Question: The solution for the weights for the optimal risky portfolio is as the following: WE = 1-WD In WD, Let RD = E(rD)- rf and

The solution for the weights for the optimal risky portfolio is as the following:

WE = 1-WD

In WD, Let RD = E(rD)- rf and RE = E(rD)- rf

Start by maximizing the shape ratio to find the solution given above. Show all your derivations steps.

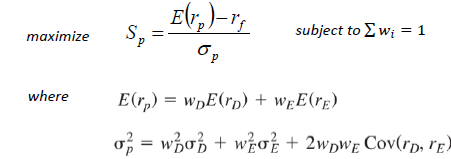

W [E(ro)-ro-[E(re)-r, Cov(ro,rg) [E(r.)-r]0+[E(re)-r, 10-[E(r.)r, +E(re)-r,]Cov(rore) maximize S E(",)-r. subject to w; = 1 P where E(rn) = wpE(rp) + wpE(re) om = woj + wo + 2wpwp Cov('d, rp) W [E(ro)-ro-[E(re)-r, Cov(ro,rg) [E(r.)-r]0+[E(re)-r, 10-[E(r.)r, +E(re)-r,]Cov(rore) maximize S E(",)-r. subject to w; = 1 P where E(rn) = wpE(rp) + wpE(re) om = woj + wo + 2wpwp Cov('d, rp)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock