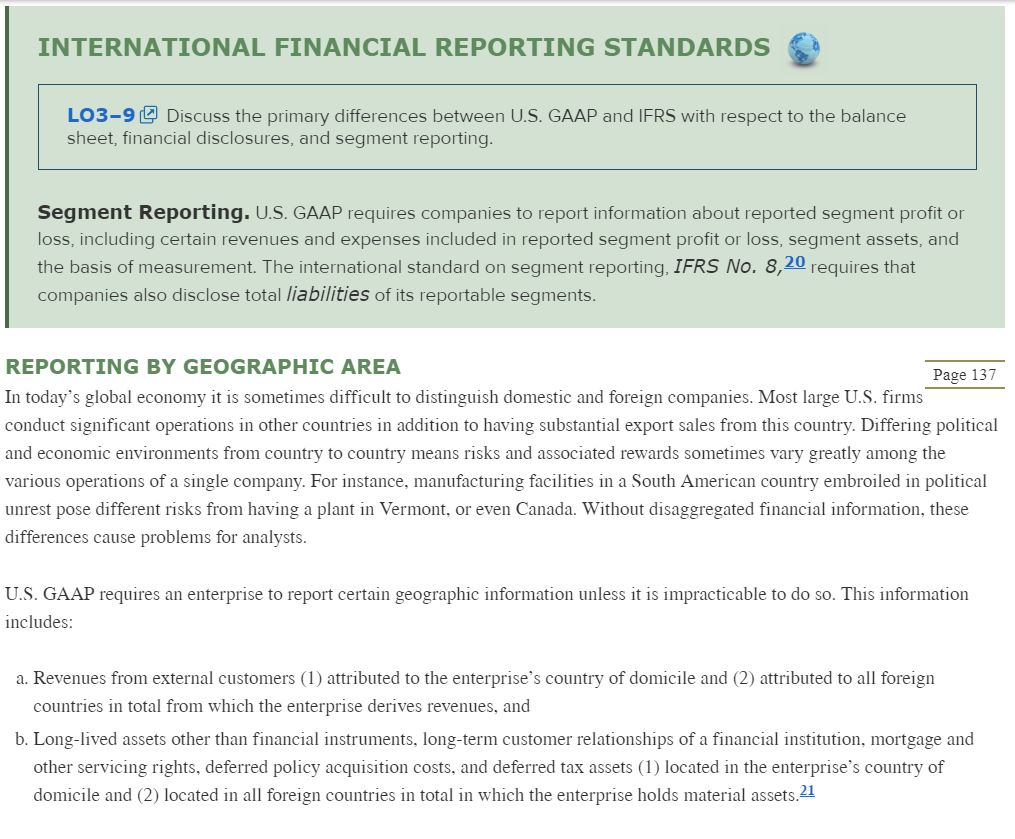

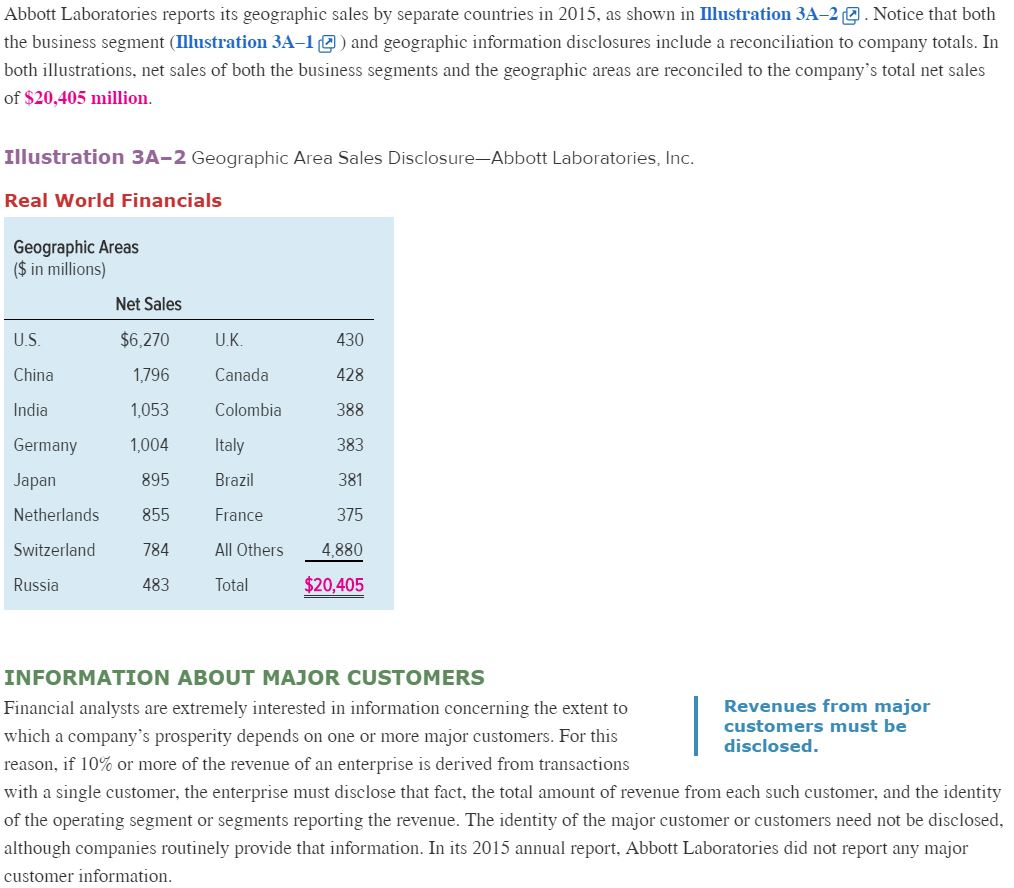

NOTE 2 SEGMENT INFORMATION Under U.S. GAAP, our Global Business Units (GBUs) are aggregated into five reportable segments: 1) Beauty, 2) Grooming, 3) Health Care, 4) Fabric & Home Care and 5) Baby, Feminine & Family Care. Our five reportable segments are comprised of: .Beauty: Hair Care (Conditioner, Shampoo, Styling Aids, Treatments); Skin and Personal Care (Antiperspirant and Deodorant, Personal .Grooming: Shave Care (Female Blades & Razors, Male Blades & Razors, Pre- and Post-Shave Products, Other Shave Care) .Health Care: Oral Care (Toothbrushes, Toothpaste, Other Oral Care); Personal Health Care (Gastrointestinal, Rapid Diagnostics, .Fabric & Home Care: Fabric Care (Fabric Enhancers, Laundry Additives, Laundry Detergents); Home Care (Air Care, Dish Care, P&G .Baby, Feminine & Family Care: Baby Care (Baby Wipes, Diapers and Pants); Feminine Care (Adult Incontinence, Feminine Care) Cleansing, Skin Care) Appliances Respiratory, Vitamins/Minerals/Supplements, Other Personal Health Care); Professional, Surface Care); and Family Care (Paper Towels, Tissues, Toilet Paper) Our largest customer, Walmart Inc. and its affiliates, accounted for consolidated net sales of approximately 15%, 16% and 15% in 2018, 2017 and 2016, respectively. No other customer represents more than 10% of our consolidated net sales. Earnings/(Loss) from Continuing Operations Before ncome Taxes Global Segment Results BEAUTY Net Earnings/(Loss) Depreciation from Continuing Operations and Total Capital Net Sales 2018 $ 12,406 2017 2016 Amortization Assets Expenditures 766 599 435 364 3,042$ 2,546 2,320 $ 236 $ 4,709 $ 11,429 1,975 1,432 1,537 GROOMING 2018 6,551 22,609 22,759 22,819 433 2017 2016 6,642 2,009 HEALTH CARE 2018 2017 2016 1,922 1,898 1,283 1,280 230 209 330 283 FABRIC & HOME CARE 2018 2017 2016 21,441 20,717 20,730 1,020 797 672 2,708 7,295 2,778 BABY FEMININE & FAMILY CARE 2018 2017 2016 18,080 18,252 18,505 2,251 2,503 9,682 9,920 9,863 3,527 4,042 CORPORAT 2018 2017 2016 (1,157) (1,289) 68,761 71,463 78,508 422 788 323 TOTAL 9,861 $ COMPANY 2018 66,832 $ 65,058 65,299 13,326 $ 13,257 13,369 2,834 118,310 $ 2,820 3,078 3,717 2017 2016 120,406 127,136 10,027 The Corporate reportable segment includes depreciation and amortization, total assets and capital expenditures of the Beauty Brands and Batteries businesses prior to their divestiture APPENDIX 3 REPORTING SEGMENT INFORMATION Many companies operate in several business segments as a strategy to achieve growth and to reduce operating risk through diversification. Financial analysis of diversified companies is especially difficult. Consider, for example, a company that operates in several distinct business segments including computer peripherals, home health care systems, textiles, and consumer food products. The results of these distinctly different activities will be aggregated into a single set of financial statements, making difficult an informed projection of future performance. It may well be that the five-year outlook differs greatly among the areas of the economy represented by the different segments. To make matters worse for an analyst, the integrated financial statements do not reveal the relative investments in each of the business segments nor the success the company has had within each area. Given the fact that so many companies these days have chosen to balance their operating risks through diversification, aggregated financial statements pose a widespread problem for analysts, lending and credit officers, and other financial forecasters REPORTING BY OPERATING SEGMENT To address the problem, the accounting profession requires companies engaged in more than one significant business to provide supplemental information concerning individual operating segments. The supplemental disaggregated data do not include complete financial statements for each reportable segment, only certain specified items Segment reporting facilitates the financial statement analysis of diversified companies. WHAT IS A REPORTABLE OPERATING SEGMENT According to U.S. GAAP guidelines, a management approach is used in determining which segments of a company are reportable This approach is based on the way that management organizes the segments within the enterprise for making operating decisions and assessing performance. The segments are, therefore, evident from the structure of the enterprise's internal organization More formally, the following characteristics define an operating segment18 as a component of an enterprise: . That engages in business activities from which it may recognize revenues and incur expenses (including revenues and expenses relating to transactions with other components of the same enterprise) .Whose operating results are regularly reviewed by the enterprise's chief operating decision maker to make decisions Page 136 about resources to be allocated to the segment and assess its performance . For which discrete financial information is available The FASB hopes that this approach provides insights into the risk and opportunities management sees in the various areas of company operations. Also, reporting information based on the enterprise's internal organization should reduce the incremental cost to companies of providing the data. In addition, there are quantitative thresholds for the definition of an operating segment to limit the number of reportable segments. Only segments of material size (10% or more of total company revenues, assets, or net income) must be disclosed. However, a company must account for at least 75% of consolidated revenue through segment disclosures. WHAT AMOUNTS ARE REPORTED BY AN OPERATING SEGMENT? For areas determined to be reportable operating segments, the following disclosures are required: a. General information about the operating segment b. Information about reported segment profit or loss, including certain revenues and expenses included in reported segment profit or loss, segment assets, and the basis of measurement c. Reconciliations of the totals of segment revenues, reported profit or loss, assets, and other significant items to corresponding enterprise amounts d. Interim period information9 Illustration 3A-1 shows the business segment information reported by Abbott Laboratories, in its 2015 annual report Illustration 3A-1 Business Segment Information Disclosure-Abbott Laboratories, Inc. Real World Financials Business Segment Information ($ in millions) Total Assets Net Operating Depr. and Amort. Capital Expenditures Segments Established Pharmaceuticals Nutritionals Diagnostics Vascular Other Total Sales Earnings 3,720 658 $2,210 $ 83 $ 112 6,975 4,646 2,792 2,272 (1,448) 1,741 1,171 1,061 3187 2,844 1,536 157 310 74 247 $ 871 142 321 32 747 $1.354 $20,405 $3,183 41,247 This amount includes items such as cash and investments, assets of non-reportable segments, goodwill and other intangible assets, and deferred income taxes. INTERNATIONAL FINANCIAL REPORTING STANDARDS LO3-9 2 Discuss the primary differences between U.S. GAAP and IFRS with respect to the balance sheet, financial disclosures, and segment reporting Segment Reporting. U.S. GAAP requires companies to report information about reported segment profit o loss, including certain revenues and expenses included in reported segment profit or loss, segment assets, and the basis of measurement. The international standard on segment reporting, IFRS No. 8,20 requires that companies also disclose total liabilities of its reportable segments REPORTING BY GEOGRAPHIC AREA In today's global economy it is sometimes difficult to distinguish domestic and foreign companies. Most large U.S. firms conduct significant operations in other countries in addition to having substantial export sales from this country. Differing political and economic environments from country to country means risks and associated rewards sometimes vary greatly among the various operations of a single company. For instance, manufacturing facilities in a South American country embroiled in political unrest pose different risks from having a plant in Vermont, or even Canada. Without disaggregated financial information, these differences cause problems for analysts. Page 137 U.S. GAAP requires an enterprise to report certain geographic information unless it is impracticable to do so. This information includes a. Revenues from external customers (1) attributed to the enterprise's country of domicile and (2) attributed to all foreign countries in total from which the enterprise derives revenues, and b. Long-lived assets other than financial instruments, long-term customer relationships of a financial institution, mortgage and other servicing rights, deferred policy acquisition costs, and deferred tax assets (1) located in the enterprise's country of domicile and (2) located in all foreign countries in total in which the enterprise holds material assets.21 Abbott Laboratories reports its geographic sales by separate countries in 2015, as shown in Illustration 3A-2Notice that both the business segment llustration 3A-1 and geographic information disclosures include a reconciliation to company totals. In both illustrations, net sales of both the business segments and the geographic areas are reconciled to the company's total net sales of $20,405 millionn Illustration 3A-2 Geographic Area Sales Disclosure-Abbott Laboratories, Inc Real World Financials Geographic Areas $ in millions Net Sales $6,270 U.K U.S China India Germany 1004 It Japan Netherlands Switzerland Russia 430 428 388 383 381 375 All Others 4880 $20,405 1,796 Canada 1,053 Colombi 895 855 784 483 razi France Total INFORMATION ABOUT MAJOR CUSTOMERS Financial analysts are extremely interested in information concerning the extent to which a company's prosperity depends on one or more major customers. For this reason, if 10% or more of the revenue of an enterprise is derived from transactions with a single customer, the enterprise must disclose that fact, the total amount of revenue from each such customer, and the identity of the operating segment or segments reporting the revenue. The identity of the major customer or customers need not be disclosed, although companies routinely provide that information. In its 2015 annual report, Abbott Laboratories did not report any major customer information Revenues from major customers must be disclosed. However, in its 2015 segment disclosures, Lockheed Martin Corporation reports that the US government accounts for 78% of its revenues. Many companies in the defense industry derive substantial portions of their revenues from contracts with the Defense Department. When cutbacks occur in national defense or in specific defense systems, the impact on a company's operations can be considerable

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts