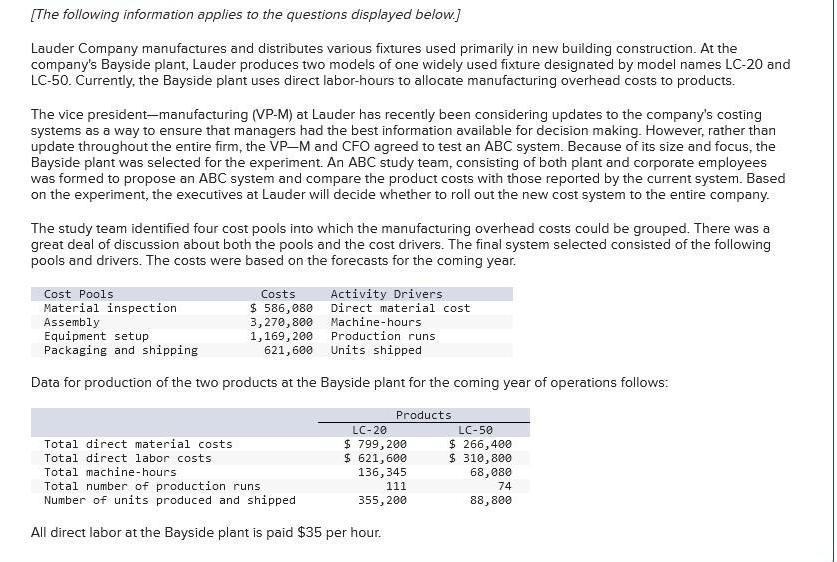

[The following information applies to the questions displayed below.] Lauder Company manufactures and distributes various fixtures...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

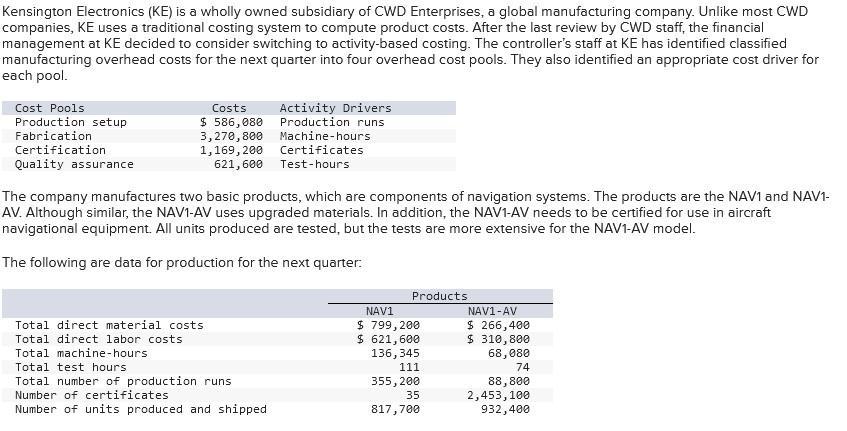

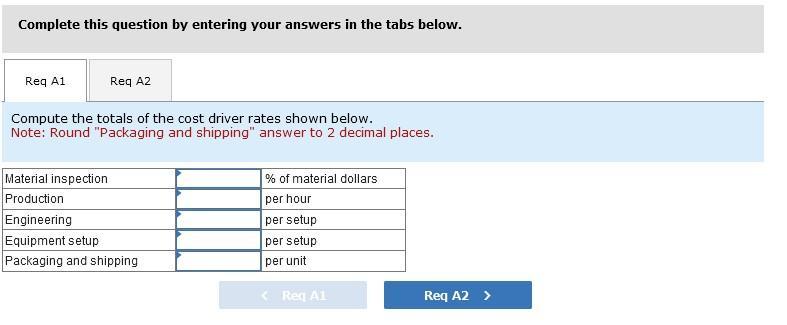

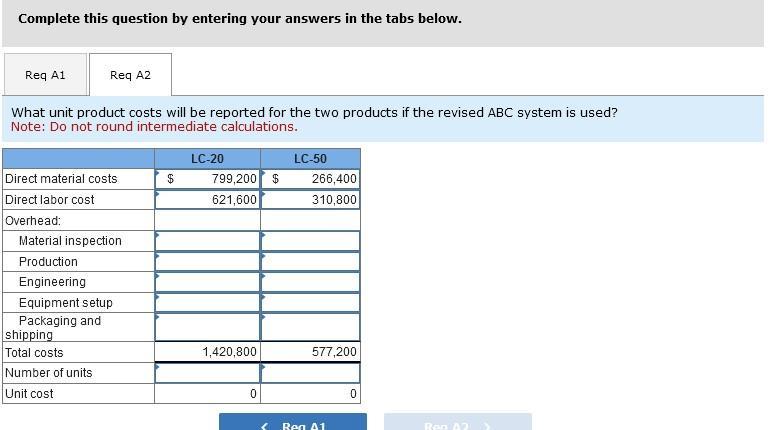

[The following information applies to the questions displayed below.] Lauder Company manufactures and distributes various fixtures used primarily in new building construction. At the company's Bayside plant, Lauder produces two models of one widely used fixture designated by model names LC-20 and LC-50. Currently, the Bayside plant uses direct labor-hours to allocate manufacturing overhead costs to products. The vice president-manufacturing (VP-M) at Lauder has recently been considering updates to the company's costing systems as a way to ensure that managers had the best information available for decision making. However, rather than update throughout the entire firm, the VP-M and CFO agreed to test an ABC system. Because of its size and focus, the Bayside plant was selected for the experiment. An ABC study team, consisting of both plant and corporate employees was formed to propose an ABC system and compare the product costs with those reported by the current system. Based on the experiment, the executives at Lauder will decide whether to roll out the new cost system to the entire company. The study team identified four cost pools into which the manufacturing overhead costs could be grouped. There was a great deal of discussion about both the pools and the cost drivers. The final system selected consisted of the following pools and drivers. The costs were based on the forecasts for the coming year. Cost Pools Material inspection Assembly Costs $ 586,080 3,270,800 1,169,200 Machine-hours Equipment setup Production runs Packaging and shipping 621,600 Units shipped Data for production of the two products at the Bayside plant for the coming year of operations follows: Activity Drivers Direct material cost Products LC-20 $ 799,200 $ 621,600 136,345 111 355,200 Total direct material costs Total direct labor costs Total machine-hours Total number of production runs Number of units produced and shipped All direct labor at the Bayside plant is paid $35 per hour. LC-50 $ 266,400 $ 310,800 68,080 74 88,800 Kensington Electronics (KE) is a wholly owned subsidiary of CWD Enterprises, a global manufacturing company. Unlike most CWD companies, KE uses a traditional costing system to compute product costs. After the last review by CWD staff, the financial management at KE decided to consider switching to activity-based costing. The controller's staff at KE has identified classified manufacturing overhead costs for the next quarter into four overhead cost pools. They also identified an appropriate cost driver for each pool. Cost Pools Production setup Fabrication Certification Quality assurance Costs $ 586,080 Activity Drivers Production runs 3,270,800 Machine-hours 1,169,200 Certificates 621,600 Test-hours The company manufactures two basic products, which are components of navigation systems. The products are the NAV1 and NAV1- AV. Although similar, the NAV1-AV uses upgraded materials. In addition, the NAV1-AV needs to be certified for use in aircraft navigational equipment. All units produced are tested, but the tests are more extensive for the NAV1-AV model. The following are data for production for the next quarter: Total direct material costs Total direct labor costs. Total machine-hours Total test hours Total number of production runs Number of certificates Number of units produced and shipped. Products NAV1 $ 799,200 $ 621,600 136,345 111 355,200 35 817,700 NAV1-AV $ 266,400 $ 310,800 68,080 74 88,800 2,453,100 932,400 Complete this question by entering your answers in the tabs below. Req A1 Req A2 Compute the totals of the cost driver rates shown below. Note: Round "Packaging and shipping" answer to 2 decimal places. Material inspection Production Engineering Equipment setup Packaging and shipping % of material dollars per hour per setup per setup per unit Req Al Req A2 > Complete this question by entering your answers in the tabs below. Req A2 What unit product costs will be reported for the two products if the revised ABC system is used? Note: Do not round intermediate calculations. Req A1 Direct material costs Direct labor cost Overhead: Material inspection Production Engineering Equipment setup Packaging and shipping Total costs Number of units Unit cost $ LC-20 799,200 $ 621,600 1,420,800 0 < LC-50 266,400 310,800 577,200 Reg A1 0 Ren 07 [The following information applies to the questions displayed below.] Lauder Company manufactures and distributes various fixtures used primarily in new building construction. At the company's Bayside plant, Lauder produces two models of one widely used fixture designated by model names LC-20 and LC-50. Currently, the Bayside plant uses direct labor-hours to allocate manufacturing overhead costs to products. The vice president-manufacturing (VP-M) at Lauder has recently been considering updates to the company's costing systems as a way to ensure that managers had the best information available for decision making. However, rather than update throughout the entire firm, the VP-M and CFO agreed to test an ABC system. Because of its size and focus, the Bayside plant was selected for the experiment. An ABC study team, consisting of both plant and corporate employees was formed to propose an ABC system and compare the product costs with those reported by the current system. Based on the experiment, the executives at Lauder will decide whether to roll out the new cost system to the entire company. The study team identified four cost pools into which the manufacturing overhead costs could be grouped. There was a great deal of discussion about both the pools and the cost drivers. The final system selected consisted of the following pools and drivers. The costs were based on the forecasts for the coming year. Cost Pools Material inspection Assembly Costs $ 586,080 3,270,800 1,169,200 Machine-hours Equipment setup Production runs Packaging and shipping 621,600 Units shipped Data for production of the two products at the Bayside plant for the coming year of operations follows: Activity Drivers Direct material cost Products LC-20 $ 799,200 $ 621,600 136,345 111 355,200 Total direct material costs Total direct labor costs Total machine-hours Total number of production runs Number of units produced and shipped All direct labor at the Bayside plant is paid $35 per hour. LC-50 $ 266,400 $ 310,800 68,080 74 88,800 Kensington Electronics (KE) is a wholly owned subsidiary of CWD Enterprises, a global manufacturing company. Unlike most CWD companies, KE uses a traditional costing system to compute product costs. After the last review by CWD staff, the financial management at KE decided to consider switching to activity-based costing. The controller's staff at KE has identified classified manufacturing overhead costs for the next quarter into four overhead cost pools. They also identified an appropriate cost driver for each pool. Cost Pools Production setup Fabrication Certification Quality assurance Costs $ 586,080 Activity Drivers Production runs 3,270,800 Machine-hours 1,169,200 Certificates 621,600 Test-hours The company manufactures two basic products, which are components of navigation systems. The products are the NAV1 and NAV1- AV. Although similar, the NAV1-AV uses upgraded materials. In addition, the NAV1-AV needs to be certified for use in aircraft navigational equipment. All units produced are tested, but the tests are more extensive for the NAV1-AV model. The following are data for production for the next quarter: Total direct material costs Total direct labor costs. Total machine-hours Total test hours Total number of production runs Number of certificates Number of units produced and shipped. Products NAV1 $ 799,200 $ 621,600 136,345 111 355,200 35 817,700 NAV1-AV $ 266,400 $ 310,800 68,080 74 88,800 2,453,100 932,400 Complete this question by entering your answers in the tabs below. Req A1 Req A2 Compute the totals of the cost driver rates shown below. Note: Round "Packaging and shipping" answer to 2 decimal places. Material inspection Production Engineering Equipment setup Packaging and shipping % of material dollars per hour per setup per setup per unit Req Al Req A2 > Complete this question by entering your answers in the tabs below. Req A2 What unit product costs will be reported for the two products if the revised ABC system is used? Note: Do not round intermediate calculations. Req A1 Direct material costs Direct labor cost Overhead: Material inspection Production Engineering Equipment setup Packaging and shipping Total costs Number of units Unit cost $ LC-20 799,200 $ 621,600 1,420,800 0 < LC-50 266,400 310,800 577,200 Reg A1 0 Ren 07 [The following information applies to the questions displayed below.] Lauder Company manufactures and distributes various fixtures used primarily in new building construction. At the company's Bayside plant, Lauder produces two models of one widely used fixture designated by model names LC-20 and LC-50. Currently, the Bayside plant uses direct labor-hours to allocate manufacturing overhead costs to products. The vice president-manufacturing (VP-M) at Lauder has recently been considering updates to the company's costing systems as a way to ensure that managers had the best information available for decision making. However, rather than update throughout the entire firm, the VP-M and CFO agreed to test an ABC system. Because of its size and focus, the Bayside plant was selected for the experiment. An ABC study team, consisting of both plant and corporate employees was formed to propose an ABC system and compare the product costs with those reported by the current system. Based on the experiment, the executives at Lauder will decide whether to roll out the new cost system to the entire company. The study team identified four cost pools into which the manufacturing overhead costs could be grouped. There was a great deal of discussion about both the pools and the cost drivers. The final system selected consisted of the following pools and drivers. The costs were based on the forecasts for the coming year. Cost Pools Material inspection Assembly Costs $ 586,080 3,270,800 1,169,200 Machine-hours Equipment setup Production runs Packaging and shipping 621,600 Units shipped Data for production of the two products at the Bayside plant for the coming year of operations follows: Activity Drivers Direct material cost Products LC-20 $ 799,200 $ 621,600 136,345 111 355,200 Total direct material costs Total direct labor costs Total machine-hours Total number of production runs Number of units produced and shipped All direct labor at the Bayside plant is paid $35 per hour. LC-50 $ 266,400 $ 310,800 68,080 74 88,800 Kensington Electronics (KE) is a wholly owned subsidiary of CWD Enterprises, a global manufacturing company. Unlike most CWD companies, KE uses a traditional costing system to compute product costs. After the last review by CWD staff, the financial management at KE decided to consider switching to activity-based costing. The controller's staff at KE has identified classified manufacturing overhead costs for the next quarter into four overhead cost pools. They also identified an appropriate cost driver for each pool. Cost Pools Production setup Fabrication Certification Quality assurance Costs $ 586,080 Activity Drivers Production runs 3,270,800 Machine-hours 1,169,200 Certificates 621,600 Test-hours The company manufactures two basic products, which are components of navigation systems. The products are the NAV1 and NAV1- AV. Although similar, the NAV1-AV uses upgraded materials. In addition, the NAV1-AV needs to be certified for use in aircraft navigational equipment. All units produced are tested, but the tests are more extensive for the NAV1-AV model. The following are data for production for the next quarter: Total direct material costs Total direct labor costs. Total machine-hours Total test hours Total number of production runs Number of certificates Number of units produced and shipped. Products NAV1 $ 799,200 $ 621,600 136,345 111 355,200 35 817,700 NAV1-AV $ 266,400 $ 310,800 68,080 74 88,800 2,453,100 932,400 Complete this question by entering your answers in the tabs below. Req A1 Req A2 Compute the totals of the cost driver rates shown below. Note: Round "Packaging and shipping" answer to 2 decimal places. Material inspection Production Engineering Equipment setup Packaging and shipping % of material dollars per hour per setup per setup per unit Req Al Req A2 > Complete this question by entering your answers in the tabs below. Req A2 What unit product costs will be reported for the two products if the revised ABC system is used? Note: Do not round intermediate calculations. Req A1 Direct material costs Direct labor cost Overhead: Material inspection Production Engineering Equipment setup Packaging and shipping Total costs Number of units Unit cost $ LC-20 799,200 $ 621,600 1,420,800 0 < LC-50 266,400 310,800 577,200 Reg A1 0 Ren 07 [The following information applies to the questions displayed below.] Lauder Company manufactures and distributes various fixtures used primarily in new building construction. At the company's Bayside plant, Lauder produces two models of one widely used fixture designated by model names LC-20 and LC-50. Currently, the Bayside plant uses direct labor-hours to allocate manufacturing overhead costs to products. The vice president-manufacturing (VP-M) at Lauder has recently been considering updates to the company's costing systems as a way to ensure that managers had the best information available for decision making. However, rather than update throughout the entire firm, the VP-M and CFO agreed to test an ABC system. Because of its size and focus, the Bayside plant was selected for the experiment. An ABC study team, consisting of both plant and corporate employees was formed to propose an ABC system and compare the product costs with those reported by the current system. Based on the experiment, the executives at Lauder will decide whether to roll out the new cost system to the entire company. The study team identified four cost pools into which the manufacturing overhead costs could be grouped. There was a great deal of discussion about both the pools and the cost drivers. The final system selected consisted of the following pools and drivers. The costs were based on the forecasts for the coming year. Cost Pools Material inspection Assembly Costs $ 586,080 3,270,800 1,169,200 Machine-hours Equipment setup Production runs Packaging and shipping 621,600 Units shipped Data for production of the two products at the Bayside plant for the coming year of operations follows: Activity Drivers Direct material cost Products LC-20 $ 799,200 $ 621,600 136,345 111 355,200 Total direct material costs Total direct labor costs Total machine-hours Total number of production runs Number of units produced and shipped All direct labor at the Bayside plant is paid $35 per hour. LC-50 $ 266,400 $ 310,800 68,080 74 88,800 Kensington Electronics (KE) is a wholly owned subsidiary of CWD Enterprises, a global manufacturing company. Unlike most CWD companies, KE uses a traditional costing system to compute product costs. After the last review by CWD staff, the financial management at KE decided to consider switching to activity-based costing. The controller's staff at KE has identified classified manufacturing overhead costs for the next quarter into four overhead cost pools. They also identified an appropriate cost driver for each pool. Cost Pools Production setup Fabrication Certification Quality assurance Costs $ 586,080 Activity Drivers Production runs 3,270,800 Machine-hours 1,169,200 Certificates 621,600 Test-hours The company manufactures two basic products, which are components of navigation systems. The products are the NAV1 and NAV1- AV. Although similar, the NAV1-AV uses upgraded materials. In addition, the NAV1-AV needs to be certified for use in aircraft navigational equipment. All units produced are tested, but the tests are more extensive for the NAV1-AV model. The following are data for production for the next quarter: Total direct material costs Total direct labor costs. Total machine-hours Total test hours Total number of production runs Number of certificates Number of units produced and shipped. Products NAV1 $ 799,200 $ 621,600 136,345 111 355,200 35 817,700 NAV1-AV $ 266,400 $ 310,800 68,080 74 88,800 2,453,100 932,400 Complete this question by entering your answers in the tabs below. Req A1 Req A2 Compute the totals of the cost driver rates shown below. Note: Round "Packaging and shipping" answer to 2 decimal places. Material inspection Production Engineering Equipment setup Packaging and shipping % of material dollars per hour per setup per setup per unit Req Al Req A2 > Complete this question by entering your answers in the tabs below. Req A2 What unit product costs will be reported for the two products if the revised ABC system is used? Note: Do not round intermediate calculations. Req A1 Direct material costs Direct labor cost Overhead: Material inspection Production Engineering Equipment setup Packaging and shipping Total costs Number of units Unit cost $ LC-20 799,200 $ 621,600 1,420,800 0 < LC-50 266,400 310,800 577,200 Reg A1 0 Ren 07 [The following information applies to the questions displayed below.] Lauder Company manufactures and distributes various fixtures used primarily in new building construction. At the company's Bayside plant, Lauder produces two models of one widely used fixture designated by model names LC-20 and LC-50. Currently, the Bayside plant uses direct labor-hours to allocate manufacturing overhead costs to products. The vice president-manufacturing (VP-M) at Lauder has recently been considering updates to the company's costing systems as a way to ensure that managers had the best information available for decision making. However, rather than update throughout the entire firm, the VP-M and CFO agreed to test an ABC system. Because of its size and focus, the Bayside plant was selected for the experiment. An ABC study team, consisting of both plant and corporate employees was formed to propose an ABC system and compare the product costs with those reported by the current system. Based on the experiment, the executives at Lauder will decide whether to roll out the new cost system to the entire company. The study team identified four cost pools into which the manufacturing overhead costs could be grouped. There was a great deal of discussion about both the pools and the cost drivers. The final system selected consisted of the following pools and drivers. The costs were based on the forecasts for the coming year. Cost Pools Material inspection Assembly Costs $ 586,080 3,270,800 1,169,200 Machine-hours Equipment setup Production runs Packaging and shipping 621,600 Units shipped Data for production of the two products at the Bayside plant for the coming year of operations follows: Activity Drivers Direct material cost Products LC-20 $ 799,200 $ 621,600 136,345 111 355,200 Total direct material costs Total direct labor costs Total machine-hours Total number of production runs Number of units produced and shipped All direct labor at the Bayside plant is paid $35 per hour. LC-50 $ 266,400 $ 310,800 68,080 74 88,800 Kensington Electronics (KE) is a wholly owned subsidiary of CWD Enterprises, a global manufacturing company. Unlike most CWD companies, KE uses a traditional costing system to compute product costs. After the last review by CWD staff, the financial management at KE decided to consider switching to activity-based costing. The controller's staff at KE has identified classified manufacturing overhead costs for the next quarter into four overhead cost pools. They also identified an appropriate cost driver for each pool. Cost Pools Production setup Fabrication Certification Quality assurance Costs $ 586,080 Activity Drivers Production runs 3,270,800 Machine-hours 1,169,200 Certificates 621,600 Test-hours The company manufactures two basic products, which are components of navigation systems. The products are the NAV1 and NAV1- AV. Although similar, the NAV1-AV uses upgraded materials. In addition, the NAV1-AV needs to be certified for use in aircraft navigational equipment. All units produced are tested, but the tests are more extensive for the NAV1-AV model. The following are data for production for the next quarter: Total direct material costs Total direct labor costs. Total machine-hours Total test hours Total number of production runs Number of certificates Number of units produced and shipped. Products NAV1 $ 799,200 $ 621,600 136,345 111 355,200 35 817,700 NAV1-AV $ 266,400 $ 310,800 68,080 74 88,800 2,453,100 932,400 Complete this question by entering your answers in the tabs below. Req A1 Req A2 Compute the totals of the cost driver rates shown below. Note: Round "Packaging and shipping" answer to 2 decimal places. Material inspection Production Engineering Equipment setup Packaging and shipping % of material dollars per hour per setup per setup per unit Req Al Req A2 > Complete this question by entering your answers in the tabs below. Req A2 What unit product costs will be reported for the two products if the revised ABC system is used? Note: Do not round intermediate calculations. Req A1 Direct material costs Direct labor cost Overhead: Material inspection Production Engineering Equipment setup Packaging and shipping Total costs Number of units Unit cost $ LC-20 799,200 $ 621,600 1,420,800 0 < LC-50 266,400 310,800 577,200 Reg A1 0 Ren 07 [The following information applies to the questions displayed below.] Lauder Company manufactures and distributes various fixtures used primarily in new building construction. At the company's Bayside plant, Lauder produces two models of one widely used fixture designated by model names LC-20 and LC-50. Currently, the Bayside plant uses direct labor-hours to allocate manufacturing overhead costs to products. The vice president-manufacturing (VP-M) at Lauder has recently been considering updates to the company's costing systems as a way to ensure that managers had the best information available for decision making. However, rather than update throughout the entire firm, the VP-M and CFO agreed to test an ABC system. Because of its size and focus, the Bayside plant was selected for the experiment. An ABC study team, consisting of both plant and corporate employees was formed to propose an ABC system and compare the product costs with those reported by the current system. Based on the experiment, the executives at Lauder will decide whether to roll out the new cost system to the entire company. The study team identified four cost pools into which the manufacturing overhead costs could be grouped. There was a great deal of discussion about both the pools and the cost drivers. The final system selected consisted of the following pools and drivers. The costs were based on the forecasts for the coming year. Cost Pools Material inspection Assembly Costs $ 586,080 3,270,800 1,169,200 Machine-hours Equipment setup Production runs Packaging and shipping 621,600 Units shipped Data for production of the two products at the Bayside plant for the coming year of operations follows: Activity Drivers Direct material cost Products LC-20 $ 799,200 $ 621,600 136,345 111 355,200 Total direct material costs Total direct labor costs Total machine-hours Total number of production runs Number of units produced and shipped All direct labor at the Bayside plant is paid $35 per hour. LC-50 $ 266,400 $ 310,800 68,080 74 88,800 Kensington Electronics (KE) is a wholly owned subsidiary of CWD Enterprises, a global manufacturing company. Unlike most CWD companies, KE uses a traditional costing system to compute product costs. After the last review by CWD staff, the financial management at KE decided to consider switching to activity-based costing. The controller's staff at KE has identified classified manufacturing overhead costs for the next quarter into four overhead cost pools. They also identified an appropriate cost driver for each pool. Cost Pools Production setup Fabrication Certification Quality assurance Costs $ 586,080 Activity Drivers Production runs 3,270,800 Machine-hours 1,169,200 Certificates 621,600 Test-hours The company manufactures two basic products, which are components of navigation systems. The products are the NAV1 and NAV1- AV. Although similar, the NAV1-AV uses upgraded materials. In addition, the NAV1-AV needs to be certified for use in aircraft navigational equipment. All units produced are tested, but the tests are more extensive for the NAV1-AV model. The following are data for production for the next quarter: Total direct material costs Total direct labor costs. Total machine-hours Total test hours Total number of production runs Number of certificates Number of units produced and shipped. Products NAV1 $ 799,200 $ 621,600 136,345 111 355,200 35 817,700 NAV1-AV $ 266,400 $ 310,800 68,080 74 88,800 2,453,100 932,400 Complete this question by entering your answers in the tabs below. Req A1 Req A2 Compute the totals of the cost driver rates shown below. Note: Round "Packaging and shipping" answer to 2 decimal places. Material inspection Production Engineering Equipment setup Packaging and shipping % of material dollars per hour per setup per setup per unit Req Al Req A2 > Complete this question by entering your answers in the tabs below. Req A2 What unit product costs will be reported for the two products if the revised ABC system is used? Note: Do not round intermediate calculations. Req A1 Direct material costs Direct labor cost Overhead: Material inspection Production Engineering Equipment setup Packaging and shipping Total costs Number of units Unit cost $ LC-20 799,200 $ 621,600 1,420,800 0 < LC-50 266,400 310,800 577,200 Reg A1 0 Ren 07

Expert Answer:

Related Book For

Quantitative Methods for Business

ISBN: 978-0324651751

11th Edition

Authors: David Anderson, Dennis Sweeney, Thomas Williams, Jeffrey cam

Posted Date:

Students also viewed these accounting questions

-

The following information applies to the questions displayed below Dower Corporation prepares its financial statements according to IFRS On March 31, 2021, the company purchased equipment for...

-

The following information applies to the questions displayed below Juan Diego began the year with a tax basis in his partnership interest of $50,000 During the year, he was allocated $20,000 of...

-

The following information applies to the questions displayed below.] Ramirez Company installs a computerized manufacturing machine in its factory at the beginning of the year at a cost of $86,800....

-

Explain how community service staff members can monitor the impact of work undertaken and/or services provided in line with the scope of their own work role?

-

1. Given that Sisuphan returned the cash, was it fair of the dealerships general manager to terminate Sisuphans employment? Why or why not? 2. Why was Sisuphan convicted of embezzlement instead of...

-

The shell of rigid rock that makes up the earths crust and the outer part of the mantle is called the a. Lithosphere b. Asthenosphere c. Thermosphere d. Subduction zone

-

How do we apply structural modeling to design?

-

Mandy Peters, the lead accountant of Ross Co., would like to buy a new general ledger software program. She couldnt do it because all funds were frozen for the rest of the fiscal period. Mandy called...

-

CON 448: SUSTAINABLE CONSTRUCTION PROJECT ASSIGNMENT - 1 Product Research DESCRIPTION & INSTRUCTIONS: As construction field engineers, you may be asked to source materials or equipment that is...

-

We have learned how companies come up with their interim financial reports. Please pick a publicly traded company of your choice, look up its more recent quarterly report on its website, and comment...

-

Farkle is a dice game played with 6 six-sided dice. There are many rules and variations to the game so let's stick with the simplest version: Each die showing a 1 is worth 100 points and each die...

-

In what ways can the informal organization and the norms and values of its culture affect the shape of an organization?

-

As organizations grow and differentiate, what problems can arise with a functional structure?

-

In what ways can organizational culture increase organizational effectiveness? Why is it important to obtain the right fit between organizational structure and culture?

-

What are the strengths of the payback method?

-

How do newcomers learn the culture of an organization? How can an organization encourage newcomers to develop (a) an institutionalized role orientation and (b) an individualized role orientation?

-

In a truck-loading operation, the arrival rate. For loading trucks is 12 trucks per hour, and the average service time is 3.5 minutes. What is the mean time between arrivals (in minutes)?

-

A stock has had returns of 8 percent, 26 percent, 14 percent, 17 percent, 31 percent, and 1 percent over the last six years. What are the arithmetic and geometric average returns for the stock?

-

Open the file Foster Rev. Select cells B6:E8 and name these cells Shipping-Cost. Select cells B19:E21 and name these cells Units-Shipped. Use these names in the sum-product function in cell C14 to...

-

United Express Service (UES) uses large quantities of packaging materials at its four distribution hubs. After screening potential suppliers, UES identified six vendors that can provide packaging...

-

Assume that the project in Problem 3 has the following activity times (in months): a. Find the critical path. b. The project must be completed in 11/2 years. Do you anticipate difficulty in meeting...

-

Based on Exhibit 1, which statement is most likely correct? A . Company A has below-average liquidity risk. B . Company B has above-average solvency risk. C . Company A has made one or more...

-

Using the information presented in Exhibit 4, the quick ratio for SAP Group at 31 December 2017 is closest to: A . 1.00. B . 1.07. C . 1.17.

-

Using the information presented in Exhibit 14, the fi nancial leverage ratio for SAP Group at December 31, 2017 is c losest to: A . 1.50. B . 1.66. C . 2.00.

Study smarter with the SolutionInn App