Question: The pure expectations theory, or the expectations hypothess, asserts that long-term interest rates can be used to estimate future short-term interest rates. Based on the

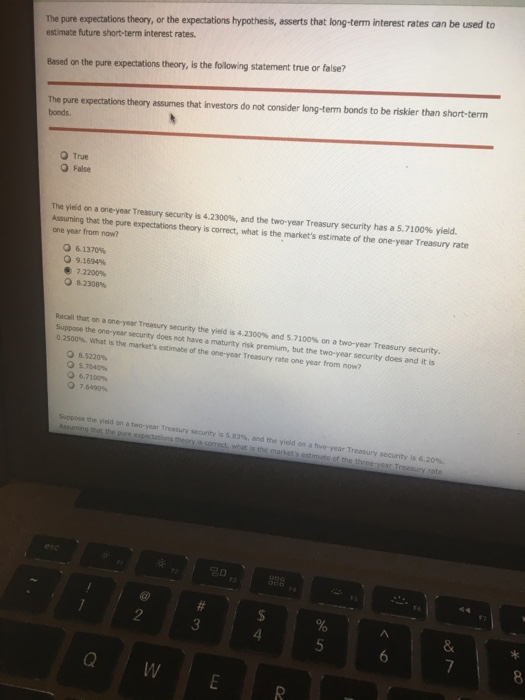

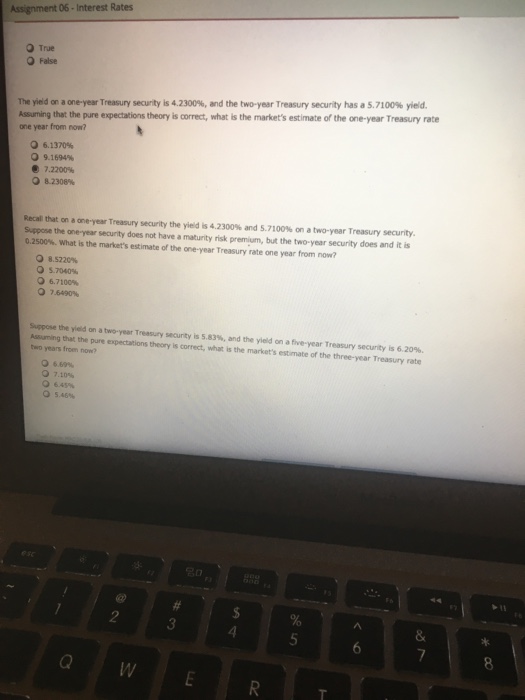

The pure expectations theory, or the expectations hypothess, asserts that long-term interest rates can be used to estimate future short-term interest rates. Based on the pure expectations theory, is the folowing statement true or false? The pure expectations theory assumes that investors do not consider long-term bonds to be riskier than short-term bonds O True O False The yield on a one-year Treasury security is 4.2300%, and the two-year Treasury Assuming that the pure expectations theory is correct, what is one year from now? security has a 5.7100% yield. the market's estimate of the one-year Treasury rate 6.1370% 9.1694% 7.2200% 82308% Recall that on a one-year Treasury security the yield is 4.2300% and S.7100% on a two-year Treasury secunty. Suppose the one-year secunty does not have a matunty risk premlum, but the two-year security does and it is 0.2500%, what is the market's estimate of the one-year Treasury rate one year from now? 8.5220% 57040% 9 6.7100% 9 7 6400% reasury security is 6.20%. 2 3 4

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts