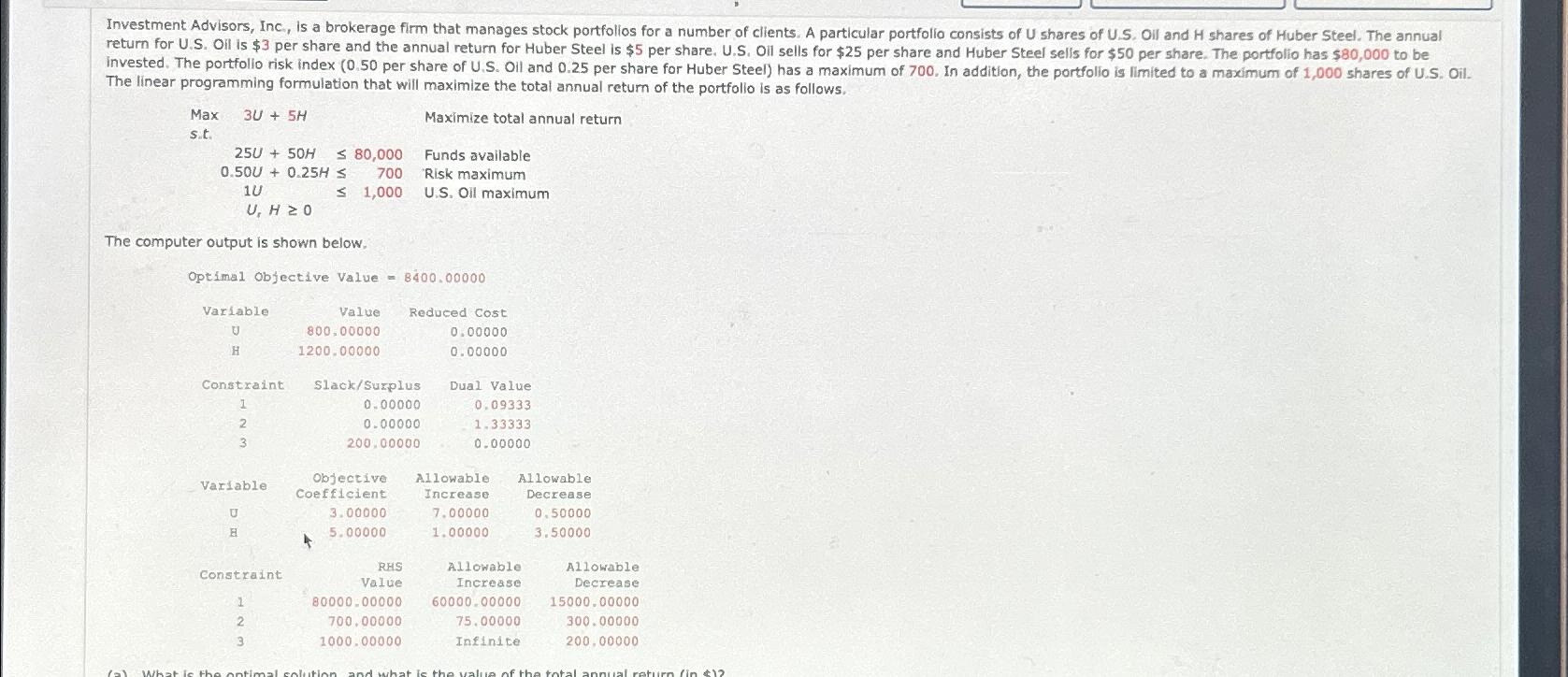

Question: The linear programming formulation that will maximize the total annual return of the portfolio is as follows. Max 3 U + 5 H Maximize total

The linear programming formulation that will maximize the total annual return of the portfolio is as follows.

Max Maximize total annual return

Funds available

Risk maximum

Oil maximum

The computer output is shown below.

tableVariableValue,Reduced CostHConstraintSlackSuxplusDual ValuetableVariabletableObjectiveCoefflcienttableAllowableIncreasetableAllowableDecreasevHConstrainttableRHSValuetableAllowableIncreasetableAllowableDecreaseInfinite,

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock