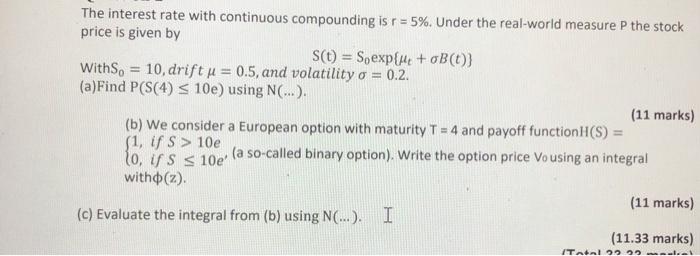

Question: The interest rate with continuous compounding is r = 5%. Under the real-world measure P the stock price is given by S(t) = S, exp{H

The interest rate with continuous compounding is r = 5%. Under the real-world measure P the stock price is given by S(t) = S, exp{H + 0B(0) WithS, = 10, drift p = 0.5, and volatility o = 0.2. (a)Find P(S(4) 10e loirs s 10e (a so-called binary option). Write the option price Vo using an integral with(z) (11 marks) (c) Evaluate the integral from (b) using N(...). I (11.33 marks) Total

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock