Question: The question is attached. Problem 3 (20') Three funds' returns follow the market index model as below: Rot = ap + PpRint + Ept where

The question is attached.

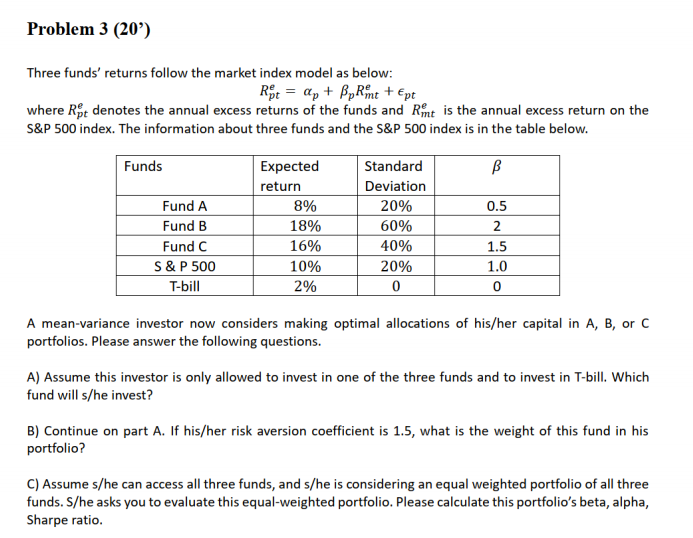

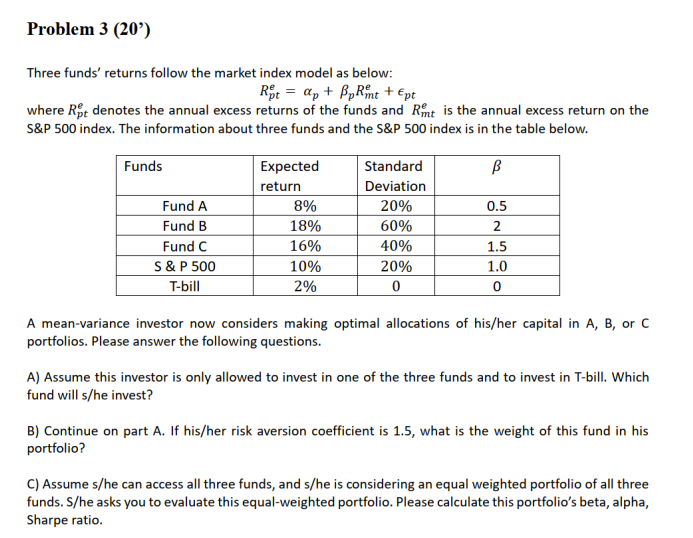

Problem 3 (20') Three funds' returns follow the market index model as below: Rot = ap + PpRint + Ept where Rot denotes the annual excess returns of the funds and Rit is the annual excess return on the S&P 500 index. The information about three funds and the S&P 500 index is in the table below. Funds Expected Standard B return Deviation Fund A 8% 20% 0.5 Fund B 18% 60% 2 Fund C 16% 40% 1.5 S & P 500 10% 20% 1.0 T-bill 2% 0 0 A mean-variance investor now considers making optimal allocations of his/her capital in A, B, or C portfolios. Please answer the following questions. A) Assume this investor is only allowed to invest in one of the three funds and to invest in T-bill. Which fund will s/he invest? B) Continue on part A. If his/her risk aversion coefficient is 1.5, what is the weight of this fund in his portfolio? C) Assume s/he can access all three funds, and s/he is considering an equal weighted portfolio of all three funds. S/he asks you to evaluate this equal-weighted portfolio. Please calculate this portfolio's beta, alpha, Sharpe ratio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts