Question: The right answer is highlighted just need to understand how to get to the right answer 019-22. A (typical) firm in a perfectly competitive constant

The right answer is highlighted just need to understand how to get to the right answer

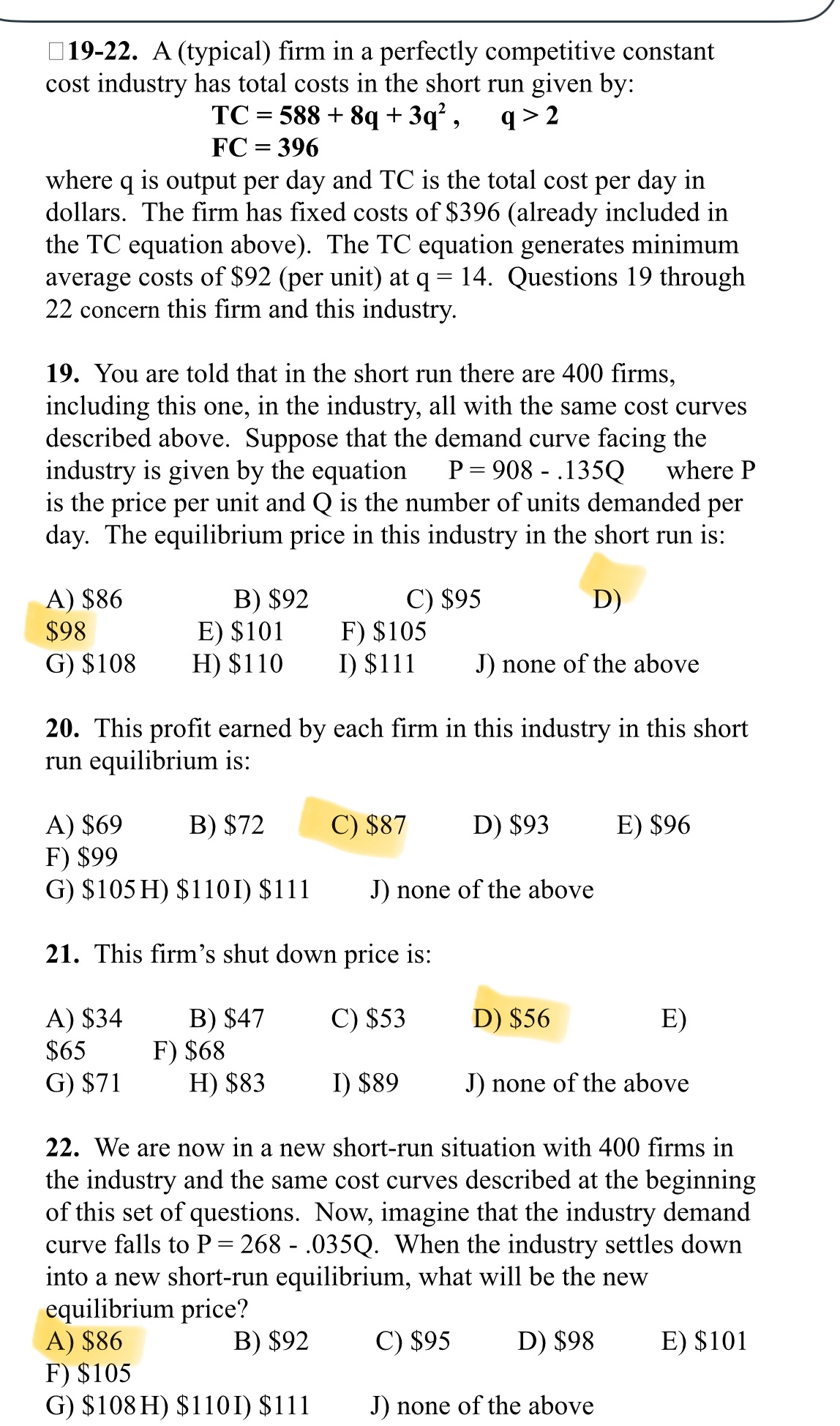

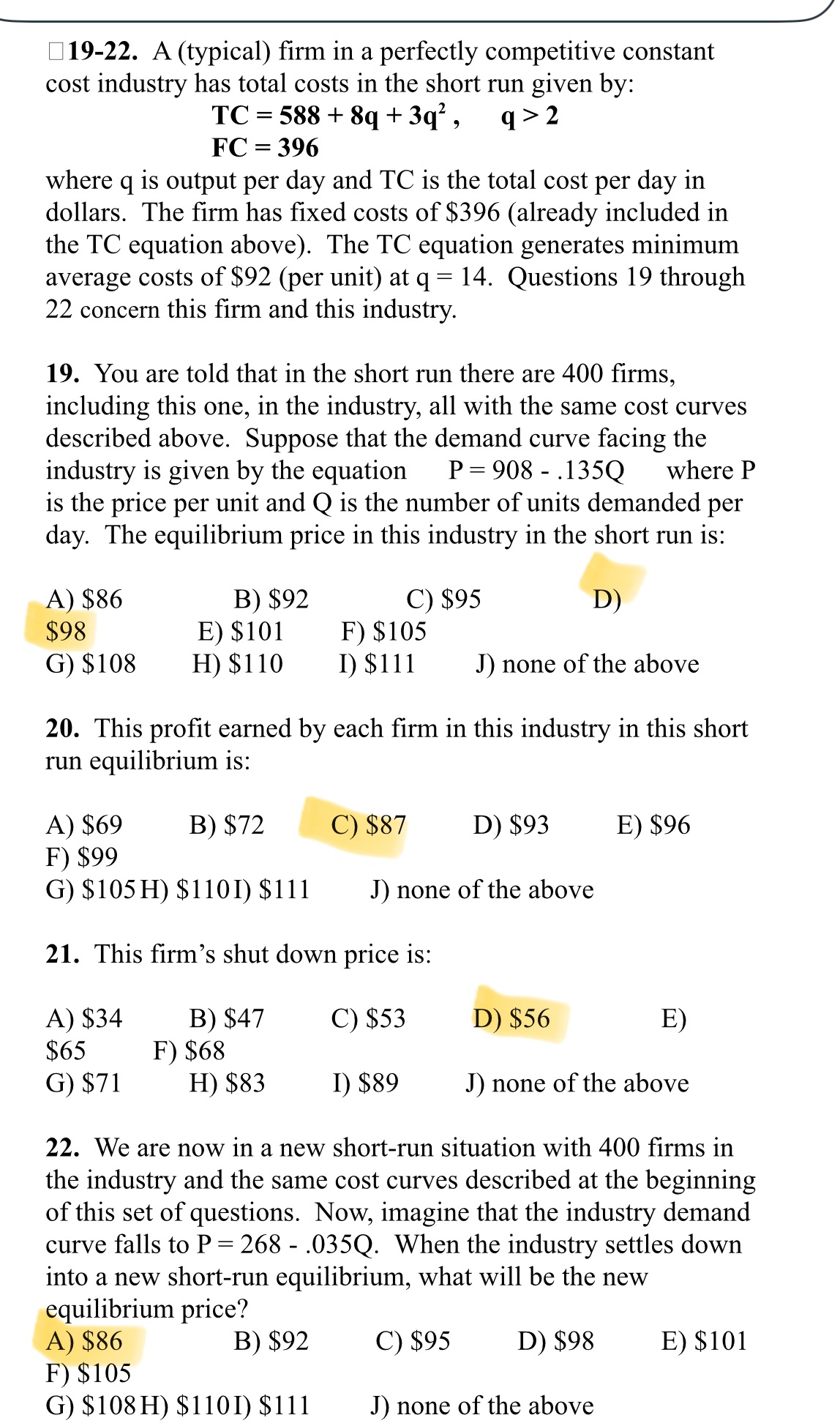

019-22. A (typical) firm in a perfectly competitive constant cost industry has total costs in the short run given by: TC = 588 + 8q + 3q2 , q>2 FC = 396 where q is output per day and TC is the total cost per day in dollars. The firm has fixed costs of $396 (already included in the TC equation above). The TC equation generates minimum average costs of $92 (per unit) at q = 14. Questions 19 through 22 concern this firm and this industry. 19. You are told that in the short run there are 400 firms, including this one, in the industry, all with the same cost curves described above. Suppose that the demand curve facing the industry is given by the equation P= 908 - .135Q where P is the price per unit and Q is the number of units demanded per day. The equilibrium price in this industry in the short run is: A) $86 B) $92 C) $95 D) $98 E) $101 F) $105 G) $108 H) $1 10 I $111 J) none of the above 20. This profit earned by each firm in this industry in this short run equilibrium is: A) $69 B) $72 C) $87 D) $93 E) $96 F) $99 G) $105H) $1101) $111 J) none of the above 21. This firm's shut down price is: A) $34 B) $47 C) $53 D) $56 E $65 F) $68 G) $71 H) $83 I) $89 J) none of the above 22. We are now in a new short-run situation with 400 firms in the industry and the same cost curves described at the beginning of this set of questions. Now, imagine that the industry demand curve falls to P = 268 - .035Q. When the industry settles down into a new short-run equilibrium, what will be the new equilibrium price? A) $86 B) $92 C $95 D) $98 E) $101 F) $105 G) $108H) $1101) $111 J) none of the above

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts