Question: The table below contains the implied volatility and option price for a series of call options of varying strike prices and varying time to expiration.

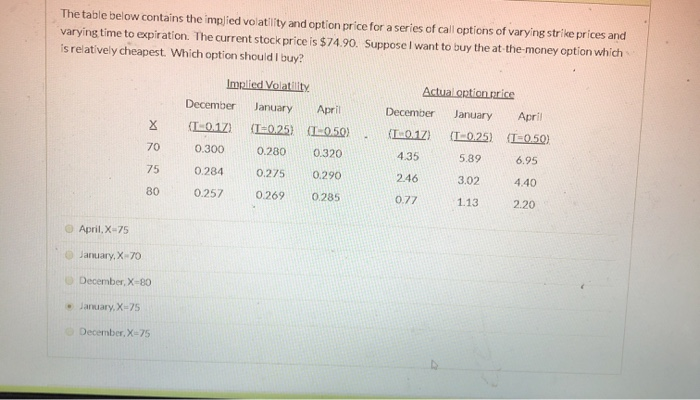

The table below contains the implied volatility and option price for a series of call options of varying strike prices and varying time to expiration. The current stock price is $74.90. Suppose I want to buy the at the money option which is relatively cheapest. Which option should I buy? Implied Volatility December January April (T-017) (T-0.25) (1-0.50) 0.300 0.280 0.320 April X Actual option price December January TL17) T-0.25) T=0.50) 435 5.89 6.95 70 75 0.284 0.275 0.290 2.46 3.02 4.40 80 0.257 0.269 0.285 0.77 1.13 2.20 April,X-75 January, X 70 December, X-80 JanuaryX-75 December, X-75

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock