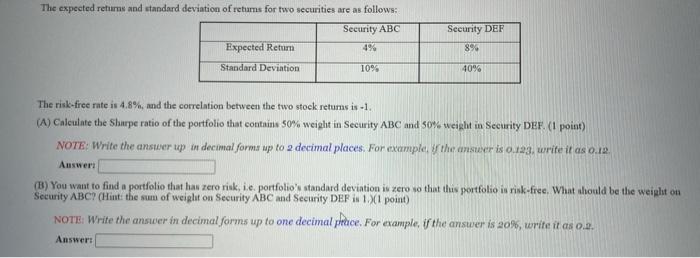

Question: The expected returns and standard deviation of returns for two securities are as follows: Security DEF Security ABC 4% Expected Return 894 Standard Deviation 10%

The expected returns and standard deviation of returns for two securities are as follows: Security DEF Security ABC 4% Expected Return 894 Standard Deviation 10% 40% The risk-free rate is 4.8%, and the correlation between the two stock returns is.1. (A) Caleulate the Shurpe ratio of the portfolio that contains 50% weight in Security ABC and 50% weight in Security DEF. (1 point) NOTE: Write the answer up in decimal forms up to 2 decimal places. For example, the answer is 129, write it as 0.12. Answer (B) You want to find a portfolio that has zero rink, i.e. portfolio's standard deviation is zero so that this portfolio in risk-free. What should be the weight on Security ABC (Hint: the sum of weight on Security ABC and Security DEF is 1.1 point) NOTE: Write the answer in decimal forms up to one decimal place. For example, if the ansuser is 20%, write it as 0.1. Answers

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts