1. The current stock price is $80. The stock pays a dividend of $2 every quarter. The...

Question:

1. The current stock price is $80. The stock pays a dividend of $2 every quarter. The risk-free rate is 4%. Over each of the next three-month periods the stock could go up by 10% (u=1.1) or down by 5% (d=.95). The option expires in six months after the second dividend is paid. What is the price of the stock at maturity if stock goes down in the first period and down in the second period? (Round to 2 decimal places)

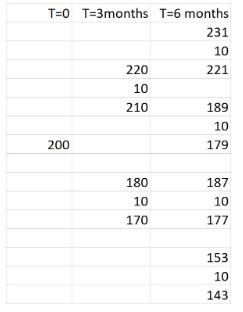

2. The current stock price is $200. The stock pays a dividend of $10 every quarter. The risk-free rate is 8%. Over each of the next three-month periods the stock could go up by 10% (u=1.1) or down by 10% (d=.90). The option expires in six months after the second dividend is paid. The price chart is given below.

a. What is the price of an European Style Call with a strike of $210? (Round to 2 decimal places)

b. What is the price of an American Style Call with a strike of $210? (Round to 2 decimal places)

c. What is the price of an European Style Put with a strike of $210? (Round to 2 decimal places)

d. What is the price of an American Style Put with a strike of $210? (Round to 2 decimal places)

Expert Answer:

a What is the price of an European Style Call with a strike of 210 Round to 2 decimal places ANS WER ... View the full answer

Financial management theory and practice

ISBN: 978-0324422696

12th Edition

Authors: Eugene F. Brigham and Michael C. Ehrhardt