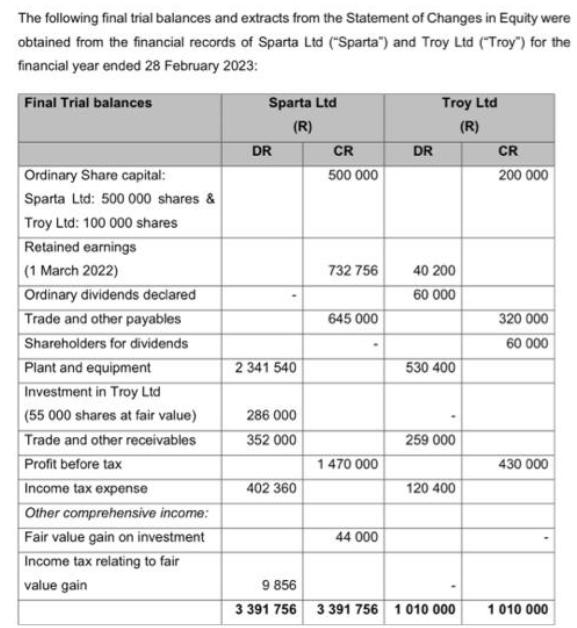

The following final trial balances and extracts from the Statement of Changes in Equity were obtained...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

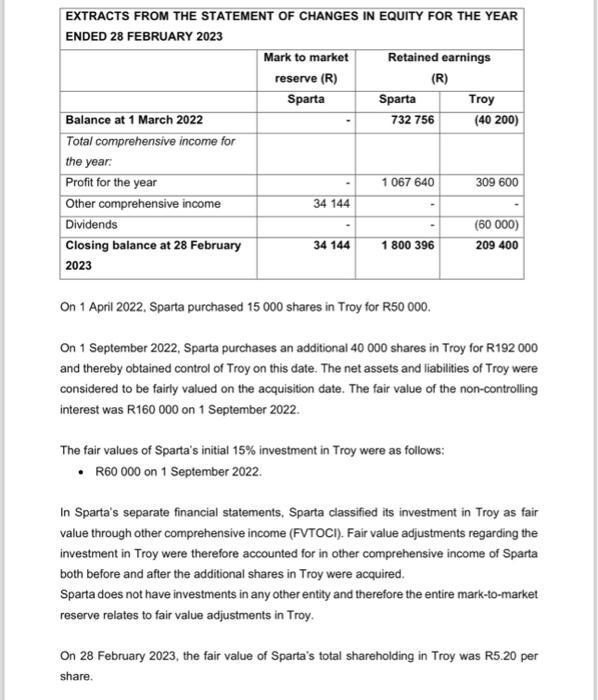

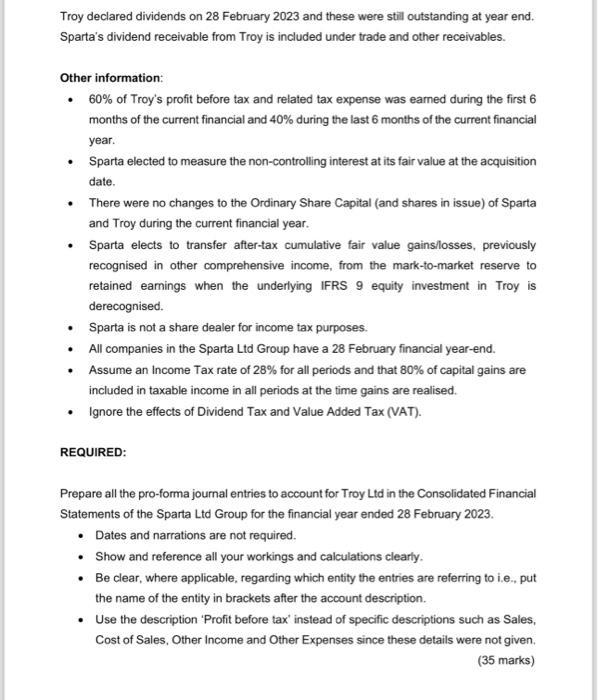

The following final trial balances and extracts from the Statement of Changes in Equity were obtained from the financial records of Sparta Ltd ("Sparta") and Troy Ltd ("Troy") for the financial year ended 28 February 2023: Final Trial balances Ordinary Share capital: Sparta Ltd: 500 000 shares & Troy Ltd: 100 000 shares Retained earnings (1 March 2022) Ordinary dividends declared Trade and other payables Shareholders for dividends Plant and equipment Investment in Troy Ltd (55 000 shares at fair value) Trade and other receivables Profit before tax Income tax expense Other comprehensive income: Fair value gain on investment Income tax relating to fair value gain Sparta Ltd (R) DR 2 341 540 286 000 352 000 402 360 CR 500 000 732 756 645 000 1 470 000 44 000 DR Troy Ltd (R) 40 200 60 000 530 400 259 000 120 400 9 856 3 391 756 3 391 756 1010 000 CR 200 000 320 000 60 000 430 000 1 010 000 EXTRACTS FROM THE STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 28 FEBRUARY 2023 Balance at 1 March 2022 Total comprehensive income for the year: Profit for the year Other comprehensive income Dividends Closing balance at 28 February 2023 Mark to market reserve (R) Sparta 34 144 34 144 Retained earnings Sparta (R) 732 756 1 067 640 1 800 396 On 1 April 2022, Sparta purchased 15 000 shares in Troy for R50 000. Troy The fair values of Sparta's initial 15% investment in Troy were as follows: R60 000 on 1 September 2022. (40 200) 309 600 (60 000) 209 400 On 1 September 2022, Sparta purchases an additional 40 000 shares in Troy for R192 000 and thereby obtained control of Troy on this date. The net assets and liabilities of Troy were considered to be fairly valued on the acquisition date. The fair value of the non-controlling interest was R160 000 on 1 September 2022. In Sparta's separate financial statements, Sparta classified its investment in Troy as fair value through other comprehensive income (FVTOCI). Fair value adjustments regarding the investment in Troy were therefore accounted for in other comprehensive income of Sparta both before and after the additional shares in Troy were acquired. Sparta does not have investments in any other entity and therefore the entire mark-to-market reserve relates to fair value adjustments in Troy. On 28 February 2023, the fair value of Sparta's total shareholding in Troy was R5.20 per share. Troy declared dividends on 28 February 2023 and these were still outstanding at year end. Sparta's dividend receivable from Troy is included under trade and other receivables. Other information: 60% of Troy's profit before tax and related tax expense was earned during the first 6 months of the current financial and 40% during the last 6 months of the current financial year. Sparta elected to measure the non-controlling interest at its fair value at the acquisition date. . There were no changes to the Ordinary Share Capital (and shares in issue) of Sparta and Troy during the current financial year. Sparta elects to transfer after-tax cumulative fair value gains/losses, previously recognised in other comprehensive income, from the mark-to-market reserve to retained earnings when the underlying IFRS 9 equity investment in Troy is derecognised. Sparta is not a share dealer for income tax purposes. All companies in the Sparta Ltd Group have a 28 February financial year-end. Assume an Income Tax rate of 28% for all periods and that 80% of capital gains are included in taxable income in all periods at the time gains are realised. Ignore the effects of Dividend Tax and Value Added Tax (VAT). REQUIRED: Prepare all the pro-forma journal entries to account for Troy Ltd in the Consolidated Financial Statements of the Sparta Ltd Group for the financial year ended 28 February 2023. Dates and narrations are not required. Show and reference all your workings and calculations clearly. Be clear, where applicable, regarding which entity the entries are referring to i.e., put the name of the entity in brackets after the account description. Use the description 'Profit before tax' instead of specific descriptions such as Sales, Cost of Sales, Other Income and Other Expenses since these details were not given. (35 marks) The following final trial balances and extracts from the Statement of Changes in Equity were obtained from the financial records of Sparta Ltd ("Sparta") and Troy Ltd ("Troy") for the financial year ended 28 February 2023: Final Trial balances Ordinary Share capital: Sparta Ltd: 500 000 shares & Troy Ltd: 100 000 shares Retained earnings (1 March 2022) Ordinary dividends declared Trade and other payables Shareholders for dividends Plant and equipment Investment in Troy Ltd (55 000 shares at fair value) Trade and other receivables Profit before tax Income tax expense Other comprehensive income: Fair value gain on investment Income tax relating to fair value gain Sparta Ltd (R) DR 2 341 540 286 000 352 000 402 360 CR 500 000 732 756 645 000 1 470 000 44 000 DR Troy Ltd (R) 40 200 60 000 530 400 259 000 120 400 9 856 3 391 756 3 391 756 1010 000 CR 200 000 320 000 60 000 430 000 1 010 000 EXTRACTS FROM THE STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 28 FEBRUARY 2023 Balance at 1 March 2022 Total comprehensive income for the year: Profit for the year Other comprehensive income Dividends Closing balance at 28 February 2023 Mark to market reserve (R) Sparta 34 144 34 144 Retained earnings Sparta (R) 732 756 1 067 640 1 800 396 On 1 April 2022, Sparta purchased 15 000 shares in Troy for R50 000. Troy The fair values of Sparta's initial 15% investment in Troy were as follows: R60 000 on 1 September 2022. (40 200) 309 600 (60 000) 209 400 On 1 September 2022, Sparta purchases an additional 40 000 shares in Troy for R192 000 and thereby obtained control of Troy on this date. The net assets and liabilities of Troy were considered to be fairly valued on the acquisition date. The fair value of the non-controlling interest was R160 000 on 1 September 2022. In Sparta's separate financial statements, Sparta classified its investment in Troy as fair value through other comprehensive income (FVTOCI). Fair value adjustments regarding the investment in Troy were therefore accounted for in other comprehensive income of Sparta both before and after the additional shares in Troy were acquired. Sparta does not have investments in any other entity and therefore the entire mark-to-market reserve relates to fair value adjustments in Troy. On 28 February 2023, the fair value of Sparta's total shareholding in Troy was R5.20 per share. Troy declared dividends on 28 February 2023 and these were still outstanding at year end. Sparta's dividend receivable from Troy is included under trade and other receivables. Other information: 60% of Troy's profit before tax and related tax expense was earned during the first 6 months of the current financial and 40% during the last 6 months of the current financial year. Sparta elected to measure the non-controlling interest at its fair value at the acquisition date. . There were no changes to the Ordinary Share Capital (and shares in issue) of Sparta and Troy during the current financial year. Sparta elects to transfer after-tax cumulative fair value gains/losses, previously recognised in other comprehensive income, from the mark-to-market reserve to retained earnings when the underlying IFRS 9 equity investment in Troy is derecognised. Sparta is not a share dealer for income tax purposes. All companies in the Sparta Ltd Group have a 28 February financial year-end. Assume an Income Tax rate of 28% for all periods and that 80% of capital gains are included in taxable income in all periods at the time gains are realised. Ignore the effects of Dividend Tax and Value Added Tax (VAT). REQUIRED: Prepare all the pro-forma journal entries to account for Troy Ltd in the Consolidated Financial Statements of the Sparta Ltd Group for the financial year ended 28 February 2023. Dates and narrations are not required. Show and reference all your workings and calculations clearly. Be clear, where applicable, regarding which entity the entries are referring to i.e., put the name of the entity in brackets after the account description. Use the description 'Profit before tax' instead of specific descriptions such as Sales, Cost of Sales, Other Income and Other Expenses since these details were not given. (35 marks)

Expert Answer:

Answer rating: 100% (QA)

To provide a comprehensive analysis I will summarize the key information and transactions and calculate relevant financial figures 1 Sparta Ltd and Tr... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Interstate Manufacturing is considering either overhauling an old machine or replacing it with a new machine. Information about the two alternatives follows. Management requires a 10% rate of return...

-

Payback, NPV, and MIRR Your division is considering two investment projects, each of which requires an up-front expenditure of $27 million. You estimate that the cost of capital is 12% and that the...

-

Give Jacobson et al.s definition of a component.

-

Find the transfer function Vo(s)/Vi(s) for the network shown in fig. Discuss.

-

Hannibal owns a farm. He purchases a tractor in 2012 at a cost of $25,000. Because 2012 is a bad year, he does not deduct any depreciation on the tractor in 2012. He sells the tractor in 2016 for...

-

The rotor shown in Fig. P12.1 rotates clockwise. Assume that the fluid enters in the radial direction and the relative velocity is tangent to the blades and remains constant across the entire rotor....

-

Paul Ward is interested in the stock of Pecunious Products, Inc. Before purchasing the stock, Ward would like your help in analyzing the data that are available to him as follows: Mr. Ward would like...

-

What would be good thorough answers to the below questions? The role of the financial manager is crucial inevery type of organization. Locate a job posting for a financial manager position from any...

-

Kennedy Prisby, age 33, is single and has no dependents. Her social security number is 111-22-3333. Her address is 101 North Fork Ave., Cedar City, UT 84720. She has no intention of donating to the...

-

a. Discuss the benefits that will accrue to a country enjoying a high economic growth rate? b. What are the limitations to high economic growth rates?

-

a) Differentiate between fiscal and Monetary Policy. (4 marks) b) Discuss any four objectives or goals of monetary policy as used to control and regulate money supply by the Central Banking...

-

a) Define the term unemployment and discuss the main causes of unemployment in developing countries (5 marks) b) Suggest the possible measures that you would implement to contain unemployment...

-

(a) Succinctly explain the methods of computing national income of a country citing the necessary adjustments to be taken in each case. (15 marks) (b) What is the difference between gross domestic...

-

a) Compare and contrast the capitalist market system and the command system. [6 Marks] b) Discuss how prices of substitutes and complements, income, cost of doing business can affect supply of flour...

-

(a) What are the causes of monopoly? Is monopoly desirable? (8marks) (b) With the use of examples, differentiate between positive and normative economics (5marks) (c) Differentiate between movements...

-

39. Water is conveyed at a volumetric rate of 4.8 x 10-2m/s through a pipeline as shown in figure 2. The internal diameter of the pipeline at sections 2 is 5.84cm and loss in head 4m. Determine the...

-

In Exercises, find the equation of the tangent line at the given point on each curve. 2y 2 - x = 4; (16, 2)

-

Outline the accounting adjustments required in relation to transactions between the company and an associate or joint venture. Explain the rationale for these adjustments.

-

On January 1, 2013, Lessard acquired 80% of the share capital of Honey for $264,800. This was sufcient for Lessard to gain control over Honey. On that date, the statement of nancial position of Honey...

-

What are the needs of the users of a not-for-profit organization's financial statement versus those of a profit oriented company?

-

The steam is generated at 8 bar from water at \(32^{\circ} \mathrm{C}\). Find the heat required to produce \(1 \mathrm{~kg}\) of steam. (a) When the steam at dryness \(=0.9\). (b) When the steam is...

-

Determine the state of steam at : (a) \(p=14\) bar and \(t=210^{\circ} \mathrm{C}\), and (b) \(p=8\) bar and \(2700 \mathrm{~kJ} / \mathrm{kg}\) of heat supplied to water from

-

Determine the condition of steam in the following cases : (a) At a pressure of 10 bar and \(200^{\circ} \mathrm{C}\). (b) At a pressure of 8 bar and specific volume of \(0.22 \mathrm{~m}^{3} /...

Study smarter with the SolutionInn App