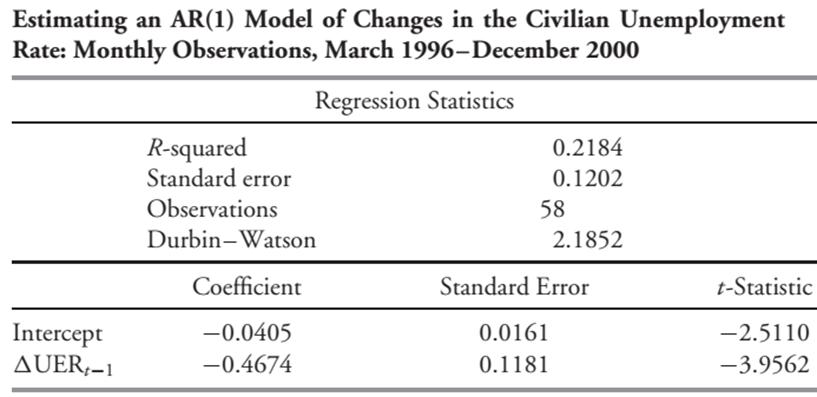

The following table gives the regression output of an AR(1) model on first differences in the unemployment

Question:

The following table gives the regression output of an AR(1) model on first differences in the unemployment rate.

Assume that changes in the civilian unemployment rate are covariance stationary and that an AR(1) model is a good description for the time series of changes in the unemployment rate.

1. Describe how to interpret the DW statistic for this regression.

2. What is the mean-reverting level to which changes in the unemployment rate converge?

3. The current change (first difference) in the unemployment rate is 0.0300. Assume that the mean-reverting level for changes in the unemployment rate is -0.0276.

A. What is the best prediction of the next change?

B. What is the prediction of the change following the next change?

Expert Answer:

1 The DurbinWatson DW statistic measures the presence of autocorrelation in the regression residuals ... View the full answer

Quantitative Investment Analysis

ISBN: 978-1119104223

3rd edition

Authors: Richard A. DeFusco, Dennis W. McLeavey, Jerald E. Pinto, David E. Runkle