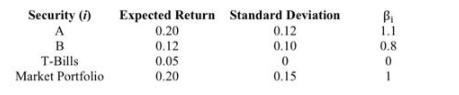

The following expected return and the standard deviation of current returns are known: a) The correlation coefficient

Fantastic news! We've Found the answer you've been seeking!

Question:

The following expected return and the standard deviation of current returns are known:

a) The correlation coefficient is – 1 between security A and B. Find the expected return on the minimum-variance portfolio constructed from these two assets alone.

b) Determine the weights of a portfolio with a standard deviation of 7% created by combining T-Bill and the market portfolio.

c) Determine which of A or B is over-valued or undervalued.

d) How will you invest $1000 in riskless T-bills and the risky assets in the Market Portfolio to maintain a standard deviation of 10%.

Expert Answer:

Related Book For

Fundamentals of Financial Management

ISBN: 978-1305635937

Concise 9th Edition

Authors: Eugene F. Brigham

Posted Date: