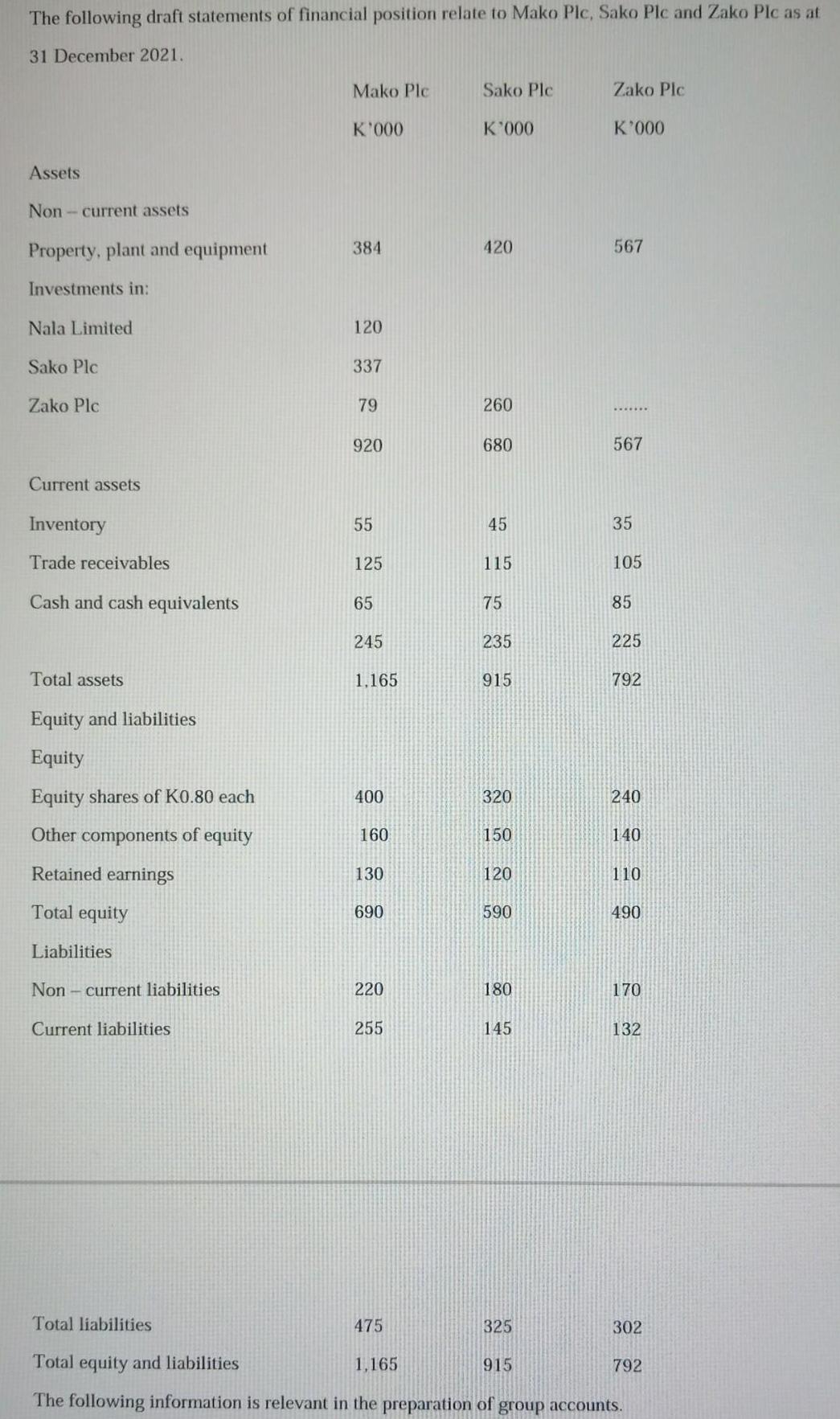

The following draft statements of financial position relate to Mako Plc, Sako Plc and Zako Plc...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The following draft statements of financial position relate to Mako Plc, Sako Plc and Zako Plc as at 31 December 2021. Assets Non-current assets Property, plant and equipment Investments in: Nala Limited Sako Plc Zako Plc Current assets Inventory Trade receivables Cash and cash equivalents Total assets Equity and liabilities Equity Equity shares of K0.80 each Other components of equity Retained earnings Total equity Liabilities Non current liabilities Current liabilities Mako Plc K'000 384 120 337 79 920 55 125 65 245 1,165 400 160 130 690 220 255 Sako Ple K'000 420 260 680 45 115 75 235 915 320 150 120 590 180 145 Zako Plc K'000 567 567 35 105 85 225 792 240 140 110 490 170 132 Total liabilities 475 325 Total equity and liabilities 1,165 915 The following information is relevant in the preparation of group accounts. 302 792 1. Sako Plc acquired 70% of Zako Plc's equity shares on 1 January 2018 for a cash consideration of K260,000. The fair value of Zako Plc's identifiable net assets stood at K350,000. On the same date, other components of equity and retained earnings were K70,000 and K40,000 respectively. The excess in fair value relates to non- depreciable land. 2. Mako Plc acquired 60% of Sako Plc's equity shares and 20% of Zako Plc's equity shares on 1 January 2019 for cash consideration of K337,000 and K79,000 respectively. The fair values of identifiable net assets stood at K545,000 and K415,000 in Sako Plc and Zako Plc respectively. On the same date, other components of equity were K130,000 in Sako Plc and K100,000 in Zako Plc. Retained earnings on the other hand were K90,000 and K60,000 in Sako Plc and Zako Plc respectively. Excess in fair values relate to non- depreciable land of Zako Plc and an item of plant of Sako Plc. The Plant has an economic useful life of five (5) years on 1 Januaryl 2019. 3. Sako Plc and Zako Plc have not issued any additional shares since being acquired by Mako Plc. Further, fair value adjustments referred to in (1) and (2) above have not been incorporated in the above statements of financial position. 4. Investments in Sako Plc and Zako Plc are classified as financial assets through other comprehensive income in accordance with IFRS 9 'Financial instruments'. The fair values of investments in SakoPlc and Zako Plc had not significantly changed since acquisition date. They are therefore recorded in the above statements of financial position at their respective costs. 5. It is group policy to value non-controlling interests using proportion of net assets method. 6. On 1 January 2019 Mako Plc disposed of 60% equity interests in Nala Limited for cash consideration of K180,000. It acquired 100% of the equity shares of Nala Limited six (6) years ago for cash consideration of K300,000 when the fair value of Nala Limited's identifiable net assets were K280,000. At 1 January 2019 the fair values of Nala Limited's identifiable net assets and 40% retained interests in Nava Limited were K290,000 and K120,000 respectively. Purchased goodwill in Nala Limited has not been impaired since its acquisition. Mako Plc has significant influence in Nala Limited at 40% shareholding. Mako Plc adjusted cost of investment by cash received and it recognized neither a profit nor a loss in its financial statements as a result of this disposal. Further, Cash received was correctly recorded in its books. During the year to 31 December 2020, Nava Limited made a profit after tax of K10,000. 7. Mako Plc completed construction of a filling station at a cost of K200,000 on 31 March 2019. Mako Plc is required by the Energy Sector Regulators to dismantle the filling station and restore the land to its original state after 20 years. This will cost Mako Plc K20,000 in 20 years' time. Mako Plc has not yet accounted for the K20,000 in its financial statements for the year to 31 December 2020. However, the cost of K200,000 has been correctly recorded in the books of Mako Plc. Note: Ignore discounting and assume that the cost of K200,000 has been correctly calculated. 8. At 31 December 2021, goodwill in Sako Plc and Zako Plc has not been impaired. Required: Prepare a consolidated statement of financial position of Mako Plc group as at 31 December 2021 in accordance with International Accounting Standards and International Financial Reporting Standards. The following draft statements of financial position relate to Mako Plc, Sako Plc and Zako Plc as at 31 December 2021. Assets Non-current assets Property, plant and equipment Investments in: Nala Limited Sako Plc Zako Plc Current assets Inventory Trade receivables Cash and cash equivalents Total assets Equity and liabilities Equity Equity shares of K0.80 each Other components of equity Retained earnings Total equity Liabilities Non current liabilities Current liabilities Mako Plc K'000 384 120 337 79 920 55 125 65 245 1,165 400 160 130 690 220 255 Sako Ple K'000 420 260 680 45 115 75 235 915 320 150 120 590 180 145 Zako Plc K'000 567 567 35 105 85 225 792 240 140 110 490 170 132 Total liabilities 475 325 Total equity and liabilities 1,165 915 The following information is relevant in the preparation of group accounts. 302 792 1. Sako Plc acquired 70% of Zako Plc's equity shares on 1 January 2018 for a cash consideration of K260,000. The fair value of Zako Plc's identifiable net assets stood at K350,000. On the same date, other components of equity and retained earnings were K70,000 and K40,000 respectively. The excess in fair value relates to non- depreciable land. 2. Mako Plc acquired 60% of Sako Plc's equity shares and 20% of Zako Plc's equity shares on 1 January 2019 for cash consideration of K337,000 and K79,000 respectively. The fair values of identifiable net assets stood at K545,000 and K415,000 in Sako Plc and Zako Plc respectively. On the same date, other components of equity were K130,000 in Sako Plc and K100,000 in Zako Plc. Retained earnings on the other hand were K90,000 and K60,000 in Sako Plc and Zako Plc respectively. Excess in fair values relate to non- depreciable land of Zako Plc and an item of plant of Sako Plc. The Plant has an economic useful life of five (5) years on 1 Januaryl 2019. 3. Sako Plc and Zako Plc have not issued any additional shares since being acquired by Mako Plc. Further, fair value adjustments referred to in (1) and (2) above have not been incorporated in the above statements of financial position. 4. Investments in Sako Plc and Zako Plc are classified as financial assets through other comprehensive income in accordance with IFRS 9 'Financial instruments'. The fair values of investments in SakoPlc and Zako Plc had not significantly changed since acquisition date. They are therefore recorded in the above statements of financial position at their respective costs. 5. It is group policy to value non-controlling interests using proportion of net assets method. 6. On 1 January 2019 Mako Plc disposed of 60% equity interests in Nala Limited for cash consideration of K180,000. It acquired 100% of the equity shares of Nala Limited six (6) years ago for cash consideration of K300,000 when the fair value of Nala Limited's identifiable net assets were K280,000. At 1 January 2019 the fair values of Nala Limited's identifiable net assets and 40% retained interests in Nava Limited were K290,000 and K120,000 respectively. Purchased goodwill in Nala Limited has not been impaired since its acquisition. Mako Plc has significant influence in Nala Limited at 40% shareholding. Mako Plc adjusted cost of investment by cash received and it recognized neither a profit nor a loss in its financial statements as a result of this disposal. Further, Cash received was correctly recorded in its books. During the year to 31 December 2020, Nava Limited made a profit after tax of K10,000. 7. Mako Plc completed construction of a filling station at a cost of K200,000 on 31 March 2019. Mako Plc is required by the Energy Sector Regulators to dismantle the filling station and restore the land to its original state after 20 years. This will cost Mako Plc K20,000 in 20 years' time. Mako Plc has not yet accounted for the K20,000 in its financial statements for the year to 31 December 2020. However, the cost of K200,000 has been correctly recorded in the books of Mako Plc. Note: Ignore discounting and assume that the cost of K200,000 has been correctly calculated. 8. At 31 December 2021, goodwill in Sako Plc and Zako Plc has not been impaired. Required: Prepare a consolidated statement of financial position of Mako Plc group as at 31 December 2021 in accordance with International Accounting Standards and International Financial Reporting Standards.

Expert Answer:

Answer rating: 100% (QA)

To prepare a consolidated statement of financial position for Mako Plc group as at 31 December 2021 we need to consolidate the financial positions of ... View the full answer

Related Book For

Financial Accounting

ISBN: 978-1118978085

IFRS 3rd edition

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso

Posted Date:

Students also viewed these business communication questions

-

The comparative condensed statements of financial position of Conard Corporation are presented on the shown below. Instructions (a) Prepare a horizontal analysis of the statement of financial...

-

The current sections of Nasreen SA's statements of financial position at December 31, 2016 and 2017, are presented here. Nasreen's net income for 2017 was ¬147,000. Depreciation expense was...

-

The comparative condensed statements of financial position of Garcia SLU are presented below. GARCIA SLU Comparative Condensed Statements of Financial Position December 31 Instructions (a) Prepare a...

-

Calculate the dollar proceeds from the FIs loan portfolio at the end of the year, the return on the FIs loan portfolio, and the net interest margin for the FI if the spot foreign exchange rate has...

-

A garden center wants to store leftover packets of vegetable seeds for sale the following spring, but the center is concerned that the seeds may not germinate at the same rate a year later. The...

-

You place an order for 750 units of Good X at a unit price of $51. The supplier offers terms of 1/15, net 35. a. How long do you have to pay before the account is overdue? If you take the full...

-

Use the equation (17.19) suggested by Pai for the turbulent stress and integrate for the velocity profile. How do the results compare with that of Prandtl? = 0.9835 H+ (1-#)['-(1-#)'] (17.19) H+

-

Listed here are the total costs associated with the 2011 production of 10,000 Blu-ray Discs (BDs) manufactured by Hip-Hop. The BDs sell for $15 each. Required 1. Classify each cost and its amount as...

-

Contribution Income Statement, Cost - Volume - Profit Graph, and Taxes Jail and Sail: Alcatraz Tour and Cruise provides sunset sightseeing tours of Alcatraz and the San Francisco Bay. Tickets cost $...

-

Procter & Gamble has been the leading soap manufacturer in the United States since 1879, when it introduced Ivory soap. However, late in 1991, its major rival, Lever Bros. (Unilever), overtook it by...

-

XYZ Company gives year-end bonus to its employees based on their number of year service and their salary. using the following: Years of Service 1 2 to 5 6 to 10 50% of salary 11 and above 75% of...

-

Faith works for a large corporation, which has a small loan program for employees. Faith takes out a $10,000 loan to cover the cost of medical expenses not covered by her insurance. After a year, it...

-

Mally has a $2500 down payment saved for this purchase and the dealer's $ 1500 cash allowance will come straight off her today. how much loan does Mally need. b) How much Molly's monthly payment will...

-

The LLC has assets with a basis of $1,000,000 and a fair market value of $2,400,000. The entity has no liabilities. T has an opportunity to purchase a 25% interest in the entity. The other 75% of the...

-

As a financial analyst advances to the role of financial manager, what key attribute is needed in their new role that was not previously required? Discuss.

-

Five annual payments of $60,000 will be needed to generate a future worth F at an annual interest rate equal to 0.082, calculate the value of F.

-

A company XYZ sells 10,000 of its products a year at $100 per unit. The price elasticity at the price is 1. Suppose its variable cost is $70 per unit. Which one of the following is true? 1. The...

-

Simplify the expression. Assume that all variables are positive. 23VI1 2 V44 8

-

The financial statements of TSMC are presented in Appendix A. The company's complete annual report, including the notes to the financial statements, is available in the Investors section of the...

-

On July 1, 2017, Ticino AG invested CHF736,000 in a mine estimated to have 800,000 tons of ore of uniform grade. During the last 6 months of 2017, 124,000 tons of ore were mined. Instructions (a)...

-

On January 1, 2017, Rolling Hills Country Club purchased a new riding mower for 18,000. The mower is expected to have an 8-year life with a 2,000 residual value. What journal entry would Rolling...

-

What is the primary business of Satyam Computer Services Ltd?

-

In January 2009, approximately how many employees did Satyam Computer Services employ?

-

What was the cash balance sheet amount and how much cash actually existed in the Satyams bank accounts?

Study smarter with the SolutionInn App