Question: The last question please! Thank you Question 6 Jack invests in a market with two stocks and the riskfree asset. The expected return of the

The last question please! Thank you

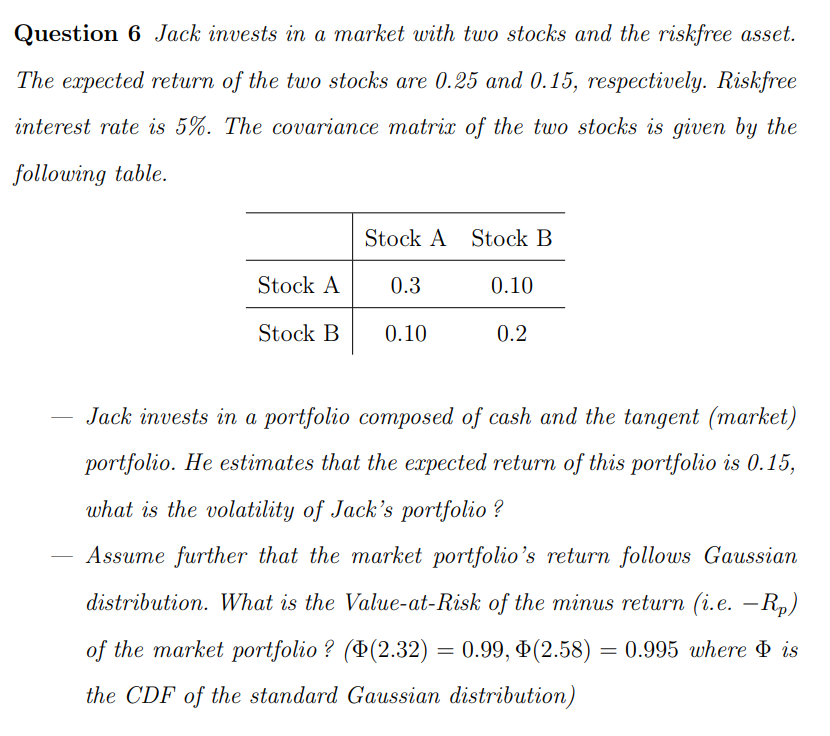

Question 6 Jack invests in a market with two stocks and the riskfree asset. The expected return of the two stocks are 0.25 and 0.15 , respectively. Riskfree interest rate is 5\%. The covariance matrix of the two stocks is given by the following table. - Jack invests in a portfolio composed of cash and the tangent (market) portfolio. He estimates that the expected return of this portfolio is 0.15 , what is the volatility of Jack's portfolio? - Assume further that the market portfolio's return follows Gaussian distribution. What is the Value-at-Risk of the minus return (i.e. Rp ) of the market portfolio? ((2.32)=0.99,(2.58)=0.995 where is the CDF of the standard Gaussian distribution)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts