Question: The first picture is the question I need to be solved Here I will attach a similar question, but with different numbers and I will

The first picture is the question I need to be solved

Here I will attach a similar question, but with different numbers and I will attach its solution. So, use them to solve the question on the first picture.

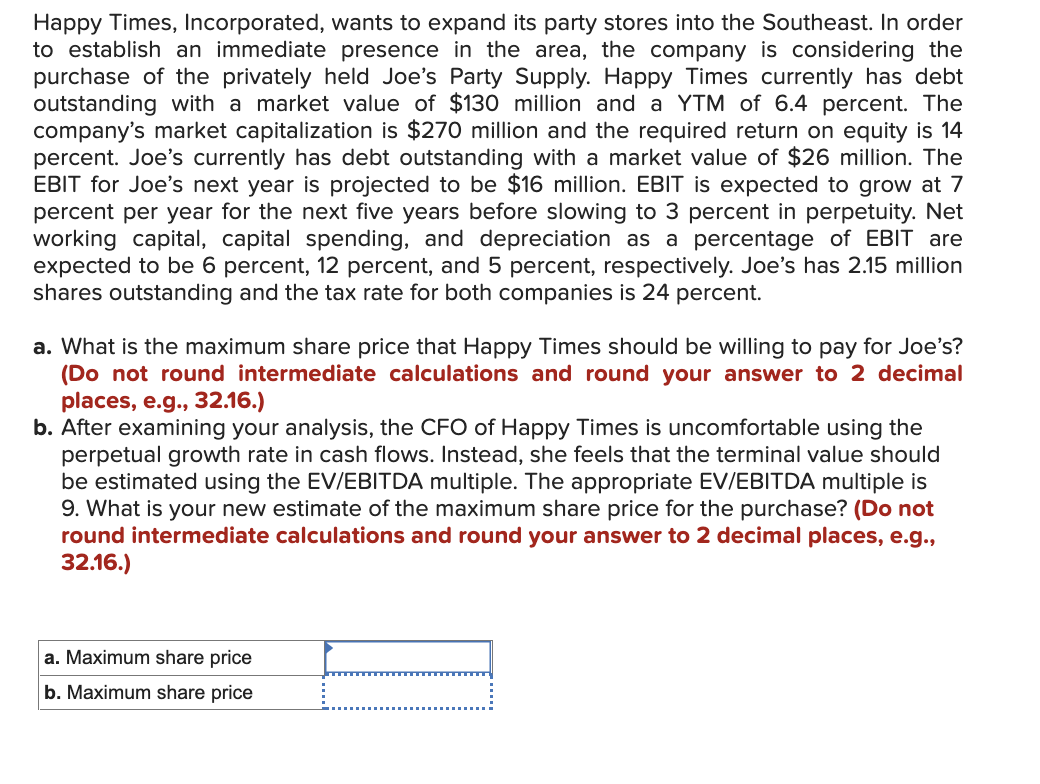

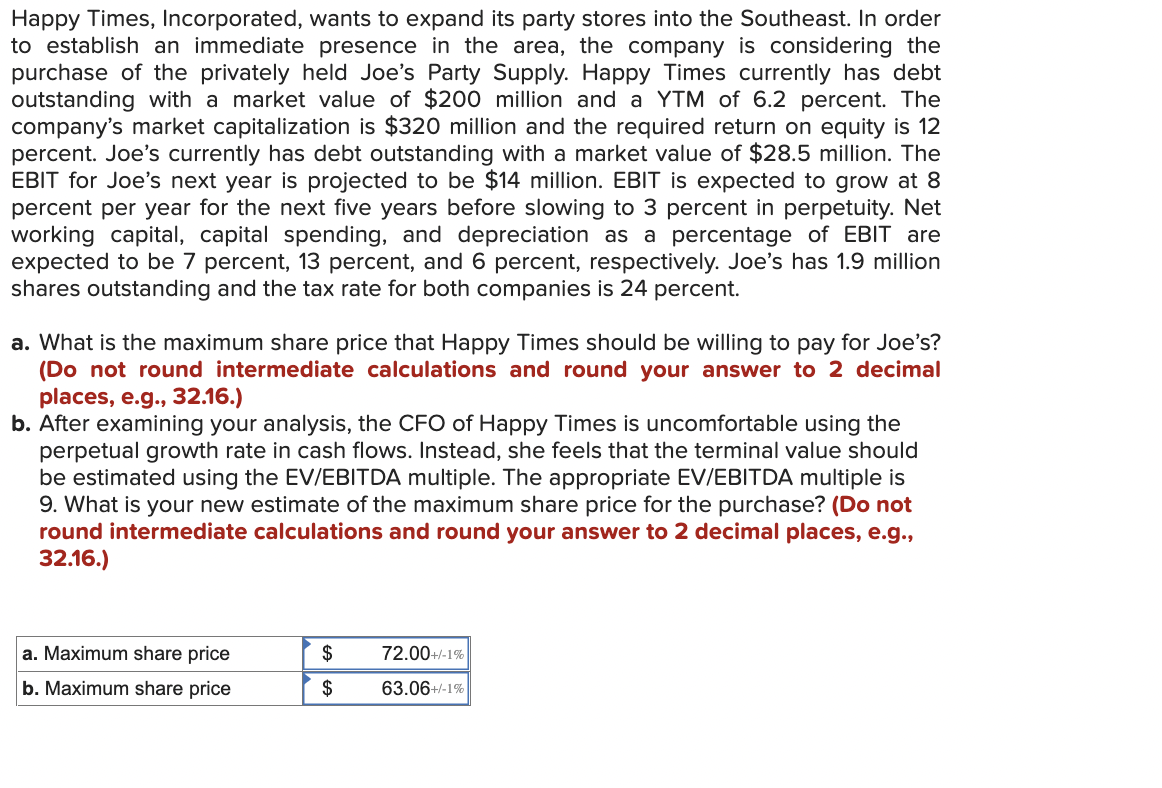

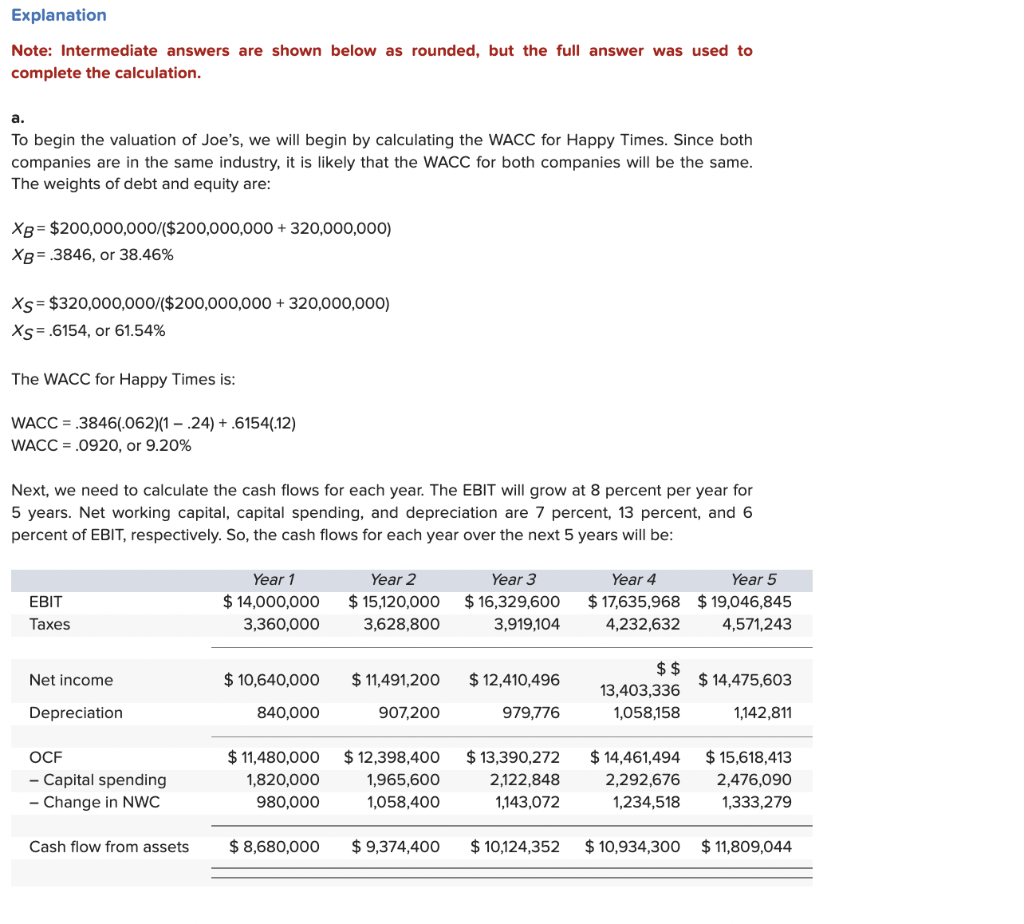

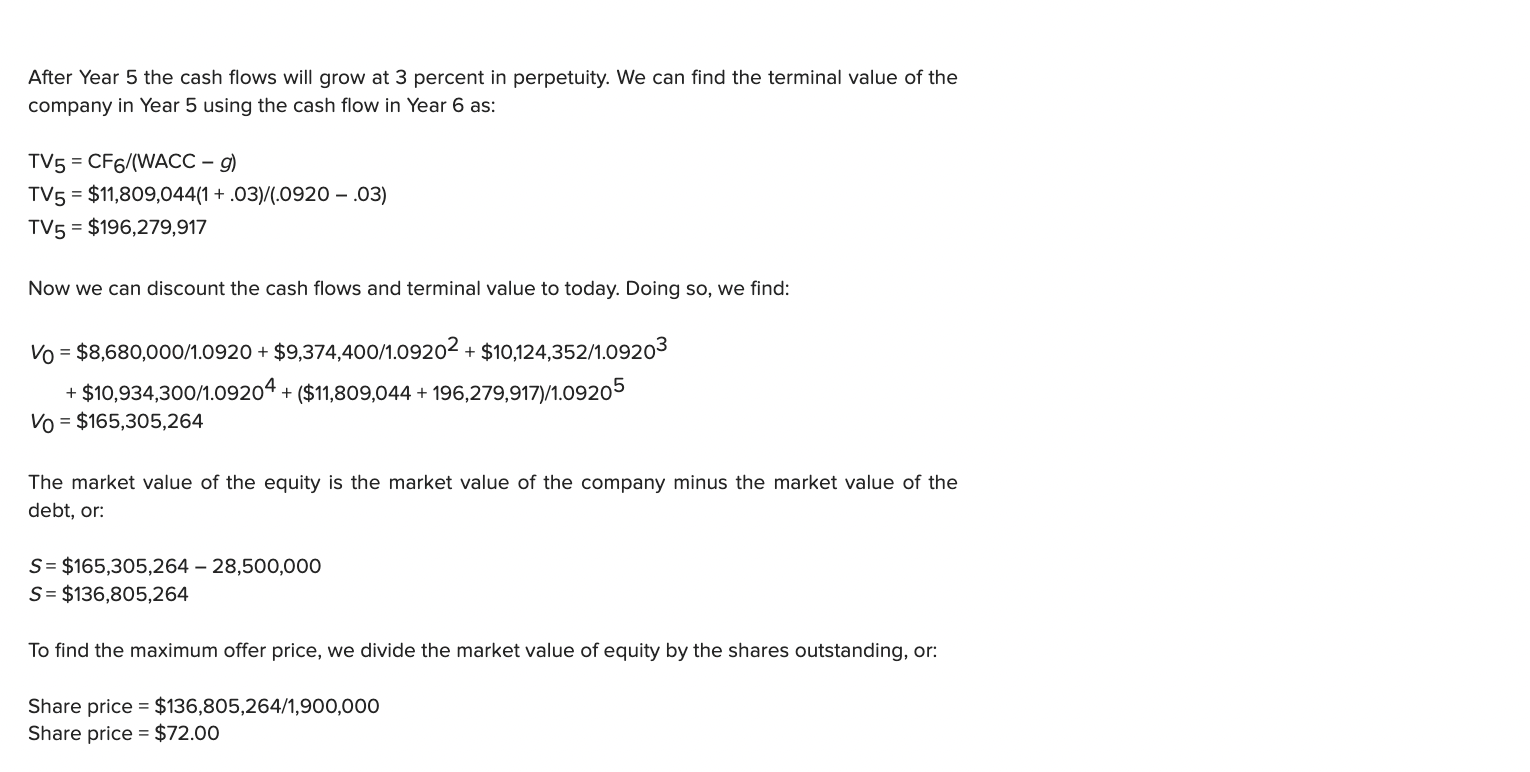

Happy Times, Incorporated, wants to expand its party stores into the Southeast. In order to establish an immediate presence in the area, the company is considering the purchase of the privately held Joe's Party Supply. Happy Times currently has debt outstanding with a market value of $130 million and a YTM of 6.4 percent. The company's market capitalization is $270 million and the required return on equity is 14 percent. Joe's currently has debt outstanding with a market value of $26 million. The EBIT for Joe's next year is projected to be $16 million. EBIT is expected to grow at 7 percent per year for the next five years before slowing to 3 percent in perpetuity. Net working capital, capital spending, and depreciation as a percentage of EBIT are expected to be 6 percent, 12 percent, and 5 percent, respectively. Joe's has 2.15 million shares outstanding and the tax rate for both companies is 24 percent. a. What is the maximum share price that Happy Times should be willing to pay for Joe's? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) b. After examining your analysis, the CFO of Happy Times is uncomfortable using the perpetual growth rate in cash flows. Instead, she feels that the terminal value should be estimated using the EV/EBITDA multiple. The appropriate EV/EBITDA multiple is 9. What is your new estimate of the maximum share price for the purchase? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Happy Times, Incorporated, wants to expand its party stores into the Southeast. In order to establish an immediate presence in the area, the company is considering the purchase of the privately held Joe's Party Supply. Happy Times currently has debt outstanding with a market value of $200 million and a YTM of 6.2 percent. The company's market capitalization is $320 million and the required return on equity is 12 percent. Joe's currently has debt outstanding with a market value of $28.5 million. The EBIT for Joe's next year is projected to be $14 million. EBIT is expected to grow at 8 percent per year for the next five years before slowing to 3 percent in perpetuity. Net working capital, capital spending, and depreciation as a percentage of EBIT are expected to be 7 percent, 13 percent, and 6 percent, respectively. Joe's has 1.9 million shares outstanding and the tax rate for both companies is 24 percent. a. What is the maximum share price that Happy Times should be willing to pay for Joe's? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) b. After examining your analysis, the CFO of Happy Times is uncomfortable using the perpetual growth rate in cash flows. Instead, she feels that the terminal value should be estimated using the EV/EBITDA multiple. The appropriate EV/EBITDA multiple is 9. What is your new estimate of the maximum share price for the purchase? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) a. To begin the valuation of Joe's, we will begin by calculating the WACC for Happy Times. Since both companies are in the same industry, it is likely that the WACC for both companies will be the same. The weights of debt and equity are: xB=$200,000,000/($200,000,000+320,000,000)xB=.3846,or38.46%xS=$320,000,000/($200,000,000+320,000,000)xS=.6154,or61.54% The WACC for Happy Times is: WACC=.3846(.062)(1.24)+.6154(.12)WACC=.0920,or9.20% Next, we need to calculate the cash flows for each year. The EBIT will grow at 8 percent per year for 5 years. Net working capital, capital spending, and depreciation are 7 percent, 13 percent, and 6 percent of EBIT, respectively. So, the cash flows for each year over the next 5 years will be: After Year 5 the cash flows will grow at 3 percent in perpetuity. We can find the terminal value of the company in Year 5 using the cash flow in Year 6 as: TV5=CF6/(WACCg)TV5=$11,809,044(1+.03)/(.0920.03)TV5=$196,279,917 Now we can discount the cash flows and terminal value to today. Doing so, we find: V0=V0$8,680,000/1.0920+$9,374,400/1.09202+$10,124,352/1.09203+$10,934,300/1.09204+($11,809,044+196,279,917)/1.09205=$165,305,264 The market value of the equity is the market value of the company minus the market value of the debt, or: S=$165,305,26428,500,000S=$136,805,264 To find the maximum offer price, we divide the market value of equity by the shares outstanding, or: Share price =$136,805,264/1,900,000 Share price =$72.00 b. To calculate the terminal value using the EV/EBITDA multiple we need to calculate the Year 5 EBITDA, which is EBIT plus depreciation, or: EBITDA=$19,046,845+1,142,811EBITDA=$20,189,656 We can now calculate the terminal value of the company using the Year 5 EBITDA, which will be: TV5=$20,189,656(9)T5=$181,706,905 Note, this is the terminal value in Year 5 since we used the Year 5 EBITDA. We need to calculate the present value of the cash flows for the first 4 years, plus the present value of the Year 5 terminal value. We do not need to include the Year 5 cash flow since it is included in the Year 5 terminal value. So, the value of the company today is: V0=V0=$8,680,000/1.0920+$9,374,400/1.09202+$10,124,352/1.09203+$10,934,300/1.09204+181,706,905/1.09205$148,312,789 The market value of the equity is the market value of the company minus the market value of the debt, or: S=$148,312,78928,500,000S=$119,812,789 To find the maximum offer price, we divide the market value of equity by the shares outstanding, or: Share price =$119,812,789/1,900,000 Share price =$63.06

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts