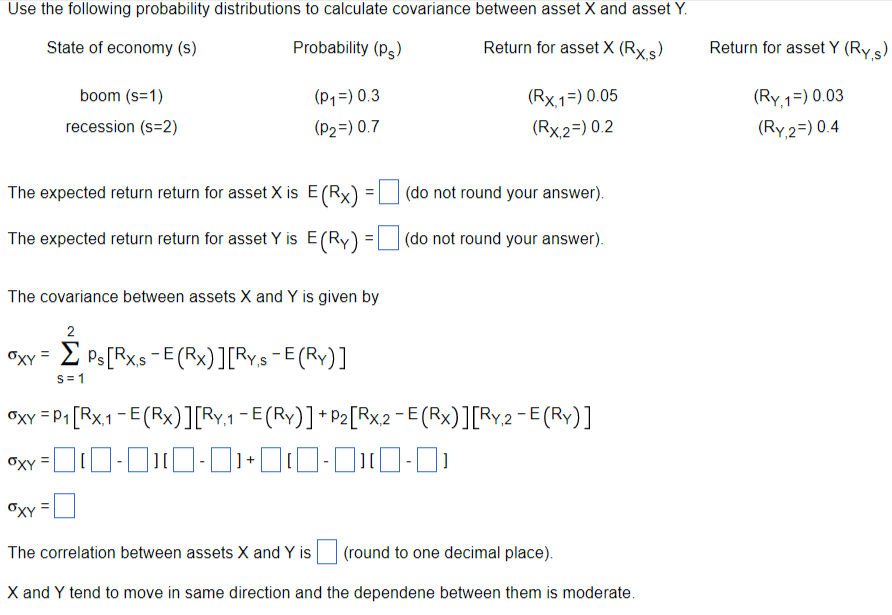

Question: The expected return return for asset X is E(RX)= (do not round your answer). The expected return return for asset Y is E(RY)= (do not

The expected return return for asset X is E(RX)= (do not round your answer). The expected return return for asset Y is E(RY)= (do not round your answer). The covariance between assets X and Y is given by XY=s=12pS[RX,sE(RX)][RY,sE(RY)]XY=p1[RX,1E(RX)][RY,1E(RY)]+p2[RX,2E(RX)][RY,2E(RY)]XY=[][]+[][]XY= The correlation between assets X and Y is (round to one decimal place). X and Y tend to move in same direction and the dependene between them is moderate

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock