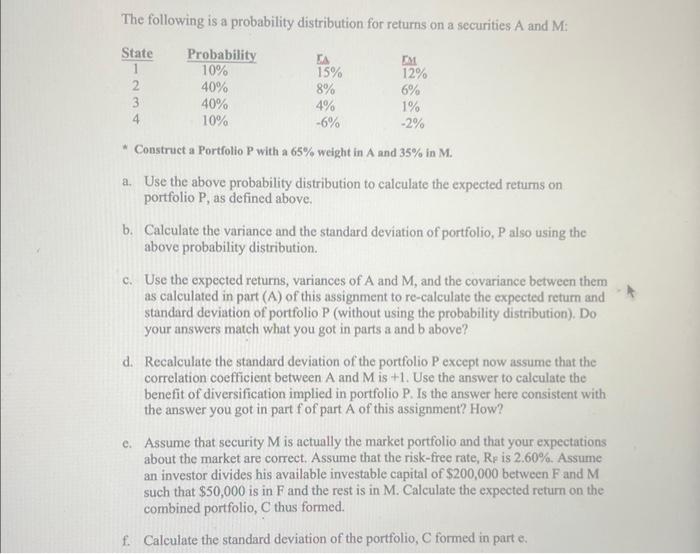

Question: The following is a probability distribution for returns on a securities A and M : * Construct a Portfolio P with a 65% weight in

The following is a probability distribution for returns on a securities A and M : * Construct a Portfolio P with a 65% weight in A and 35% in M. a. Use the above probability distribution to calculate the expected retums on portfolio P, as defined above. b. Calculate the variance and the standard deviation of portfolio, P also using the above probability distribution. c. Use the expected returns, variances of A and M, and the covariance between them as calculated in part (A) of this assignment to re-calculate the expected return and standard deviation of portfolio P (without using the probability distribution). Do your answers match what you got in parts a and b above? d. Recalculate the standard deviation of the portfolio P except now assume that the correlation coefficient between A and M is +1 . Use the answer to calculate the benefit of diversification implied in portfolio P. Is the answer here consistent with the answer you got in part f of part A of this assignment? How? e. Assume that security M is actually the market portfolio and that your expectations about the market are correct. Assume that the risk-free rate, RF is 2.60%. Assume an investor divides his available investable capitat of $200,000 between F and M such that $50,000 is in F and the rest is in M. Calculate the expected return on the combined portfolio, C thus formed. f. Catculate the standard deviation of the portfolio, C formed in part e

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts