Question: the question is described as below. 5. (4 points) (Two Versions of Asian Calls and their no-arbitrage price) Let us say we have an asset

the question is described as below.

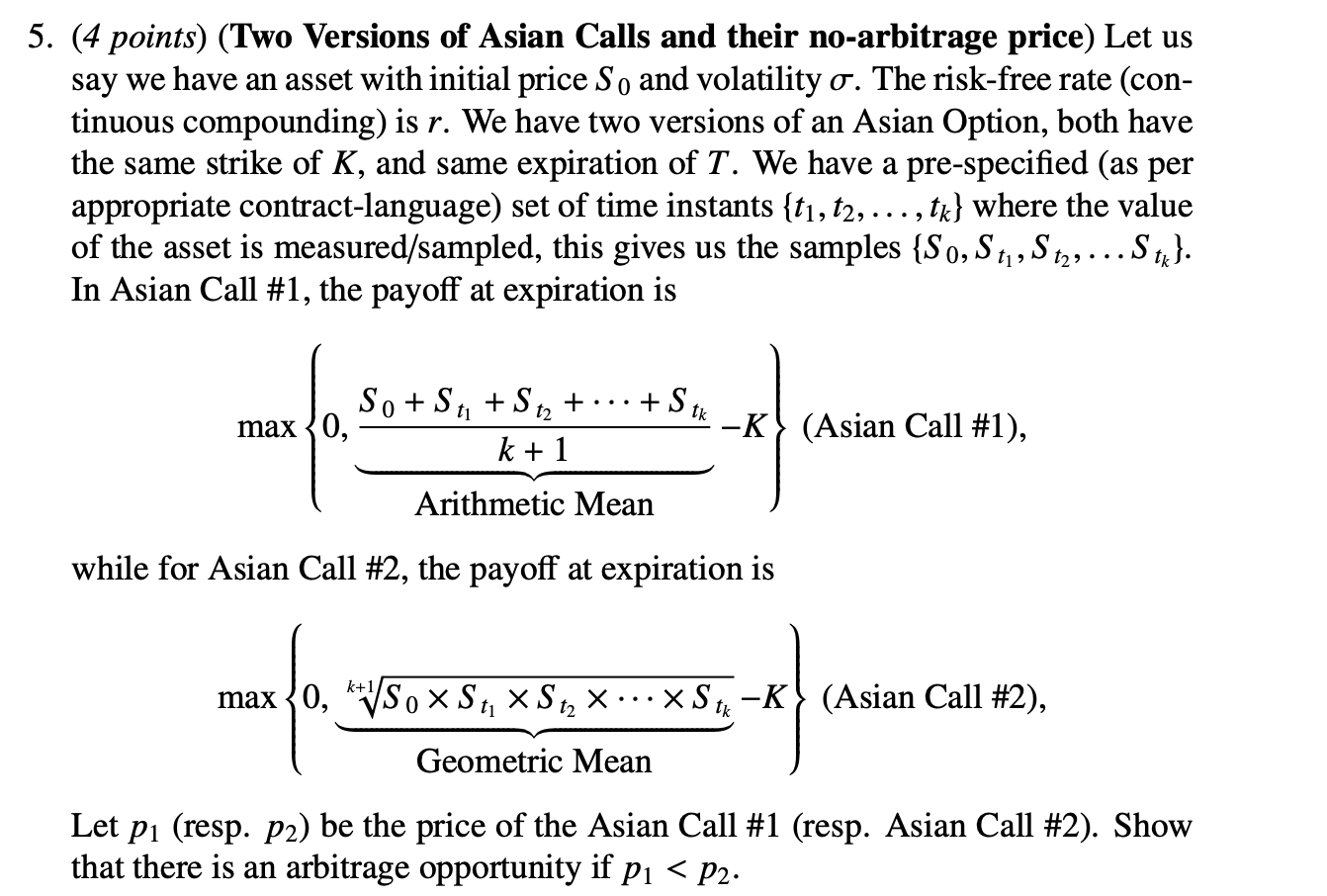

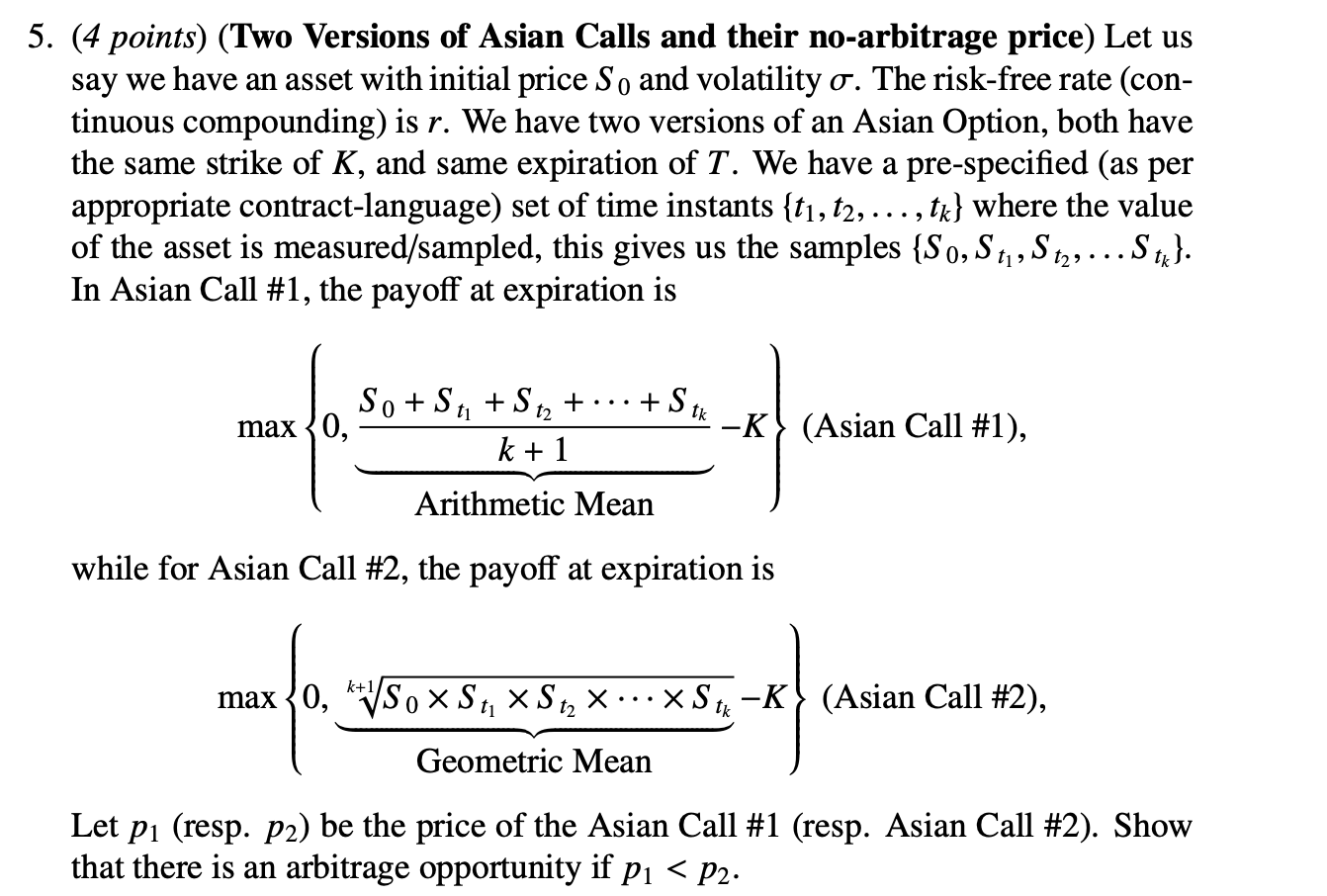

5. (4 points) (Two Versions of Asian Calls and their no-arbitrage price) Let us say we have an asset with initial price So and volatility o. The risk-free rate (con- tinuous compounding) is r. We have two versions of an Asian Option, both have the same strike of K, and same expiration of T. We have a pre-specified (as per appropriate contract-language) set of time instants {t1, t2, ..., tx} where the value of the asset is measured/sampled, this gives us the samples {So, S , Stz, . . . So). In Asian Call #1, the payoff at expiration is max 3 0, So+Sa +sat ... +5 th k + 1 -K (Asian Call #1), Arithmetic Mean while for Asian Call #2, the payoff at expiration is max

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts