The Pineapple Industry Association (PIA) is a government owned enterprise which is legislated to generate its...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

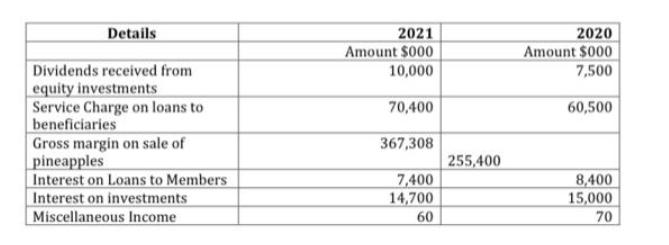

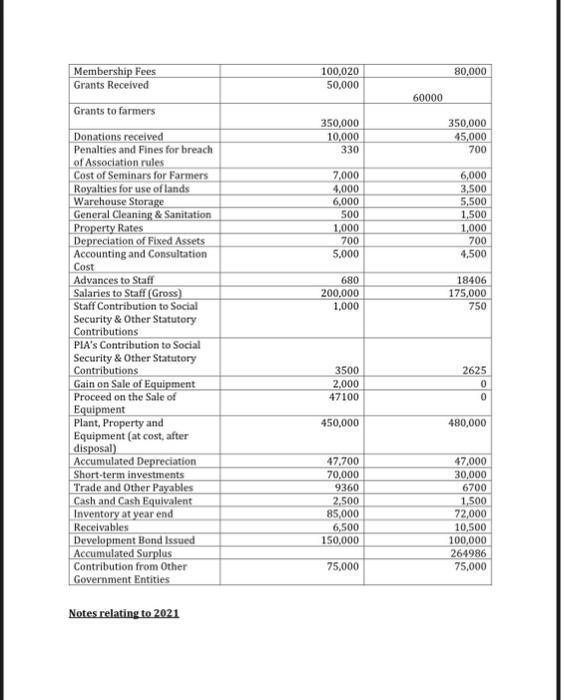

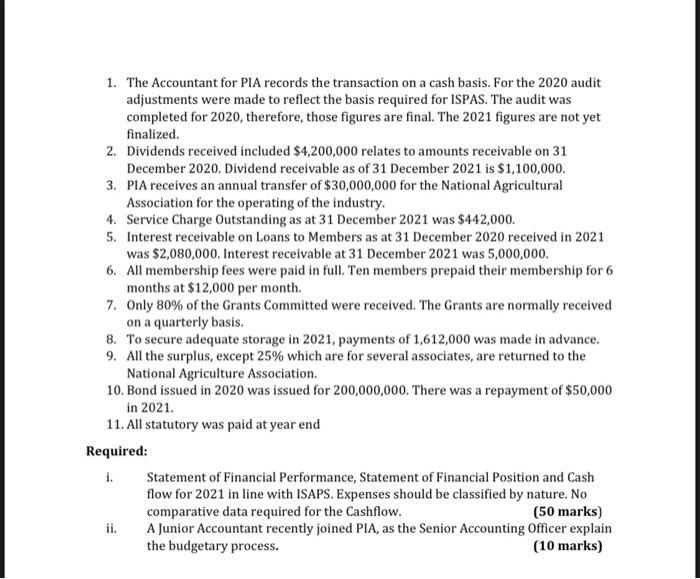

The Pineapple Industry Association (PIA) is a government owned enterprise which is legislated to generate its own income which it uses to cover capital and recurrent expenditures. PIA is an agent of National Agriculture Association. The Young Famers association controls 25% of PIA. Outside of these powers, its government also provide Pineapple Industry with monthly subventions to cover its recurrent expenditures based on Pineapple Enterprise budgetary demands and the legal allocations by the government. Pineapple Enterprises uses ISPAP to prepare its financial statements. You were asked by to government to assist Pineapple Industry with its accounting processes, which involved the recording, generation and preparation of accounting transactions and final accounts as stipulated by the IPSASS. Collaborating with a team of qualified and experienced accountants, you were able to prepare the following accounting information of Pineapple Industry for the year ended December 2021. Details Dividends received from equity investments Service Charge on loans to beneficiaries Gross margin on sale of pineapples Interest on Loans to Members Interest on investments Miscellaneous Income 2021 Amount $000 10,000 70,400 367,308 7,400 14,700 60 255,400 2020 Amount $0001 7,500 60,500 8,400 15,000 70 Membership Fees Grants Received Grants to farmers Donations received Penalties and Fines for breach of Association rules Cost of Seminars for Farmers Royalties for use of lands Warehouse Storage General Cleaning & Sanitation Property Rates Depreciation of Fixed Assets Accounting and Consultation Cost Advances to Staff Salaries to Staff (Gross) Staff Contribution to Social Security & Other Statutory Contributions PIA's Contribution to Social Security & Other Statutory Contributions Gain on Sale of Equipment Proceed on the Sale of Equipment Plant, Property and Equipment (at cost, after disposal) Accumulated Depreciation Short-term investments Trade and Other Payables Cash and Cash Equivalent Inventory at year end Receivables Development Bond Issued Accumulated Surplus Contribution from Other Government Entities Notes relating to 2021 100,020 50,000 350,000 10,000 330 7,000 4,000 6,000 500 1,000 700 5,000 680 200,000 1,000 3500 2,000 47100 450,000 47,700 70,000 9360 2,500 85,000 6,500 150,000 75,000 60000 80,000 350,000 45,000 700 6,000 3,500 5,500 1,500 1,000 700 4,500 18406 175,000 750 2625 0 0 480,000 47,000 30,000 6700 1,500 72,000 10,500 100,000 264986 75,000 1. The Accountant for PIA records the transaction on a cash basis. For the 2020 audit adjustments were made to reflect the basis required for ISPAS. The audit was completed for 2020, therefore, those figures are final. The 2021 figures are not yet finalized. 2. Dividends received included $4,200,000 relates to amounts receivable on 31 December 2020. Dividend receivable as of 31 December 2021 is $1,100,000. 3. PIA receives an annual transfer of $30,000,000 for the National Agricultural Association for the operating of the industry. 4. Service Charge Outstanding as at 31 December 2021 was $442,000. 5. Interest receivable on Loans to Members as at 31 December 2020 received in 2021 was $2,080,000. Interest receivable at 31 December 2021 was 5,000,000. 6. All membership fees were paid in full. Ten members prepaid their membership for 6 months at $12,000 per month. 7. Only 80% of the Grants Committed were received. The Grants are normally received on a quarterly basis. 8. To secure adequate storage in 2021, payments of 1,612,000 was made in advance. 9. All the surplus, except 25% which are for several associates, are returned to the National Agriculture Association. 10. Bond issued in 2020 was issued for 200,000,000. There was a repayment of $50,000 in 2021. 11. All statutory was paid at year end Required: i. ii. Statement of Financial Performance, Statement of Financial Position and Cash flow for 2021 in line with ISAPS. Expenses should be classified by nature. No comparative data required for the Cashflow. A Junior Accountant recently joined PIA, as the Senior Accounting the budgetary process. (50 marks) Officer explain (10 marks) The Pineapple Industry Association (PIA) is a government owned enterprise which is legislated to generate its own income which it uses to cover capital and recurrent expenditures. PIA is an agent of National Agriculture Association. The Young Famers association controls 25% of PIA. Outside of these powers, its government also provide Pineapple Industry with monthly subventions to cover its recurrent expenditures based on Pineapple Enterprise budgetary demands and the legal allocations by the government. Pineapple Enterprises uses ISPAP to prepare its financial statements. You were asked by to government to assist Pineapple Industry with its accounting processes, which involved the recording, generation and preparation of accounting transactions and final accounts as stipulated by the IPSASS. Collaborating with a team of qualified and experienced accountants, you were able to prepare the following accounting information of Pineapple Industry for the year ended December 2021. Details Dividends received from equity investments Service Charge on loans to beneficiaries Gross margin on sale of pineapples Interest on Loans to Members Interest on investments Miscellaneous Income 2021 Amount $000 10,000 70,400 367,308 7,400 14,700 60 255,400 2020 Amount $0001 7,500 60,500 8,400 15,000 70 Membership Fees Grants Received Grants to farmers Donations received Penalties and Fines for breach of Association rules Cost of Seminars for Farmers Royalties for use of lands Warehouse Storage General Cleaning & Sanitation Property Rates Depreciation of Fixed Assets Accounting and Consultation Cost Advances to Staff Salaries to Staff (Gross) Staff Contribution to Social Security & Other Statutory Contributions PIA's Contribution to Social Security & Other Statutory Contributions Gain on Sale of Equipment Proceed on the Sale of Equipment Plant, Property and Equipment (at cost, after disposal) Accumulated Depreciation Short-term investments Trade and Other Payables Cash and Cash Equivalent Inventory at year end Receivables Development Bond Issued Accumulated Surplus Contribution from Other Government Entities Notes relating to 2021 100,020 50,000 350,000 10,000 330 7,000 4,000 6,000 500 1,000 700 5,000 680 200,000 1,000 3500 2,000 47100 450,000 47,700 70,000 9360 2,500 85,000 6,500 150,000 75,000 60000 80,000 350,000 45,000 700 6,000 3,500 5,500 1,500 1,000 700 4,500 18406 175,000 750 2625 0 0 480,000 47,000 30,000 6700 1,500 72,000 10,500 100,000 264986 75,000 1. The Accountant for PIA records the transaction on a cash basis. For the 2020 audit adjustments were made to reflect the basis required for ISPAS. The audit was completed for 2020, therefore, those figures are final. The 2021 figures are not yet finalized. 2. Dividends received included $4,200,000 relates to amounts receivable on 31 December 2020. Dividend receivable as of 31 December 2021 is $1,100,000. 3. PIA receives an annual transfer of $30,000,000 for the National Agricultural Association for the operating of the industry. 4. Service Charge Outstanding as at 31 December 2021 was $442,000. 5. Interest receivable on Loans to Members as at 31 December 2020 received in 2021 was $2,080,000. Interest receivable at 31 December 2021 was 5,000,000. 6. All membership fees were paid in full. Ten members prepaid their membership for 6 months at $12,000 per month. 7. Only 80% of the Grants Committed were received. The Grants are normally received on a quarterly basis. 8. To secure adequate storage in 2021, payments of 1,612,000 was made in advance. 9. All the surplus, except 25% which are for several associates, are returned to the National Agriculture Association. 10. Bond issued in 2020 was issued for 200,000,000. There was a repayment of $50,000 in 2021. 11. All statutory was paid at year end Required: i. ii. Statement of Financial Performance, Statement of Financial Position and Cash flow for 2021 in line with ISAPS. Expenses should be classified by nature. No comparative data required for the Cashflow. A Junior Accountant recently joined PIA, as the Senior Accounting the budgetary process. (50 marks) Officer explain (10 marks)

Expert Answer:

Answer rating: 100% (QA)

Question 1 Pineapple Industry Association Statement of Financial Performance For the year ended December 31 2021 000 Revenue Service Charge on loans to beneficiaries 367308 Gross margin on sale of pin... View the full answer

Related Book For

Government and Not for Profit Accounting Concepts and Practices

ISBN: 978-1118155974

6th edition

Authors: Michael H. Granof, Saleha B. Khumawala

Posted Date:

Students also viewed these accounting questions

-

CBC is a government owned enterprise which is legislated to generate its own income which it uses to cover capital and recurrent expenditures. The legislations also give the government the powers to...

-

The Pineapple Industry Association (PIA) is a government owned enterprise which is legislated to generate its own income which it uses to cover capital and recurrent expenditures. PIA is an agent of...

-

The income statement for the year ended December 31, 2015, the balance sheets for December 31, 2015 and 2014, and the statement of retained earnings for the year ended December 31, 2015, for...

-

1. What is Anthropology, Sociology, and Political Science in your own understanding? 2. What is the nature of Anthropology, Sociology, and Political Science? 3. How are they similar with one another?

-

While some states, such as Tennessee, have been quick to ban or limit international outsourcing of government activities, other state governments have sought to take advantage of tow-cost...

-

Suppose a bond has a modified duration of 4. By approximately how much will the bonds value change if interest rates a. increase by 50 basis points b. decrease by 150 basis points c. increase by 10...

-

What are the advantages and disadvantages of using the S-curve analysis as a project control tool?

-

OBrien Company manufactures and sells one product. The following information pertains to each of the companys first three years of operations: Variable costs per unit: Manufacturing: Direct materials...

-

A man measures the acceleration of an elevator using a bathroom scale. He places a 30 kg mass on it. The scale reads 30 kg when the elevator is at rest, and 34 kg when the elevator is moving....

-

Aman and Juanita have $150,000 in their business bank account. You have calculated their warehouse stock and equipment to be valued at a total of $480,000. They want to take out a policy for...

-

Write a paper, where you discuss what are some of the initiatives of community policing? In your paper be sure to: identify and discuss some community policing initiatives/programs. support your...

-

What are the phases of social media marketing maturity? How does social media marketing change for companies as they shift from the trial phase to the transition phase and eventually move into the...

-

Which of the four social media user types identified by the Social Technographics Score would you classify yourself as? What would this mean for marketers targeting you?

-

On 1 May 2011 Jenny Barnes, who is a retailer, had the following balances in her books: Premises 70,000; Equipment 8,200; Vehicles 5,100; Inventory 9,500; Trade accounts receivable 150. Jenny does...

-

What is the difference between absorption costing and marginal costing?

-

What are the three components of an array definition?

-

All nonverbal messages have key characteristics that communicators must take into account. Identify the characteristics of nonverbal messages. Check all that apply. a. Nonverbal messages have...

-

Find the area of the surface generated by revolving the para- metric curve x = cos 1, y = sin? 1 (0 < I sa/2) about the y-axis.

-

Crystal City established a capital projects fund to account for the construction of a new bridge. During the year the fund was established, the city issued bonds, signed (and encumbered) $6 million...

-

A city acquires $1 million of public safety emergency communication equipment by entering into a capital lease. The city divides its rst rent payment of $ 135,868 between lease interest and lease...

-

The balance sheets of both enterprise funds and internal service funds report capital assets and long-term debt. What does that tell you about the funds measurement focus and basis of accounting?...

-

The \(10-\mathrm{kg} / \mathrm{m}\) cable is suspended between the supports \(A\) and \(B\). If the cable can sustain a maximum tension of \(1.5 \mathrm{kN}\) and the maximum sag is \(3...

-

The cable has a weight of \(5 \mathrm{lb} / \mathrm{ft}\). If it can \(\operatorname{span} L=300 \mathrm{ft}\) and has a sag of \(h=15 \mathrm{ft}\), determine the length of the cable. The ends \(A\)...

-

Solve Prob. 6-1 using the Mller-Breslau principle. Data From Problem 6.1 3 ft 6 ft C 6 ft B 9 ft

Study smarter with the SolutionInn App