Question: The table below shows standard deviations and correlation coefficients for seven stocks from different countries. Calculate the variance of a portfolio with equal investments in

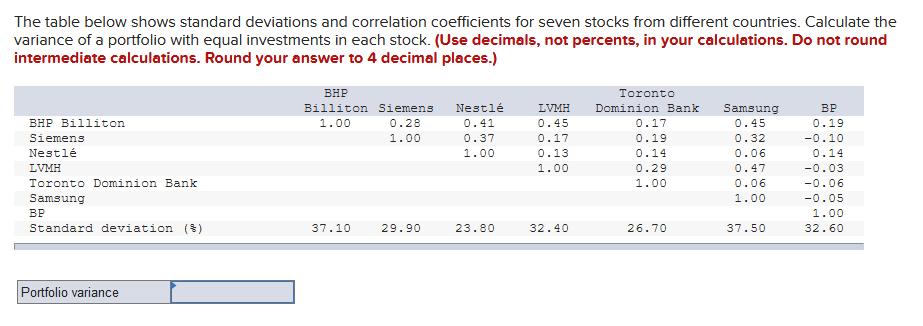

The table below shows standard deviations and correlation coefficients for seven stocks from different countries. Calculate the variance of a portfolio with equal investments in each stock. (Use decimals, not percents, in your calculations. Do not round intermediate calculations. Round your answer to 4 decimal places.) BHP Billiton Siemens 1.00 0.28 1.00 Nestl 0.41 0.37 1.00 LVMH 0.45 0.17 0.13 1.00 BHP Billiton Siemens Nestl LVMH Toronto Dominion Bank Samsung BP Standard deviation (3) Toronto Dominion Bank 0.17 0.19 0.14 0.29 1.00 Samsung 0.45 0.32 0.06 0.47 0.06 1.00 BP 0.19 -0.10 0.14 -0.03 -0.06 -0.05 1.00 32.60 37.10 29.90 23.80 32.40 26.70 37.50 Portfolio variance The table below shows standard deviations and correlation coefficients for seven stocks from different countries. Calculate the variance of a portfolio with equal investments in each stock. (Use decimals, not percents, in your calculations. Do not round intermediate calculations. Round your answer to 4 decimal places.) BHP Billiton Siemens 1.00 0.28 1.00 Nestl 0.41 0.37 1.00 LVMH 0.45 0.17 0.13 1.00 BHP Billiton Siemens Nestl LVMH Toronto Dominion Bank Samsung BP Standard deviation (3) Toronto Dominion Bank 0.17 0.19 0.14 0.29 1.00 Samsung 0.45 0.32 0.06 0.47 0.06 1.00 BP 0.19 -0.10 0.14 -0.03 -0.06 -0.05 1.00 32.60 37.10 29.90 23.80 32.40 26.70 37.50 Portfolio variance

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts